Airtran 2002 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2002 Airtran annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51

|

|

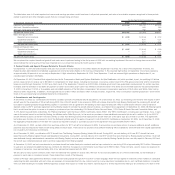

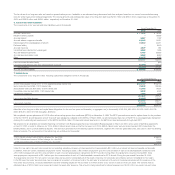

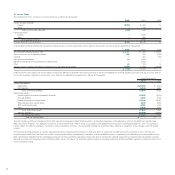

At December 31, 2002, we had NOL carryforwards for income tax purposes of approximately $116 million that begin to expire in 2012. In addition, our AMT credit carryforwards for

income tax purposes were $3.3 million.

Prior to the Airways Corporation merger, Airways Corporation generated NOL carryforwards of $23.1 million. The use of preacquisition NOL carryforwards is subject to limitations

imposed by the Internal Revenue Code. We do not anticipate that these limitations will affect utilization of the carryforwards prior to expiration. For financial reporting purposes, a

valuation allowance of $8.1 million was recognized to offset the deferred tax assets related to those carryforwards. When realized, the tax benefit for those items will be applied to

reduce goodwill related to the acquisition of Airways Corporation. During 2001, we utilized $5.9 million of Airways Corporation’s NOL carryforwards, and reduced goodwill by the

$2.3 million tax benefit of such utilization.

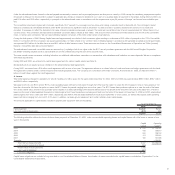

13. Impairment Loss/Lease Termination

In response to the expected slowdown in air travel as a result of the September 11 Events, we announced on September 17, 2001 an updated capacity plan whereby we reduced our

scheduled operations to approximately 80 percent of our pre-September 11th schedule. With other airlines similarly reducing flights and grounding older aircraft types resulting in an

overall reduction in values in the previously-owned aircraft market, we decided to review our DC-9 fleet for impairment. During the second quarter of 2001, we announced our intention

to retire our fleet of four B737 aircraft in the third quarter of 2001 in order to simplify our fleet and reduce costs. The B737s are being replaced with B717 aircraft. We have subsequently

sold and delivered all three of the owned B737 aircraft.

In connection with the 2001 reduction in value of the DC-9s and B737s, we performed evaluations to determine, in accordance with SFAS 121, whether future cash flows (undiscounted

and without interest charges) expected to result from the use and eventual disposition of these aircraft would be less than the aggregate carrying amount of these aircraft and related

assets. As a result of the evaluations, management determined that the estimated future cash flows expected to be generated by these aircraft would be less than their carrying amounts,

and therefore these aircraft are impaired as defined by SFAS 121. Consequently, the original cost bases of these assets were reduced to reflect the fair market value at the date the decisions

were made, resulting in a $28 million impairment loss on the DC-9s and a $10.8 million impairment loss on the B737s in 2001. We used appraisals and considered recent transactions

and market trends involving similar aircraft in determining the fair market values.

In addition, spare parts, materials and supplies were written down to the lower of cost or market. Such charges totaled $3.4 million in 2001.

We are currently in negotiations with the lessor regarding the disposition of one leased B737. The termination of the lease includes estimated costs related to buying out the lease and

to bring the aircraft into compliance with the return provisions of the lease agreement. The lease termination charge was $7.3 million. The remaining balance of accruals for the lease

termination at December 31, 2002 and 2001 were $5.1 million and $6.7 million, respectively.

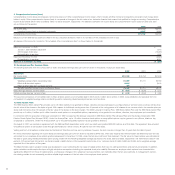

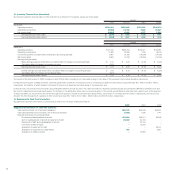

14. Employee Benefit Plans

Effective January 1, 1998, we consolidated our 401(k) plans (the Plan). All employees, except pilots, are eligible to participate in the consolidated Plan, a defined contribution benefit plan

that qualifies under Section 401(k) of the Internal Revenue Code. Participants may contribute up to 15 percent of their base salary to the Plan. Contributions to the Plan by Holdings are

discretionary. The amount of our contributions to the Plan expensed in 2002, 2001 and 2000 were approximately $0.2 million, $0.3 million and $0.5 million, respectively.

Effective in the third quarter of 2000, Airways agreed to fund, on behalf of our mechanics and inspectors, a monthly fixed contribution per eligible employee to their union’s pension plan.

In May of 2001, a similar agreement was made on behalf of our maintenance training instructors. During 2002 and 2001, we expensed approximately $0.3 million and $0.2 million,

respectively, related to these agreements. Beginning in January 2002, additional agreements with our stores clerks and ground service equipment employees took effect that call for a

monthly fixed amount per eligible employee to be made to the union’s pension plan. During 2002, the contribution to this plan was less than $0.1 million. At the time these agreements

take effect, the eligible employee may continue making contributions to the Plan, but there will be no company match.

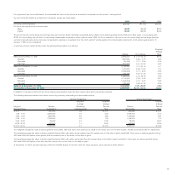

Effective August 1, 2001, the AirTran Airways Pilot Savings and Investment Plan (Pilot Savings Plan) was established. This plan is designed to qualify under Section 401(k) of the Internal

Revenue Code. Funds previously invested in the Plan, representing contributions made by and for pilots, were moved to the Pilot Savings Plan during 2001. Eligible employees may

contribute up to the IRS maximum allowed. We will not match pilot contributions to this Pilot Savings Plan. Effective on August 1, 2001, we also established the Pilot-Only Defined

Contribution Pension Plan (DC Plan) which qualifies under Section 403(b) of the Internal Revenue Code. Company contributions were 6 percent of eligible gross wages during 2001,

increasing to 7 percent, 8 percent and 10.5 percent during 2002, 2003 and 2004, respectively. We expensed $3.3 million and $1.8 million in contributions to the DC Plan during 2002

and 2001, respectively.

Under our 1995 Employee Stock Purchase Plan, employees who complete 12 months of service are eligible to make periodic purchases of our common stock at up to a 15 percent

discount from the market value on the offering date. The Board of Directors determines the discount rate, which was increased to 10 percent from 5 percent effective November 1, 2001.

We are authorized to issue up to 4 million shares of common stock under this plan. During 2002, 2001 and 2000, the employees purchased a total of 196,424, 31,396 and 61,626

shares, respectively, at an average price of $4.44, $6.93 and $4.30 per share, respectively.

25