National Grid 2006 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2006 National Grid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

|

|

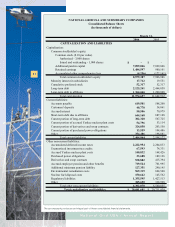

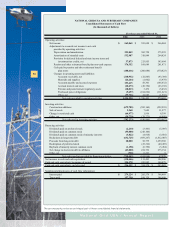

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued)

13. Derivatives:

The Company accounts for derivative financial instruments under SFAS No. 133, “Accounting for

Derivatives and Hedging Activities,” and SFAS No. 149, “Amendment of SFAS No. 133 on

Derivative Instruments and Hedging Activities,” as amended. Under the provisions of SFAS No.

133, all derivatives except those qualifying for the normal purchase/normal sale exception are rec-

ognized on the balance sheet at their fair value. Fair value is determined using current quoted

market prices. If a contract is designated as a cash flow hedge, the change in its market value is

generally deferred as a component of other comprehensive income until the transaction it is hedg-

ing is completed. Conversely, the change in the market value of a derivative not designated as a

cash flow hedge is deferred as a regulatory asset or liability. A cash flow hedge is a hedge of a

forecasted transaction or the variability of cash flows to be received or paid related to a recog-

nized asset or liability. To qualify as a cash flow hedge, the fair value changes in the derivative

must be expected to offset 80% to 125% of the changes in fair value or cash flows of the hedged

item. The Company also has purchase power agreements with non-affiliates for the purchase of

power and capacity for resale to its retail customers. These agreements generally have no notional

amounts and do not meet the definition of a derivative under SFAS No. 133.

14. Comprehensive Income (Loss):

Comprehensive income (loss) is the change in the equity of a company, not including those

changes that result from shareholder transactions. While the primary component of comprehen-

sive income (loss) is reported net income, the other components of comprehensive income (loss)

relate to additional minimum pension liability recognition, deferred gains and losses associated

with hedging activity, and unrealized gains and losses associated with certain investments held as

available for sale (see Note D – “Accumulated Other Comprehensive Income (Loss)”).

15. Additional Minimum Pension Liability:

Additional minimum pension liability (AML) is recognized under SFAS No. 87, “Employers’

Accounting for Pensions.” Consistent with current rate agreements, Niagara Mohawk recovers all

costs associated with its qualified pension plan due to the nature of its rate plan and has recorded

a regulatory asset as an off-set to the qualified plan AML. The AML for the non-qualified plan is

off-set through an adjustment to accumulated other comprehensive income.

The additional minimum pension liability for the Company’s other subsidiaries is recognized in the

balance sheet as a liability with an offsetting charge to other comprehensive income.

16. New Accounting Standards:

SFAS 123R

In December 2004, the FASB issued SFAS No. 123R, “Share-Based Payment.” This standard

addresses the accounting for transactions in which a company receives employee services in

exchange for (a) equity instruments of the company or (b) liabilities that are based on the fair value

of the company’s equity instruments or that may be settled by the issuance of such equity instru-

ments. This standard also eliminates the ability to account for share-based compensation transac-

tions using Accounting Principles Board Opinion (APB) No. 25, “Accounting for Stock Issued to

Employees,” and requires that such transactions be accounted for using a fair-value-based

method. The standard is effective for fiscal years beginning after June 15, 2005. The adoption of

this statement on April 1, 2006 did not have a material impact on the Company’s financial posi-

tion, results of operations, or cash flows.

FIN 47

In March 2005, the FASB issued Interpretation No. 47, “Accounting for Conditional Asset

Retirement Obligations,” (FIN 47). FIN 47 will result in (a) more consistent recognition of liabilities

relating to asset retirement obligations, (b) more information about expected future cash outflows

associated with those obligations and (c) more information about investments in long-lived assets

because additional asset retirement costs will be recognized as part of the carrying amounts of

the assets.

39

National Grid USA / Annual Report