Dollar Tree 2007 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2007 Dollar Tree annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52

|

|

151 MILLION 151 MILLION

151 MILLION 151 MILLION

DOLLAR TREE, INC. • 2007 ANNUAL REPORT

41

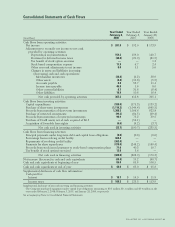

NOTE 5 – LONG-TERM DEBT

Long-term debt at February 2, 2008 and February 3, 2007 consists of the following:

February 2, February 3,

(in millions) 2008 2007

$450.0 million Unsecured Revolving Credit Facility, interest payable monthly at

LIBOR,plus 0.475%, which was 4.47% at February 2, 2008, principal payable

upon expiration of the facility in March 2009 $250.0 $250.0

Demand Revenue Bonds, interest payable monthly at a variable rate which was

3.38% at February 2, 2008, principal payable on demand, maturing June 2018 18.5 18.8

Total long-term debt 268.5 268.8

Less current portion 18.5 18.8

Long-term debt, excluding current portion $250.0 $250.0

Maturities of long-term debt are as follows: 2008 - $18.5 million and 2009 - $250.0 million.

Unsecured Revolving Credit Facility

In March 2004, the Company entered into a five-year

Unsecured Revolving Credit Facility (the Facility). The

Facility provides for a $450.0 million revolving line of

credit, including up to $50.0 million in available let-

ters of credit, bearing interest at LIBOR, plus 0.475%.

The Facility also bears an annual facilities fee, calculat-

ed as a percentage, as defined, of the amount available

under the line of credit and an annual administrative

fee payable quarterly. The Facility, among other

things, requires the maintenance of certain specified

financial ratios, restricts the payment of certain

distributions and prohibits the incurrence of certain

new indebtedness.

Demand Revenue Bonds

On May 20, 1998, the Company entered into an unse-

cured Loan Agreement with the Mississippi Business

Finance Corporation (MBFC) under which the MBFC

issued Taxable Variable Rate Demand Revenue Bonds

(the Bonds) in an aggregate principal amount of $19.0

million to finance the acquisition, construction, and

installation of land, buildings, machinery and equip-

ment for the Company’s distribution facility in Olive

Branch, Mississippi. The Bonds do not contain a pre-

payment penalty as long as the interest rate remains

variable. The Bonds contain a demand provision and,

therefore, are classified as current liabilities.

Credit Agreement

On February 20, 2008, the Company entered into a

five-year $550.0 million Credit Agreement (the

Agreement). The Agreement provides for a $300.0

million revolving line of credit, including up to $150.0

million in available letters of credit, and a $250.0 mil-

lion term loan. The interest rate on the facility will be

based, at the Company’s option, on a LIBOR rate, plus

a margin, or an alternate base rate, plus a margin. The

revolving line of credit also bears a facilities fee, calcu-

lated as a percentage, as defined, of the amount avail-

able under the line of credit, payable quarterly. The

term loan is due and payable in full at the five year

maturity date of the Agreement. The Agreement also

bears an administrative fee payable annually. The

Agreement, among other things, requires the mainte-

nance of certain specified financial ratios, restricts the

payment of certain distributions and prohibits the

incurrence of certain new indebtedness. The

Company’s March 2004, $450.0 million unsecured

revolving credit facility was terminated concurrent

with entering into the Agreement.

NOTE 6 – DERIVATIVE FINANCIAL INSTRUMENTS

Non-Hedging Derivatives

At February 2, 2008, the Company was party to a

derivative instrument in the form of an interest rate

swap that does not qualify for hedge accounting treat-

ment pursuant to the provisions of SFAS No. 133

because it contains a knock-out provision. The swap

creates the economic equivalent of a fixed rate obliga-

tion by converting the variable-interest rate to a fixed

rate. Under this interest rate swap, the Company pays

interest to a financial institution at a fixed rate, as

defined in the agreement. In exchange, the financial

institution pays the Company at a variable interest

rate, which approximates the floating rate on the vari-

able-rate obligation, excluding the credit spread. The

interest rate on the swap is subject to adjustment

monthly. No payments are made by either party for

months in which the variable-interest rate, as calculat-

ed under the swap agreement, is greater than the

“knock-out rate.” The following table summarizes the

terms of the interest rate swap:

AND GROWINGWING

AND GROWINGWING