Delta Airlines 2005 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2005 Delta Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

Table of Contents

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

In accordance with SFAS No. 144, "Accounting for the Impairment or Disposal of Long-Lived Assets," we record impairment

losses on long-lived assets used in operations when events and circumstances indicate the assets may be impaired and the

undiscounted cash flows estimated to be generated by those assets are less than their carrying amounts. For long-lived assets held for

sale, we record impairment losses when the carrying amount is greater than the fair value less the cost to sell. We discontinue

depreciation of long-lived assets once they are classified as held for sale.

To determine impairments for aircraft used in operations, we group assets at the fleet type level (the lowest level for which there

are identifiable cash flows) and then estimate future cash flows based on projections of passenger yield, fuel costs, labor costs and

other relevant factors. If impairment occurs, the amount of the impairment loss recognized is the amount by which the carrying

amount of the aircraft exceeds the estimated fair value. Aircraft fair values are estimated by management using published sources,

appraisals and bids received from third parties, as available. See Note 16 for additional information about asset impairments.

Goodwill and Intangible Assets

In accordance with SFAS No. 142, "Goodwill and Other Intangible Assets," we apply a fair value-based impairment test to the net

book value of goodwill and indefinite-lived intangible assets on an annual basis and, if certain events or circumstances indicate that an

impairment loss may have been incurred, on an interim basis. The annual impairment test date for our goodwill and indefinite-lived

intangible assets is December 31. Intangible assets with determinable useful lives are amortized on a straight-line basis over their

estimated useful lives. Our leasehold and operating rights have definite useful lives and are amortized over their respective lease

terms, which range from nine to 19 years.

We had one reporting unit with assigned goodwill at December 31, 2005 and 2004. In evaluating our goodwill for impairment, we

first compare the reporting unit's fair value to its carrying value. We estimate the fair value of our reporting unit by considering

(1) market multiple and recent transaction values of peer companies and (2) projected discounted future cash flows, if reasonably

estimable. In applying the projected discounted future cash flow methodology, we (1) estimate the reporting unit's future cash flows

based on capacity, passenger yield, traffic, operating costs and other relevant factors and (2) discount those cash flows based on the

reporting unit's weighted average cost of capital. If the reporting unit's fair value exceeds its carrying value, no further testing is

required. If, however, the reporting unit's carrying value exceeds its fair value, we then determine the amount of the impairment

charge, if any. We recognize an impairment charge if the carrying value of the reporting unit's goodwill exceeds its implied fair value.

We perform the impairment test for our indefinite-lived intangible assets by comparing the asset's fair value to its carrying value.

Fair value is estimated based on projected discounted future cash flows. We recognize an impairment charge if the asset's carrying

value exceeds its estimated fair value.

See Note 7 for additional information about the goodwill and intangible assets impairment charges recorded during 2004.

Interest Capitalized

We capitalize interest on advance payments for the acquisition of new aircraft and on construction of ground facilities as an

additional cost of the related assets. Interest is capitalized at our weighted average interest rate on long-term debt or, if applicable, the

interest rate related to specific asset financings. Interest capitalization ends when the equipment or facility is ready for service or its

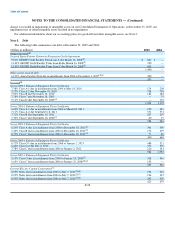

intended use. Capitalized interest totaled $9 million, $10 million and $12 million for the years ended December 31, 2005, 2004 and

2003, respectively.

Interest Expense

In accordance with SOP 90-7, we record interest expense only to the extent (1) interest will be paid during the Chapter 11

proceedings or (2) it is probable interest will be an allowed priority, secured, or

F-19