eBay 2006 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2006 eBay annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

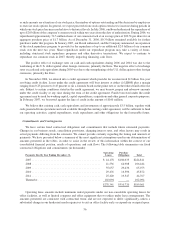

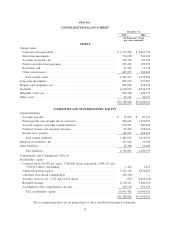

Recent Accounting Pronouncements

In July 2006, the Financial Accounting Standards Board (“FASB”) issued Financial Interpretation No. 48,

“Accounting for Uncertainty in Income Taxes-an interpretation of FASB Statement No. 109” (“FIN 48”), which is a

change in accounting for income taxes. Among other provisions, FIN 48: specifies how tax benefits for uncertain

tax positions are to be recognized, measured, and derecognized in financial statements; requires certain disclosures

of uncertain tax matters; specifies how reserves for uncertain tax positions should be classified on the balance sheet;

and provides transition and interim-period guidance. FIN 48 is effective for fiscal years beginning after Decem-

ber 15, 2006 and as a result, is effective for us in the first quarter of 2007. We have not yet completed our evaluation

of the impact of adoption on our consolidated financial statements.

In September 2006, the FASB issued SFAS No. 157, “Fair Value Measurements” (FAS 157). FAS 157

establishes a framework for measuring fair value and expands disclosures about fair value measurements. The

changes to current practice resulting from the application of this statement relate to the definition of fair value, the

methods used to measure fair value, and the expanded disclosures about fair value measurements. We will be

required to adopt the provisions on FAS 157 beginning with our first quarter ending March 31, 2007. We do not

believe that the adoption of the provisions of FAS 157 will materially impact our consolidated financial statements.

Effective December 31, 2006, we adopted the recognition and disclosure provisions of SFAS No. 158,

“Employers Accounting for Defined Benefit Pension and Other Postretirement Plans — an amendment of FASB

Statements No. 87, 88, 106, and 132(R),” (FAS 158). These provisions did not materially impact our consolidated

financial statements. FAS 158 requires an employer to recognize the over-funded or under-funded status of a

defined benefit pension and other postretirement plan (other than a multiemployer plan) as an asset or liability in its

statement of financial position and to recognize changes in that funded status in the year in which the changes occur

through comprehensive income of a business entity. This statement also requires plan assets and obligations to be

measured as of the employer’s balance sheet date. The measurement provision of this statement will be effective for

years beginning after December 15, 2008 with early adoption encouraged. We have not yet adopted the

measurement date provisions of this statement.

In 2006, we adopted Staff Accounting Bulletin No. 108, “Considering the Effects of Prior Year Misstatements

When Quantifying Misstatements in Current Year Financial Statements” (SAB 108), which provides interpretive

guidance on how the effects of the carryover or reversal of prior year misstatements should be considered in

quantifying a current year misstatement. The adoption of SAB 108 did not impact our consolidated financial

statements.

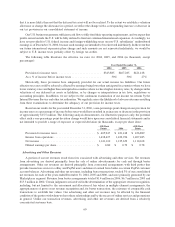

ITEM 7A: QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Interest Rate Risk

The primary objective of our investment activities is to preserve principal while at the same time maximizing

yields without significantly increasing risk. To achieve this objective, we maintain our portfolio of cash equivalents

and short-term and long-term investments in a variety of securities, including government and corporate securities

and money market funds. These securities are generally classified as available for sale and consequently are

recorded on the balance sheet at fair value with unrealized gains or losses reported as a separate component of

accumulated other comprehensive income (loss), net of estimated tax.

Investments in both fixed-rate and floating-rate interest-earning instruments carry varying degrees of interest

rate risk. The fair market value of our fixed-rate securities may be adversely impacted due to a rise in interest rates.

In general, securities with longer maturities are subject to greater interest-rate risk than those with shorter

maturities. While floating rate securities generally are subject to less interest-rate risk than fixed-rate securities,

floating-rate securities may produce less income than expected if interest rates decrease. Due in part to these factors,

our investment income may fall short of expectations or we may suffer losses in principal if securities are sold that

have declined in market value due to changes in interest rates. As of December 31, 2006, our fixed-income

investments earned a pretax yield of approximately 4.7%, with a weighted average maturity of two months. If

interest rates were to instantaneously increase (decrease) by 100 basis points, the fair market value of our total

investment portfolio could decrease (increase) by approximately $1.3 million.

62