Ameriprise 2013 Annual Report Download

Download and view the complete annual report

Please find the complete 2013 Ameriprise annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

|

|

A

Ye

a

r

o

f Growth

ANNUAL REPORT

Table of contents

-

Page 1

A Year of Growth ANNUAL R E P O RT -

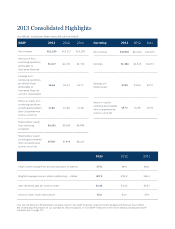

Page 2

... 2013 2012 2011 Assets under management and administration (in billions) $771 $681 $631 Weighted average common shares outstanding - diluted 207.1 222.8 246.3 Cash dividends paid per common share $2.01 $1.43 $0.87 Common stock shares repurchased 17.8 24.6 27.9 This Annual Report... -

Page 3

... Reserve continued its unprecedented bond buying program. In this environment, we drove strong growth and profitability across our businesses. Our results and progress demonstrate that we're executing our strategy well and building on our solid foundation. Ameriprise Financial Annual Report 2013... -

Page 4

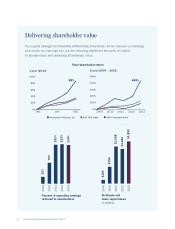

... Financial, Inc. S&P Financials Index $1,668 131% 133% 130% 70% 23% 2009 2010 2011 2012 2013 2009 $164 2010 $756 2011 2012 $1,654 Percent of operating earnings returned to shareholders Dividends and share repurchases in millions 2 Ameriprise Financial Annual Report 2013 2013... -

Page 5

... return last year. $647 2010 2011 $631 2012 $681 2013 Assets under management and administration in billions $771 Ameriprise Financial Annual Report 2013 We grew assets under management and administration to a record $771 billion at the end of 2013, up 13 percent. Operating net revenues... -

Page 6

...also benefit our experienced advisor recruiting, where we have established a firm foothold. 2009 $270 2010 2011 2012 2012 Retail client assets in billions 2009 $271 2010 $342 2011 $384 $396 Operating net revenue per advisor in thousands 4 Ameriprise Financial Annual Report 2013 2013... -

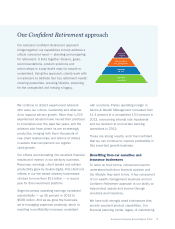

Page 7

...and our Conï¬dent Retirement approach is our ability to help protect assets and income through annuities and insurance. We have built strongly rated businesses that provide excellent product capabilities. Our financial planning model, legacy of maintaining Ameriprise Financial Annual Report 2013 5 -

Page 8

... including ending new third-party sales and adding investment options designed to help manage volatility. We are adding business where we want and experienced a good pick up in variable annuity sales in 2013. We're also focused on offering clients variable annuities without guaranteed benefit riders... -

Page 9

... to compete for a solid share. It's a core focus and a complement to our local strength as we aim to move the business to net in ows over time. $243 $457 2009 2010 2011 $436 2012 $455 2013 Asset Management assets under management in billions $501 Ameriprise Financial Annual Report 2013 7 -

Page 10

..., our win rate is strong, and we continue to build our new business pipeline. As I re ect on our progress in Asset Management, I feel very good about the investments we've made, the capabilities we've built and the opportunity before us. The drivers of net out ows we experienced in 2013 re ected... -

Page 11

... involvement. Ameriprise was recognized again as a member of The Civic 50 - a list of the top civic-minded companies. 16.0% 10.7% 2010 13.7% Operating return on equity, excl. AOCI 2011 2013 $7.05 Evolving our business mix and deploying capital Ameriprise Financial Annual Report 2013 9 -

Page 12

... campaign management. Ameriprise volunteers worked with the St. Bernard Project in New Orleans. In 2013, we supported a diverse group of over 5,000 nonprofits through: • Grant Making - Ameriprise supported 163 nonprofits that help individuals and families in our communities. • Annual Giving... -

Page 13

... in Ameriprise. We will continue to do all we can to reward it. Sincerely, Our values Client focus, integrity, excellence, and respect for individuals and communities in which we live and work James M. Cracchiolo Chairman and Chief Executive Officer Ameriprise Financial Annual Report 2013 11 -

Page 14

...charges Operating total net revenues 2011 $10,192 136 6 - - 2012 2013 $10,217 $11,199 71 7 - (4) 345 7 (10) - an SEC-registered investment adviser and an affiliate of Columbia Management Investment Advisers, LLC, based in the U.K. RiverSource insurance and annuity products are issued by RiverSource... -

Page 15

Ameriprise Financial, Inc. 2013 Form 10-K -

Page 16

...) 1099 Ameriprise Financial Center, Minneapolis, Minnesota (Address of principal executive offices) Registrant's telephone number, including area code: (612) 671-3131 Securities registered pursuant to Section 12(b) of the Act: Title of each class Common Stock (par value $.01 per share) Securities... -

Page 17

... Director Independence ...Principal Accountant Fees and Services ...176 178 179 179 179 Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities ...Selected Financial Data ...Management's Discussion and Analysis of Financial Condition and Results... -

Page 18

... is located at 55 Ameriprise Financial Center, Minneapolis, Minnesota 55474. We also maintain executive offices in New York City. Ameriprise Financial is a diversified financial services company with a 119 year history of providing financial solutions. We offer a broad range of products and services... -

Page 19

...that we provide through our advisors (e.g., financial planning, investment advisory accounts and retail brokerage services) and products and services that we market directly to consumers or through affinity groups (e.g., personal auto and home insurance). We use Columbia Managementá"¼ as the primary... -

Page 20

...Columbia Management Investment Distributors, Inc. American Enterprise Investment Services Inc. RiverSource Life Insurance Company IDS Property Casualty Insurance Company Ameriprise Certificate Company Ameriprise Trust Company Ameriprise National Trust Bank RiverSource Life Insurance Co. of New... -

Page 21

...) and AEIS (defined below). AMPF Holding Corporation's results of operations are included in our Advice & Wealth Management segment. American Enterprise Investment Services Inc. (''AEIS'') is our registered clearing broker-dealer subsidiary. Brokerage transactions for accounts introduced by AFSI... -

Page 22

... payout rate than our employee advisors as they are responsible for paying their own overhead, staff compensation and other business expenses. In addition, our franchisee advisors pay a franchise association fee and other fees in exchange for the support we offer and the right to use our brand name... -

Page 23

... asset allocation and other financial planning tools. We also offer shares in public non-exchange traded real estate investment trusts, structured notes and other alternative investments issued by unaffiliated companies. We offer trading and portfolio strategy services across a number of fixed... -

Page 24

...investment options and to purchase certain guaranteed benefit or volatility management riders. In addition to RiverSource insurance and annuity products, our advisors offer products of unaffiliated carriers on a limited basis, including variable annuities, life insurance and long term care insurance... -

Page 25

... products. The certificates compete with investments offered by banks, savings and loan associations, credit unions, mutual funds, insurance companies and similar financial institutions. In times of weak performance in the equity markets, certificate sales are generally stronger. In 2013, advisors... -

Page 26

... families, as well as the assets we manage for institutional clients in separately managed accounts, collective funds, hedge funds, the general and separate accounts of the RiverSource Life companies, the assets of IDS Property Casualty and Ameriprise Certificate Company. These investment management... -

Page 27

... options in variable annuity and variable life insurance products, including RiverSource products. The Columbia Management family of funds includes domestic and international equity funds, fixed income funds, cash management funds, balanced funds, specialty funds, absolute return funds and asset... -

Page 28

... our Consolidated Balance Sheets, such as the assets held in the general account of our RiverSource Life companies and assets held by Ameriprise Certificate Company. Our fixed income team manages the general account assets to produce a consolidated and targeted rate of return on investments based on... -

Page 29

... family of funds. Pursuant to distribution agreements with the funds, we offer and sell fund shares on a continuous basis and pay certain costs associated with the marketing and selling of shares. We earn commissions for distributing the Columbia Management funds through sales charges (front-end... -

Page 30

... as well as variable portfolio funds of other companies. RiverSource variable annuity products in force offer a fixed account investment option with guaranteed minimum interest crediting rates ranging up to 4% at December 31, 2013. Contract purchasers can choose to add optional benefit provisions to... -

Page 31

...Property Casualty companies (as defined below under ''Ameriprise Auto & Home Insurance Products''). The primary sources of revenues for this segment are premiums, fees and charges we receive to assume insurance-related risk. We earn net investment income on owned assets supporting insurance reserves... -

Page 32

...to a cap and floor). The policyholder may allocate all or a portion of the policy value to a fixed or indexed account. In 2013, we introduced RiverSource TrioSourceSM universal life insurance with long term care benefits. TrioSource allows clients to allocate a policy's cash value to a fixed account... -

Page 33

... rate increases with respect to these and other existing blocks of long term care insurance policies, subject to regulatory approval. Ameriprise Auto & Home Insurance Products We offer personal auto, home, excess personal liability, travel and specialty insurance products through IDS Property... -

Page 34

... of liabilities and reserves related to our insurance products, see Note 2 to our Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10-K. Financial Strength Ratings Independent rating organizations evaluate the financial soundness and claims-paying ability... -

Page 35

... stock and mutual insurance companies. Competitive factors affecting the sale of annuity and insurance products include distribution capabilities, price, product features, hedging capability, investment performance, commission structure, perceived financial strength, claims-paying ratings, service... -

Page 36

...respect to the net capital requirements and the marketing and trading activities of broker-dealers. Our broker-dealer subsidiaries, as well as our financial advisors and other personnel, must obtain all required state and FINRA licenses and registrations to engage in the securities business and take... -

Page 37

...Investment companies are required by the SEC to adopt and implement written policies and procedures designed to prevent violations of the federal securities laws and to designate a chief compliance officer. Ameriprise Certificate Company pays dividends to the parent company and is subject to capital... -

Page 38

...insurance and securities laws. The Minnesota Department of Commerce, the Wisconsin Office of the Commissioner of Insurance, and the New York State Department of Financial Services (the ''Domiciliary Regulators'') regulate certain of the RiverSource Life companies, and the Property Casualty companies... -

Page 39

..., Item 8 of this Annual Report on Form 10-K for additional information regarding guaranty association assessments. Certain variable annuity and variable life insurance policies offered by the RiverSource Life companies constitute and are registered as securities under the Securities Act of 1933, as... -

Page 40

... to financial holding companies. Parent Company Regulation Ameriprise Financial is a publicly traded company that is subject to SEC and New York Stock Exchange (''NYSE'') rules and regulations regarding public disclosure, financial reporting, internal controls and corporate governance. The... -

Page 41

... conditions and client activity. Downturns and volatility in equity markets can have, and have had, an adverse effect on the revenues and returns from our asset management services, wrap accounts and variable annuity contracts. Because the profitability of these products and services depends on fees... -

Page 42

...interest-sensitive products, such as fixed universal life insurance, fixed annuities and face-amount certificates, and we increase crediting rates on in-force products to keep these products competitive. Because returns on invested assets may not increase as quickly as current interest rates, we may... -

Page 43

... products have guaranteed minimum crediting rates. Due to the long-term nature of the liabilities associated with certain of our businesses, such as long term care and fixed universal life with secondary guarantees as well as fixed annuities and guaranteed benefits on variable annuities, sustained... -

Page 44

... quality of investment advice, investment performance, product offerings and features, price, perceived financial strength, claims-paying ability and credit ratings. Our competitors include broker-dealers, banks, asset managers, insurers and other financial institutions. Many of our businesses face... -

Page 45

... products and services, or the financial industry in general, may increase the number of withdrawals and redemptions or reduce purchases made by our clients, which would adversely impact the levels of our assets under management, revenues and liquidity position. A drop in our investment performance... -

Page 46

... and could result in changes to investment valuations that may materially adversely impact our results of operations or financial condition. Fixed maturity, equity, trading securities and short-term investments, which are reported at fair value on the consolidated balance sheets, represent the... -

Page 47

..., including insurers currently in receiverships, increasing the risk of triggering guaranty fund assessments. For more information regarding assessments from guaranty fund associations, see Note 23 to our Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10... -

Page 48

... underwriting costs that have been deferred on the sale of annuity, life and disability income insurance and, to a lesser extent, direct marketing expenses for personal auto and home insurance, and distribution expenses for certain mutual fund products. For annuity and universal life products, DAC... -

Page 49

For more information regarding DAC, see Part II, Item 7 of this Annual Report on Form 10-K under the heading ''Management's Discussion and Analysis of Financial Condition and Results of Operations - Critical Accounting Policies - Deferred Acquisition Costs and Deferred Sales Inducement Costs'' and ... -

Page 50

... deployment in response to both investor interest and evolution in the financial markets of increasingly sophisticated products, such as those which incorporate automatic asset re-allocation, long/short trading strategies or multiple portfolios or funds, and business-driven hedging, compliance and... -

Page 51

... as our insurance and brokerage subsidiaries and our face-amount certificate company) to pay dividends or make other permitted payments. See Item 1 of this Annual Report on Form 10-K - ''Regulation'' as well as the information contained in Part II, Item 7 under the heading ''Management's Discussion... -

Page 52

... accelerate the timing in which benefits are paid under our insurance policies; significant widespread property damage may materially increase the amount of claims submitted under our property casualty insurance policies; an increase in claims and any resulting increase in claims reserves caused by... -

Page 53

... earnings. In the years ended December 31, 2013, 2012, and 2011, we earned $1.8 billion, $1.6 billion and $1.6 billion, respectively, in distribution fees. Our own Columbia Management family of mutual funds paid a significant portion of these revenues to us in accordance with plans and agreements of... -

Page 54

...2010, called for sweeping changes in the supervision and regulation of the financial services industry designed to provide for greater oversight of financial industry participants, reduce risk in banking practices and in securities and derivatives trading, enhance public company corporate governance... -

Page 55

... on our financial condition and results of operations. Changes in U.S. federal income or estate tax law could make some of our products less attractive to clients. Many of the products we issue or on which our businesses are based (including both insurance products and non-insurance products) enjoy... -

Page 56

... in and the adoption of accounting standards and securities and insurance rating agency processes and standards applicable to our businesses and the financial services industry; and changes in general economic or market conditions. Stock markets in general have experienced volatility that has often... -

Page 57

...including: sales and distribution of mutual funds, annuities, equity and fixed income securities, real estate investment trusts, insurance products, and financial advice offerings; supervision of the Company's financial advisors; administration of insurance claims; security of client information and... -

Page 58

... poor performance histories, higher expenses relative to other investment options and improper fees paid to Ameriprise Financial or its subsidiaries. The action also alleges that the Company breached fiduciary duties under ERISA because it used its affiliate Ameriprise Trust Company as the Plan... -

Page 59

... worth of our common stock through 2014. The share repurchase program does not require the purchase of any minimum number of shares, and depending on market conditions and other factors, these purchases may be commenced or suspended at any time without prior notice. Acquisitions under the share... -

Page 60

... 31, 2013, 2012, 2011, 2010 and 2009 and for the five-year period ended December 31, 2013. On April 30, 2010, we acquired the long-term asset management business of Columbia Management Group. Results presented below include the results of this business after the date of acquisition. The selected... -

Page 61

... strategy: Wealth Management and Asset Management. Our wealth management capabilities are centered on the long-term, personal relationships between our clients and our financial advisors (our ''advisors''). Through our advisors, we offer financial planning, products and services designed to be used... -

Page 62

... our fixed annuities, fixed insurance, deposit products and the fixed portion of variable annuities and variable insurance contracts, the value of deferred acquisition costs (''DAC'') and deferred sales inducement costs (''DSIC'') assets, the values of liabilities for guaranteed benefits associated... -

Page 63

... the related general and administrative expenses are eliminated and the changes in the assets and liabilities related to the CIEs, primarily debt and underlying syndicated loans, are reflected in net investment income. We continue to include the fees in the management and financial advice fees line... -

Page 64

... operations in the numerator, and Ameriprise Financial shareholders' equity, excluding AOCI and the impact of consolidating investment entities using a five-point average of quarter-end equity in the denominator. (2) Critical Accounting Policies The accounting and reporting policies that we use... -

Page 65

... Operations. For annuity and life, disability income and long term care insurance products, key assumptions underlying these long-term projections include interest rates (both earning rates on invested assets and rates credited to contractholder and policyholder accounts), equity market performance... -

Page 66

... Balances, Future Policy Benefits and Claims Fixed Annuities and Variable Annuity Guarantees Fixed annuities and variable annuity guarantees include amounts for fixed account values on fixed and variable deferred annuities, guaranteed benefits associated with variable annuities, equity indexed... -

Page 67

... Life, disability income and long term care insurance includes liabilities for fixed account values on fixed and variable universal life policies, liabilities for indexed accounts of indexed universal life (''IUL'') products, liabilities for unpaid amounts on reported claims, estimates of benefits... -

Page 68

...it is reported. Liabilities for estimates of benefits that will become payable on future claims on term life, whole life, disability income and long term care policies are based on the net level premium method, using anticipated premium payments, mortality and morbidity rates, policy persistency and... -

Page 69

... Consolidated Financial Statements. Sources of Revenues and Expenses Management and Financial Advice Fees Management and financial advice fees relate primarily to fees earned from managing mutual funds, separate account and wrap account assets and institutional investments, as well as fees earned... -

Page 70

... than trading securities and equity method investments, are recognized using the specific identification method on a trade date basis. Premiums Premiums include premiums on auto and home insurance, traditional life and health (disability income and long term care) insurance and immediate annuities... -

Page 71

... to the premium-paying period. For certain mutual fund products, DAC are generally amortized over fixed periods on a straight-line basis adjusted for redemptions. See ''Deferred Acquisition Costs and Deferred Sales Inducement Costs'' under ''Critical Accounting Policies'' for further information on... -

Page 72

...: Years Ended December 31, 2013 Revenues Management and financial advice fees Distribution fees Net investment income Premiums Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Distribution expenses Interest credited to fixed accounts Benefits, claims... -

Page 73

... and wrap account net inflows, partially offset by asset management net outflows. See our discussion on the changes in AUM in our segment results of operations section below. Distribution fees increased $155 million, or 10%, to $1.8 billion for the year ended December 31, 2013 compared to... -

Page 74

... fund returns related to the life contingent benefits associated with GMWB. An increase in expenses related to our auto and home business driven by higher claim and claim adjustment expense reflecting the impact of growth in exposures due to a 29% increase in gross new policies and higher loss cost... -

Page 75

..., 2013 Advice & Wealth Management Net revenues Expenses Operating earnings Asset Management Net revenues Expenses Operating earnings Annuities Net revenues Expenses Operating earnings Protection Net revenues Expenses Operating earnings Corporate & Other Net revenues Expenses Operating loss 2012 (in... -

Page 76

... powers national trust bank. In 2012, we liquidated checking, savings and money market accounts and certificates of deposit and returned all funds to our clients. We also sold Ameriprise Bank's consumer loan portfolio, including first mortgages, home equity loans, home equity lines of credit and... -

Page 77

... ended December 31, 2013 compared to $443 million for the prior year primarily due to strong growth in wrap account assets, increased client activity and continued expense management, partially offset by the impact of low interest rates and lower earnings due to the transition of banking operations... -

Page 78

... Management, Annuities and Protection segments. On April 30, 2010, we completed the acquisition of the long-term asset management business of the Columbia Management Group from Bank of America. The acquisition significantly enhanced the capabilities of the Asset Management segment by increasing... -

Page 79

... 5 Morningstar star ratings Percent of assets with 4 or 5 Morningstar star ratings Mutual fund performance rankings are based on the performance of Class Z fund shares for Columbia branded mutual funds. Only funds with Class Z shares are included. In instances where a fund's Class Z shares do not... -

Page 80

... period's ending balance and all months in the current period. The following table presents managed asset net flows: Years Ended December 31, 2013 Columbia managed asset net flows Threadneedle managed asset net flows Less: Sub-advised eliminations Total managed asset net flows $ 2012 Change 55% NM... -

Page 81

... 453.3 $ 20.0 December 31, 2013 Equity Fixed income Money market Alternative Hybrid and other Total managed assets (1) 2012 $ 275.3 $ 224.1 $ 51.2 196.4 205.2 (8.8) 7.1 6.5 0.6 6.4 6.7 (0.3) 15.6 12.9 2.7 $ 500.8 $ 455.4 $ 45.4 Average ending balances are calculated using an average of the prior... -

Page 82

... investment grade and high yield credit mandates given strong performance in these asset classes, partially offset by new mandates funded in 2013. Threadneedle managed assets increased $19.6 billion, or 15%, during the year ended December 31, 2013 primarily due to market appreciation, as well as net... -

Page 83

...operating basis: Years Ended December 31, 2013 Revenues Management and financial advice fees Distribution fees Net investment income Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Distribution expenses Amortization of deferred acquisition costs General... -

Page 84

...on an operating basis: Years Ended December 31, 2013 Revenues Management and financial advice fees Distribution fees Net investment income Premiums Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Distribution expenses Interest credited to fixed accounts... -

Page 85

... changes and an increase in expenses of approximately $40 million related to higher reserve funding driven by the impact of higher fees from prior year sales with variable annuity guarantees, partially offset by a $31 million benefit from policyholder movement of investments in Portfolio Navigator... -

Page 86

...on an operating basis: Years Ended December 31, 2013 Revenues Management and financial advice fees Distribution fees Net investment income Premiums Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Distribution expenses Interest credited to fixed accounts... -

Page 87

... benefit from a life insurance reserve release in the prior year. The increase in expenses related to our auto and home business was driven by higher claim and claim adjustment expense reflecting the impact of growth in exposures due to a 29% increase in gross new policies and higher loss cost... -

Page 88

...: Years Ended December 31, 2012 Revenues Management and financial advice fees Distribution fees Net investment income Premiums Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Distribution expenses Interest credited to fixed accounts Benefits, claims... -

Page 89

... changes for the year ended December 31, 2012 reflected a $50 million benefit from an adjustment to the model which values the reserves related to living benefit guarantees primarily attributable to prior periods, partially offset by lower bond fund returns related to the life contingent benefits... -

Page 90

... prior year sales with variable annuity guarantees. A $9 million benefit from a life insurance reserve release in 2012. The market impact on DSIC was a benefit of $7 million in 2012 compared to an expense of $2 million in 2011 as a result of favorable equity and bond fund returns in 2012 compared to... -

Page 91

... changes: Years Ended December 31, 2012 Segment Pretax Operating Increase (Decrease) Other revenues Benefits, claims, losses and settlement expenses Amortization of DAC Interest credited to fixed accounts Total expenses Total $ Annuities $ - (32) 41 2 11 (11) $ Protection $ 2011 Annuities Protection... -

Page 92

... wrap account assets increased $12.3 billion, or 12%, compared to the prior year due to net inflows and market appreciation. The following table presents the results of operations of our Advice & Wealth Management segment on an operating basis: Years Ended December 31, 2012 Revenues Management... -

Page 93

... 31, 2012 Equity Fixed income Money market Alternative Hybrid and other Total managed assets by type (1) 2011 $ 209.9 196.5 7.5 9.3 12.3 435.5 $ 224.1 205.2 6.5 6.7 12.9 455.4 $ $ $ $ $ Average ending balances are calculated using an average of the prior period's ending balance and all... -

Page 94

... the changes in Columbia and Threadneedle managed assets: Years Ended December 31, 2012 Columbia Managed Assets Rollforward Retail Funds Beginning assets Mutual fund inflows Mutual fund outflows Net VP/VIT fund flows Net new flows Reinvested dividends Net flows Distributions Market appreciation... -

Page 95

... the year ended December 31, 2012 due to an increase in both Columbia and Threadneedle managed assets. Columbia managed assets increased $4.3 billion, or 1%, in 2012 due to market appreciation, partially offset by net outflows. Columbia retail funds increased $11.5 billion, or 6%, in 2012 due to... -

Page 96

...operating basis: Years Ended December 31, 2012 Revenues Management and financial advice fees Distribution fees Net investment income Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Distribution expenses Amortization of deferred acquisition costs General... -

Page 97

...on an operating basis: Years Ended December 31, 2012 Revenues Management and financial advice fees Distribution fees Net investment income Premiums Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Distribution expenses Interest credited to fixed accounts... -

Page 98

... changes, as well as higher reserve funding related to higher fees from variable annuity guarantees, partially offset by the market impact to DSIC and lower reserve increases resulting from lower sales of immediate annuities with life contingencies. Benefits, claims, losses and settlement expenses... -

Page 99

... fees Net investment income Premiums Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Distribution expenses Interest credited to fixed accounts Benefits, claims, losses and settlement expenses Amortization of deferred acquisition costs General... -

Page 100

...increase in general and administrative expense driven by higher severance expense, compensation related accruals and investment spending, partially offset by a $15 million benefit from a settlement with a third-party service provider. Fair Value Measurements We report certain assets and liabilities... -

Page 101

... the valuation of variable annuity riders and indexed universal life insurance by updating certain contractholder assumptions, adding explicit margins to provide for profit, risk and expenses, and adjusting the rates used to discount expected cash flows to reflect a current market estimate of our... -

Page 102

... broker-dealer subsidiary, American Enterprise Investment Services, Inc. (''AEIS''), our Auto and Home insurance subsidiary, IDS Property Casualty Insurance Company (''IDS Property Casualty''), doing business as Ameriprise Auto & Home Insurance, our transfer agent subsidiary, Columbia Management... -

Page 103

... Life of NY(1)(2) IDS Property Casualty(1)(3) Ameriprise Insurance Company(1)(3) ACC(4)(5) Threadneedle(6) Ameriprise National Trust Bank(7) AFSI(3)(4) Ameriprise Captive Insurance Company(3) Ameriprise Trust Company(3) AEIS(3)(4) RiverSource Distributors, Inc.(3)(4) Columbia Management Investment... -

Page 104

...: 2013 RiverSource Life(1) Ameriprise Bank, FSB(2) ACC Columbia Management Investment Advisers, LLC Columbia Management Investment Services Corporation Threadneedle Ameriprise Trust Company Securities America Financial Corporation(3) IDS Property Casualty Ameriprise Holdings, Inc. Ameriprise Advisor... -

Page 105

... lower funding and purchase of mortgage loans in 2012 and a $225 million increase in cash from changes in credit card receivables, which were sold to Barclays in 2012. See our discussion of the conversion of Ameriprise Bank to a limited powers national trust bank in our Results of Operations section... -

Page 106

...net change in other banking deposits reflecting the liquidation of banking deposits related to the Ameriprise Bank transition. Cash proceeds from issuance of debt, net of issuance costs, was $744 million for the year ended December 31, 2013 compared to none in the prior year. These increases in cash... -

Page 107

...acquisition integration, general and administrative costs, consolidated tax rate, return of capital to shareholders, and excess capital position and financial flexibility to capture additional growth opportunities; other statements about future economic performance, the performance of equity markets... -

Page 108

...generated on our fixed annuities, fixed insurance, brokerage client cash balances, face amount certificate products and the fixed portion of our variable annuities and variable insurance contracts, the value of DAC and DSIC assets, the value of liabilities for guaranteed benefits associated with our... -

Page 109

... Macro hedge program(5) Fixed annuities, fixed insurance and fixed portion of variable annuities and variable insurance products Brokerage client cash balances Certificates Indexed universal life insurance Total Before Hedge Impact $ (40) - 435 23 N/A 458 3 14 134 1 10 $ 580 Hedge Impact Net Impact... -

Page 110

... of the performance of the investment assets. For this reason, when equity prices decline, the returns from the separate account assets coupled with guaranteed benefit fees from annuity holders may not be sufficient to fund expected payouts. In that case, reserves must be increased with a negative... -

Page 111

...invest in fixed rate securities to fund the rate credited to clients. We guarantee an interest rate to the holders of these products. Investment assets and client liabilities generally differ as it relates to basis, repricing or maturity characteristics. Rates credited to clients' accounts generally... -

Page 112

... We pay interest on certain brokerage client cash balances and have the ability to reset these rates from time to time based on prevailing economic and business conditions. We earn revenue to fund the interest paid from interest-earning assets or fees from off-balance sheet deposits at FDIC insured... -

Page 113

... must credit to client accounts. Interest Rate Risk - Indexed Universal Life As mentioned above, most of the proceeds received from IUL insurance are invested in fixed income securities with the return on those investments intended to fund the purchase of call spreads. There are two risks relating... -

Page 114

... during the terms of the treaties. As of December 31, 2013, our largest reinsurance credit risk is related to a long term care coinsurance treaty with life insurance subsidiaries of Genworth Financial, Inc. See Note 7 to our Consolidated Financial Statements for additional information on reinsurance... -

Page 115

...: Ameriprise Financial, Inc. Report of Independent Registered Public Accounting Firm ...Consolidated Statements of Operations - Years ended December 31, 2013, 2012 and 2011 ...Consolidated Statements of Comprehensive Income - Years ended December 31, 2013, 2012 and 2011 ...Consolidated Balance... -

Page 116

Report of Independent Registered Public Accounting Firm To the Board of Directors and Shareholders of Ameriprise Financial, Inc.: In our opinion, the accompanying consolidated balance sheets and the related consolidated statements of operations, comprehensive income, equity, and of cash flows ... -

Page 117

... Ended December 31, 2013 Revenues Management and financial advice fees Distribution fees Net investment income Premiums Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Distribution expenses Interest credited to fixed accounts Benefits, claims, losses... -

Page 118

... during the period Reclassification of net securities gains included in net income Impact on deferred acquisition costs, deferred sales inducement costs, benefit reserves and reinsurance recoverables Total net unrealized gains (losses) on securities Net unrealized gains (losses) on derivatives... -

Page 119

... cash and investments Other assets Other assets of consolidated investment entities, at fair value Total assets Liabilities and Equity Liabilities: Policyholder account balances, future policy benefits and claims Separate account liabilities Customer deposits Short-term borrowings Long-term... -

Page 120

... Number of Additional Consolidated Other Financial, Inc. NonOutstanding Common Paid-In Retained Investment Treasury Comprehensive Shareholders' controlling Shares Shares Capital Earnings Entities Shares Income Equity Interests Balances at January 1, 2011 246,697,892 Comprehensive income (loss): Net... -

Page 121

... Net transfers from (to) separate accounts Surrenders and other benefits Cash paid for purchased options with deferred premiums Issuance of debt, net of issuance costs Repayments of debt Change in short-term borrowings, net Dividends paid to shareholders Repurchase of common shares Exercise of stock... -

Page 122

... operating activities, the change in freestanding derivatives hedging guaranteed minimum withdrawal benefits (''GMWB'') and guaranteed minimum accumulation benefits (''GMAB'') liabilities was reclassified from ''Policyholder account balances, future policy benefits and claims'' to ''Derivatives, net... -

Page 123

... to receive the entity's returns) or has equity investors that do not provide sufficient financial resources for the entity to support its activities. A VIE is required to be assessed for consolidation under two models: • If the VIE is a money market fund or is an investment company, or has the... -

Page 124

... cost basis of the security. The significant inputs to cash flow projections consider potential debt restructuring terms, projected cash flows available to pay creditors and the Company's position in the debtor's overall capital structure. For structured investments (e.g., residential mortgage... -

Page 125

... loans, net reflect the Company's interest in commercial mortgage loans and consumer loans secured by residential properties, less the related allowance for loan losses. Policy and Certificate Loans Policy and certificate loans include life insurance policy, annuity and investment certificate loans... -

Page 126

... Company receives investment management fees, mortality and expense risk fees, guarantee fees and cost of insurance charges from the related accounts. Included in separate account assets and liabilities is the value of the units in issue of the pooled pension funds that are offered by Threadneedle... -

Page 127

... developed or purchased software are carried at cost less accumulated depreciation or amortization and are reflected within other assets. The Company generally uses the straight-line method of depreciation and amortization over periods ranging from three to 39 years. At December 31, 2013 and 2012... -

Page 128

... insurance and annuity businesses. The portion of these costs which are incremental and direct to the acquisition of a new or renewal insurance policy or annuity contract are deferred. Significant costs capitalized by the Company include sales based compensation related to the acquisition of new... -

Page 129

The client asset value growth rates are the rates at which variable annuity and variable universal life (''VUL'') insurance contract values invested in separate accounts are assumed to appreciate in the future. The rates used vary by equity and fixed income investments. Management reviews and, where... -

Page 130

... and interest rates. Life and Health Insurance Life and health insurance includes liabilities for fixed account values on fixed and variable universal life policies, liabilities for indexed accounts of IUL products, liabilities for unpaid amounts on reported claims, estimates of benefits payable on... -

Page 131

... (e.g. cost of insurance charges, contractual administrative charges, similar fees and investment margin). See Note 10 for information regarding the liability for contracts with secondary guarantees. Liabilities for unpaid amounts on reported life insurance claims are equal to the death benefits... -

Page 132

... charges on fixed and variable universal life insurance and annuities, which are recognized when assessed. Net Investment Income Net investment income primarily includes interest income on fixed maturity securities classified as Available-for-Sale, mortgage loans, policy and certificate loans... -

Page 133

... charges, net of reinsurance and cost of reinsurance for UL insurance products and variable annuity guaranteed benefit rider charges. These charges are recognized as revenue when assessed. The Company also records revenue related to consolidated pooled investment vehicles managed by Threadneedle... -

Page 134

... residual returns. For the pooled investment vehicles which are VREs, the Company consolidates the structure when it has a controlling financial interest. The Company also provides investment advisory, distribution and other services to the Columbia and Threadneedle mutual fund families. The Company... -

Page 135

... balances of assets and liabilities held by consolidated investment entities measured at fair value on a recurring basis: December 31, 2013 Level 1 Assets Investments: Corporate debt securities Common stocks Other investments Syndicated loans Total investments Receivables Other assets Total assets... -

Page 136

... of changes in Level 3 assets and liabilities held by consolidated investment entities measured at fair value on a recurring basis: Corporate Debt Securities Balance, January 1, 2013 Total gains (losses) included in: Net income Other comprehensive income (loss) Purchases Sales Issues Settlements... -

Page 137

... and liabilities held by consolidated investment entities: December 31, 2013 Fair Value Other assets (in millions) $ 1,936 Valuation Technique Discounted cash flow/market comparables Discounted cash flow Unobservable Input Equivalent yield Expected rental value (per square foot) Annual default rate... -

Page 138

... yield and expected rental value of the property may include: rental cash flows, current occupancy, historical vacancy rates, tenant history and assumptions regarding how quickly the property can be occupied and at what rental rates. Management reviews the valuation report and assumptions used... -

Page 139

... in net investment income related to changes in the fair value of financial assets and liabilities for which the fair value option was elected were $28 million, $(85) million and $(122) million for the years ended December 31, 2013, 2012 and 2011, respectively. The majority of the syndicated loans... -

Page 140

... $ 305 97 20 708 377 4,457 5,964 $ 5. Investments The following is a summary of Ameriprise Financial investments: December 31, 2013 Available-for-Sale securities, at fair value Mortgage loans, net Policy and certificate loans Other investments Total $ 2012 (in millions) 30,310 $ 31,472 3,510 3,609... -

Page 141

... 31, 2013 and 2012, fixed maturity securities comprised approximately 85% of Ameriprise Financial investments. Rating agency designations are based on the availability of ratings from Nationally Recognized Statistical Rating Organizations (''NRSROs''), including Moody's Investors Service (''Moody... -

Page 142

...current period net income due to sales of Available-for-Sale securities and due to the reclassification of noncredit other-than-temporary impairment losses to credit losses; and (iii) other items primarily consisting of adjustments in asset and liability balances, such as DAC, DSIC, benefit reserves... -

Page 143

...-than-temporary impairments for the years ended December 31, 2013, 2012 and 2011 primarily related to credit losses on non-agency residential mortgage backed securities. Available-for-Sale securities by contractual maturity at December 31, 2013, were as follows: Amortized Cost Due Due Due Due within... -

Page 144

... receivables include commercial mortgage loans, syndicated loans, consumer loans, policy loans, certificate loans and margin loans. See Note 2 for information regarding the Company's accounting policies related to loans and the allowance for loan losses. Allowance for Loan Losses The following... -

Page 145

... the acquisition date. Credit Quality Information Nonperforming loans, which are generally loans 90 days or more past due, were $22 million and $7 million as of December 31, 2013 and 2012, respectively. All other loans were considered to be performing. Commercial Mortgage Loans The Company reviews... -

Page 146

... 31, 2013 18% 1 17 1 21 36 6 100% 2012 17% 1 18 2 24 33 5 100% Syndicated Loans The Company's syndicated loan portfolio is diversified across industries and issuers. The primary credit indicator for syndicated loans is whether the loans are performing in accordance with the contractual terms of the... -

Page 147

... liabilities related to the RiverSource TrioSourceSM universal life product launched in 2013. Generally, the maximum amount of life insurance risk retained by the Company is $1.5 million on a single life and $1.5 million on any flexible premium survivorship life policy. Risk on fixed and variable... -

Page 148

...for the years ended December 31, 2013, 2012 and 2011. The changes in the carrying amount of goodwill reported in the Company's main operating segments were as follows: Advice & Wealth Management Balance at January 1, 2012 Foreign currency translation Purchase price adjustments Balance at December 31... -

Page 149

... 19 9. Deferred Acquisition Costs and Deferred Sales Inducement Costs In the third quarter of the year, management conducts its annual review of insurance and annuity valuation assumptions relative to current experience and management expectations. To the extent that expectations change as a result... -

Page 150

... Payout contracts guarantee a fixed income payment for life or the term of the contract. The Company generally invests the proceeds from the annuity payments in fixed rate securities. The Index 500 Annuity, the Company's EIA product, is a single premium deferred fixed annuity. The contract is issued... -

Page 151

...above the minimum guarantee for funds allocated to the indexed account is linked to the performance of the S&P 500 Index (subject to a cap and floor). The policyholder may allocate all or a portion of the policy value to a fixed or indexed account. The Company also offers term life insurance as well... -

Page 152

... policy value to cover the monthly deductions and charges. The following table provides information related to variable annuity guarantees for which the Company has established additional liabilities: December 31, 2013 Variable Annuity Guarantees by Benefit Type(1) GMDB: Return of premium... -

Page 153

... recognized on assets transferred to separate accounts for the years ended December 31, 2013, 2012 and 2011. 12. Customer Deposits Customer deposits consisted of the following: December 31, 2013 Fixed rate certificates Stock market certificates Stock market embedded derivative reserve Other Less... -

Page 154

... fixed and variable rate securities. Certain investment certificate products have returns tied to the performance of equity markets. The Company guarantees the principal for purchasers who hold the certificate for the full 52-week term and purchasers may participate in increases in the stock market... -

Page 155

... notes due 2066 and credit facility contain various administrative, reporting, legal and financial covenants. The Company was in compliance with all such covenants at both December 31, 2013 and 2012. At December 31, 2013, future maturities of Ameriprise Financial long-term debt were as follows... -

Page 156

... letters of credit issued against this facility were $2 million as of December 31, 2013. 14. Fair Values of Assets and Liabilities GAAP defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at... -

Page 157

... the balances of assets and liabilities of Ameriprise Financial measured at fair value on a recurring basis: December 31, 2013 Level 1 Assets Cash equivalents Available-for-Sale securities: Corporate debt securities Residential mortgage backed securities Commercial mortgage backed securities Asset... -

Page 158

...Policyholder account balances, future policy benefits and claims: EIA embedded derivatives IUL embedded derivatives GMWB and GMAB embedded derivatives Total policyholder account balances, future policy benefits and claims Customer deposits Other liabilities: Interest rate derivative contracts Equity... -

Page 159

... Purchases Sales Issues Settlements Transfers into Level 3 Transfers out of Level 3 Balance, December 31, 2013 Changes in unrealized gains (losses) relating to assets and liabilities held at December 31, 2013 included in: Net investment income Interest credited to fixed accounts Benefits, claims... -

Page 160

... income Purchases Sales Issues Settlements Transfers into Level 3 Transfers out of Level 3 Balance, December 31, 2011 Changes in unrealized gains (losses) relating to assets and liabilities held at December 31, 2011 included in: Net investment income Benefits, claims, losses and settlement expenses... -

Page 161

... fair value hierarchy. Assets Cash Equivalents Cash equivalents include highly liquid investments with original maturities of 90 days or less. Actively traded money market funds are measured at their net asset value (''NAV'') and classified as Level 1. The Company's remaining cash equivalents are... -

Page 162

... uncollateralized derivative assets was immaterial at December 31, 2013 and 2012. See Note 15 and Note 16 for further information on the credit risk of derivative instruments and related collateral. Liabilities Policyholder Account Balances, Future Policy Benefits and Claims The Company values the... -

Page 163

... basis. December 31, 2013 Carrying Value Financial Assets Mortgage loans, net Policy and certificate loans Receivables Restricted and segregated cash Other investments and assets Financial Liabilities Policyholder account balances, future policy benefits and claims Investment certificate reserves... -

Page 164

... restrictions on transfer and lack of liquidity in the primary market for these assets. Policyholder Account Balances, Future Policy Benefits and Claims The fair value of fixed annuities, in deferral status, is determined by discounting cash flows using a risk neutral discount rate with adjustments... -

Page 165

Investment Certificate Reserves The fair value of investment certificate reserves is determined by discounting cash flows using discount rates that reflect current pricing for assets with similar terms and characteristics, with adjustments for early withdrawal behavior, penalty fees, expense margin ... -

Page 166

... the Company's liabilities subject to master netting arrangements: December 31, 2013 Gross Amounts Not Offset in the Gross Gross Amounts Amounts of Liabilities Consolidated Balance Sheets Amounts of Offset in the Presented in the Recognized Consolidated Consolidated Financial Cash Securities Net... -

Page 167

...balances, future policy benefits and claims Other liabilities Policyholder account balances, future policy benefits and claims Other liabilities Customer deposits Other liabilities Other liabilities 21 8 5 - - 2 IUL IUL embedded derivatives Other assets N/A 27 - 6 - 13 125 1 45 Stock market... -

Page 168

... Bank assets Tax hedge Interest rate lock commitments Seed money Equity Macro hedge program IUL IUL embedded derivatives EIA EIA embedded derivatives Stock market certificates Stock market certificates embedded derivatives Seed money Ameriprise Financial Franchise Advisor Deferred Compensation Plan... -

Page 169

... activities. The gross notional amount of these derivative contracts was $710 million at December 31, 2013. EIA, IUL and stock market certificate products have returns tied to the performance of equity markets. As a result of fluctuations in equity markets, the obligation incurred by the Company... -

Page 170

...2012 (in millions) $ (11) 14 (1) (4) $ (2) 2011 $ 18 (10) (34) 15 (11) $ $ Currently, the longest period of time over which the Company is hedging exposure to the variability in future cash flows is 22 years and relates to forecasted debt interest payments. Fair Value Hedges In 2010, the Company... -

Page 171

... (''Advisor Group Deferral Plan'') and the Threadneedle Equity Incentive Plan (''EIP''). The components of the Company's share-based compensation expense, net of forfeitures, were as follows: December 31, 2013 Stock option Restricted stock(1) Restricted stock units Liability awards Total (1) 2012... -

Page 172

... age and length of service. Compensation expense for restricted stock awards is based on the market price of Ameriprise Financial common stock on the date of grant and is amortized on a straight-line basis over the vesting period. Quarterly dividends are paid on restricted stock, as declared by the... -

Page 173

... in cases of death, disability and qualified retirement. Compensation expense related to the Company match is recognized on a straight-line basis over the vesting period. Dividend equivalents are issued on deferrals into the Ameriprise Financial Stock Fund and the Company match. Dividend equivalents... -

Page 174

... date fair value for franchise advisor and advisor group deferrals during 2013, 2012 and 2011 was $80.77, $54.98 and $52.72, respectively. Performance Share Units Under the 2005 ICP , the Company's Executive Leadership Team may be awarded a target number of performance share units (''PSUs''). PSUs... -

Page 175

..., 1.8 million and 1.7 million treasury shares, respectively, for restricted stock award grants and issuance of shares vested under the Ameriprise Financial Franchise Advisor Deferred Compensation Plan. For the years ended December 31, 2012 and 2011, the Company reacquired 0.3 million and 0.3 million... -

Page 176

... transfer of funds exist under regulatory requirements applicable to certain of the Company's subsidiaries. At December 31, 2013, the aggregate amount of unrestricted net assets was approximately $1.9 billion. The National Association of Insurance Commissioners (''NAIC'') defines Risk-Based Capital... -

Page 177

... for asset managers. The Company has four broker-dealer subsidiaries, American Enterprise Investment Services Inc., Ameriprise Financial Services, Inc., RiverSource Distributors, Inc. and Columbia Management Investment Distributors, Inc. The broker-dealers are subject to the net capital requirements... -

Page 178

...of the Company's deferred income tax assets and liabilities, which are included net within other assets or other liabilities on the Consolidated Balance Sheets, were as follows: December 31, 2013 Deferred income tax assets Liabilities for future policy benefits and claims Investment related Deferred... -

Page 179

...Net income tax provision (benefit) $ (344) - 24 3 (317) 2012 (in millions) $ 238 4 (9) 7 $ 240 2011 $ 90 (15) (28) (1) 46 $ $ 22. Retirement Plans and Profit Sharing Arrangements Defined Benefit Plans Pension Plans The Company's U.S. non-advisor employees are generally eligible for the Ameriprise... -

Page 180

... annuity payments or a lump sum payout at vested termination, retirement, death or disability. The Retirement Plan's year-end is September 30. In addition, the Company sponsors the Ameriprise Financial Supplemental Retirement Plan (the ''SRP''), an unfunded non-qualified deferred compensation plan... -

Page 181

... net periodic benefit cost for pension plans were as follows: 2013 Discount rates Rates of increase in compensation levels Expected long-term rates of return on assets 3.45% 4.36 7.62 2012 4.15% 4.27 7.69 2011 4.75% 4.25 8.00 In developing the expected long-term rate of return on assets, management... -

Page 182

...basis: December 31, 2013 Asset Category Equity securities: U.S. large cap stocks U.S. small cap stocks Non-U.S. large cap stocks Non-U.S. small cap stocks Emerging markets Debt securities: U.S. investment grade bonds U.S. high yield bonds Non-U.S. investment grade bonds Real estate investment trusts... -

Page 183

... basis: Real Estate Investment Trusts $ (in millions) 8 1 2 - 11 - 1 12 - 2 (12) $ 2 $ Hedge Funds $ 9 - 11 (8) 12 1 5 18 2 - - 20 Asset Category Balance at January 1, 2011 Actual return on plan assets: Relating to assets still held at the reporting date Purchases Sales Balance at December 31, 2011... -

Page 184

...years of service, or upon retirement at or after age 65, disability or death while employed. The Company's defined contribution plan expense was $35 million, $36 million and $33 million in 2013, 2012 and 2011, respectively. Threadneedle Profit Sharing Plan On an annual basis, Threadneedle employees... -

Page 185

... Consumer mortgage loan commitments Consumer lines of credit Affordable housing partnerships Total funding commitments $ (in millions) 71 $ 542 4 137 754 $ 2012 76 627 5 144 852 $ Guarantees The Company's life and annuity products all have minimum interest rate guarantees in their fixed accounts... -

Page 186

...including: sales and distribution of mutual funds, annuities, equity and fixed income securities, real estate investment trusts, insurance products, and financial advice offerings; supervision of the Company's financial advisors; administration of insurance claims; security of client information and... -

Page 187

... of 2011, the Company sold Securities America to Ladenburg Thalmann Financial Services, Inc. The components of loss from discontinued operations, net of tax, were as follows: Years Ended December 31, 2013 Total net revenues Income (loss) from discontinued operations Gain on sale Income tax benefit... -

Page 188

...based on a rate times volume or fixed basis. The Advice & Wealth Management segment provides financial planning and advice, as well as full-service brokerage services, primarily to retail clients through the Company's advisors. These services are centered on long-term, personal relationships between... -

Page 189

... benefits to reflect a current estimate of the Company's life insurance subsidiary's nonperformance spread. Integration and restructuring charges primarily relate to the Company's acquisition of the long-term asset management business of Columbia Management Group on April 30, 2010. The costs... -

Page 190

..., 2013 2012 (in millions) 2011 Operating earnings: Advice & Wealth Management Asset Management Annuities Protection Corporate & Other Total segment operating earnings Net realized gains Net income (loss) attributable to noncontrolling interests Market impact on variable annuity guaranteed benefits... -

Page 191

... income Diluted Income from continuing operations Income (loss) from discontinued operations Net income Weighted average common shares outstanding: Basic Diluted Cash dividends declared per common share Common share price: High Low $ $ $ 9/30 6/30 3/31 12/31 9/30 2012 6/30 3/31 (in millions, except... -

Page 192

... and Chief Financial Officer, assessed the effectiveness of the Company's internal control over financial reporting as of December 31, 2013. In making this assessment, the Company's management used the criteria set forth by the 1992 Committee of Sponsoring Organizations of the Treadway Commission in... -

Page 193

...Mr. Berman served as Executive Vice President and Chief Financial Officer of AEFC, a position he held since January 2003. From April 2001 to January 2004, Mr. Berman served as Corporate Treasurer of American Express. Donald E. Froude - President - The Personal Advisors Group Mr. Froude (58) has been... -

Page 194

... as Vice President - Business Planning and Communications for the Group President, Global Financial Services at American Express. Colin Moore - Executive Vice President and Global Chief Investment Officer Mr. Moore (55) has been our Executive Vice President and Global Chief Investment Officer since... -

Page 195

...2012. Prior to that time, he served as President - Insurance and Chief Strategy Officer since February 2008 and, as Senior Vice President - Strategy and Business Development since September 2005. Prior to that, Mr. Woerner served as Senior Vice President - Strategic Planning and Business Development... -

Page 196

...303 shares of common stock issuable under the Ameriprise Financial Franchise Advisor Deferred Compensation Plan. Descriptions of our equity compensation plans can be found in Note 17 to our Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10-K. Information... -

Page 197

... I - Condensed Financial Information of Registrant (Parent Company Only) All other financial schedules are not required under the related instructions, or are inapplicable and therefore have been omitted. 3. Exhibits: The list of exhibits required to be filed as exhibits to this report are listed on... -

Page 198

... and stead, to sign and affix the undersigned's name as such director and/or officer of said corporation to an Annual Report on Form 10-K or other applicable form, and all amendments thereto, to be filed by such corporation with the Securities and Exchange Commission, Washington, D.C., under the... -

Page 199

Date: February 27, 2014 By /s/ W. Walker Lewis W. Walker Lewis Director Date: February 27, 2014 By /s/ Siri S. Marshall Siri S. Marshall Director Date: February 27, 2014 By /s/ Jeffrey Noddle Jeffrey Noddle Director Date: February 27, 2014 By /s/ H. Jay Sarles H. Jay Sarles Director Date: ... -

Page 200

... Independent Registered Public Accounting Firm on Financial Statement Schedule To the Board of Directors and Shareholders of Ameriprise Financial, Inc.: Our audits of the consolidated financial statements and of the effectiveness of internal control over financial reporting referred to in our report... -

Page 201

Schedule I - Condensed Financial Information of Registrant (Parent Company Only) Condensed Statements of Operations ...Condensed Statements of Comprehensive Income ...Condensed Balance Sheets ...Condensed Statements of Cash Flows ...Notes to Condensed Financial Information of Registrant ...F-3 F-4 ... -

Page 202

... Information of Registrant Condensed Statements of Operations (Parent Company Only) December 31, 2013 Revenues Management and financial advice fees Distribution fees Net investment income Other revenues Total revenues Banking and deposit interest expense Total net revenues Expenses Benefits, claims... -

Page 203

... during the period Reclassification of net securities gains included in net income Impact on deferred acquisition costs, deferred sales inducement costs, benefit reserves and reinsurance recoverables Total net unrealized gains (losses) on securities Net unrealized gains (losses) on derivatives... -

Page 204

...Condensed Financial Information of Registrant Condensed Balance Sheet (Parent Company Only) December 31, 2013 2012 (in millions, except share amounts) Assets Cash and cash equivalents Investments Loans to subsidiaries Due from subsidiaries Receivables Land, buildings, equipment, and software, net of... -

Page 205

... Cash paid for purchased options with deferred premiums Cash received for purchased options with deferred premiums Issuances of debt, net of issuance costs Repayments of debt Exercise of stock options Excess tax benefits from share-based compensation Other, net Net cash used in financing activities... -

Page 206

... fee revenue is reflected in equity in earnings of subsidiaries. The change in fair value of derivatives used to economically hedge exposure to equity price risk of Ameriprise Financial, Inc. common stock granted as part of the Ameriprise Financial Franchise Advisor Deferred Compensation Plan... -

Page 207

...Annual Report on Form 10-K, File No. 1-32525, filed on February 29, 2008). Ameriprise Financial Performance Cash Unit Plan Supplement to the Long Term Incentive Award Program Guide (incorporated by reference to Exhibit 10.1 of the Quarterly Report on Form 10-Q, File No. 1-32525, filed on May 2, 2011... -

Page 208

... and JPMorgan Chase Bank, N.A., as Co-Documentation Agents (incorporated by reference to Exhibit 10.1 to the Current Report on Form 8-K, File No. 1-32525, filed on October 1, 2013). Capital Support Agreement by and between Ameriprise Financial, Inc. and Ameriprise Certificate Company, dated as of... -

Page 209

... 500 Index (S&P 500® Index), an unmanaged index of common stocks, is frequently used as a general measure of market performance. The Index re ects reinvestment of all distributions and changes in market prices, but excludes brokerage commissions or other fees. The S&P 500 Financials Index measures... -

Page 210

... Ameriprise Financial Center 707 2nd Avenue South Minneapolis, MN 55474 612.671.3131 7 World Trade Center 250 Greenwich Street, Suite 3900 New York, NY 10007 Information Available to Shareholders Copies of our company's Annual Report on Form 10-K, proxy statement, press releases and other documents... -

Page 211

...President, Corporate Communications and Community Relations Colin Moore Executive Vice President, Global Chief Investment Officer Kim M. Sharan President, Financial Planning and Wealth Strategies and Chief Marketing Officer Joseph E. Sweeney President, Advice & Wealth Management Products and Service... -

Page 212

Financial Planning | Retirement | Investments | Insurance ameriprise.com © 2014 Ameriprise Financial, Inc. All rights reserved. 400425 K (2/14)