TD Bank 2002 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2002 TD Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

|

|

3

TO OUR SHAREHOLDERS

To our shareholders

A Look Back

2002 was a difficult year for the Bank.

Capital markets continued to struggle and for the third straight

year North America’s major stock market indices reported losses,

representing the longest continuous down stretch since the end

of the Second World War. In addition, several high profile cases

of corporate malfeasance were uncovered.

Figuratively speaking, investor confidence was brought to its

knees.

The after-effects of the telecom bubble bursting resonated well

into 2002 and the utilities sector in the U.S. and U.K. domestic

markets suffered a rapid and unprecedented deterioration in the

latter part of the year.

All of these events had a severe impact on our wholesale

banking business.

Consequently, our financial results for the year were mixed

and unsatisfactory overall.

Swift and Decisive Action

We had no choice but to move swiftly and aggressively to change

the risk profile of the Bank, and overhaul our corporate lending

strategy.

Our corporate loan book was divided into core and non-core

relationships. Loans in the non-core book are being exited, a

process that we expect to substantially complete over the next

three-year period. Core client relationships will be strengthened.

Changes were made to our lending standards, and our

procedures and practices. We intend to reduce the total amount

of capital available for corporate lending and have implemented

an enhanced credit framework with stricter industry, portfolio

and name concentration limits. A new organizational structure

has been put in place to lead and support these initiatives, and

lines of responsibility and accountability have been made clearer.

Looking ahead, we are confident that these changes have

dramatically and fundamentally reduced our risk profile, and

positioned our wholesale banking business for renewed growth

and performance in the years ahead.

Additionally, these moves have accelerated our transition

towards focusing more of our financial and intellectual capital on

our retail businesses, which are less volatile and where we have

a leading Canadian position and key competitive advantages with

our service model.

In the near term, we expect to derive 70% of our earnings

from this area of our business, ultimately growing to reach our

goal of 80% of our total earnings mix over the longer-term.

Personal and Commercial Banking

The integration of the Canada Trust franchise with our TD Bank

Financial Group retail network, the largest merger in Canadian

banking history, is now essentially complete.

TD Canada Trust revenue grew during 2002 and we generated

good increases in a number of key product segments. Our

Customer Satisfaction Index reached a record high at year end,

which we believe is a testament to the hard work and dedication

of our employees.

At year end, TD Canada Trust's overall share of its market was

21.46 percent, compared to 21.86 percent a year ago.

Notwithstanding this slight overall decline and the challenges

presented by branch integration, our share of the market is stable,

close to pre-merger levels and well within our expectations.

This year, we will direct much of our attention to streamlining

our processes and investing in our infrastructure to support our

service model. In doing so, we expect to realize improved

operational and cost efficiencies.

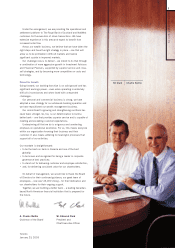

Chairman of the Board

President and Chief Executive Officer

A. Charles Baillie

W. Edmund Clark

Our results for 2002 did not measure up to

expectations or reflect our capabilities. Looking

ahead, we understand our challenge very

clearly – to demonstrate that we can deliver

consistent value for our shareholders.