Xcel Energy 2008 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2008 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

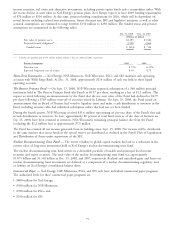

If Xcel Energy were to use alternative assumptions for Dec. 31, 2008 pension expense determinations, a one-percent

change would result in the following impact on the estimates recognized by Xcel Energy:

Pension Costs

+1% 1%

(In Millions)

Rate of Return ............................................. $(20.1) $20.1

Discount Rate .............................................. (4.8) 6.9

Effective Dec. 31, 2008, Xcel Energy reduced its initial medical trend assumption from 8.0 percent to 7.4 percent. The

ultimate trend assumption remained unchanged at 5.0 percent. The period until the ultimate rate is reached is five

years. Xcel Energy bases its medical trend assumption on the long-term cost inflation expected in the health care

market, considering the levels projected and recommended by industry experts, as well as recent actual medical cost

increases experienced by Xcel Energy’s retiree medical plan. See Note 11 to the consolidated financial statements for

additional discussion of Xcel Energy’s benefit plans.

Xcel Energy continually makes judgments and estimates related to these critical accounting policy areas, based on an

evaluation of the varying assumptions and uncertainties for each area. The information and assumptions underlying

many of these judgments and estimates will be affected by events beyond the control of Xcel Energy, or otherwise

change over time. This may require adjustments to recorded results to better reflect the events and updated information

that becomes available. The accompanying financial statements reflect management’s best estimates and judgments of

the impact of these factors as of Dec. 31, 2008.

For a discussion of significant accounting policies, see Note 1 to the consolidated financial statements.

Nuclear Decommissioning

NSP-Minnesota owns nuclear generation facilities and regulations require NSP-Minnesota to decommission its nuclear

power plants after each facility is taken out of service. Xcel Energy records future plant removal obligations as a liability

at fair value. This liability will be increased over time by applying the interest method of accretion to the liability. Due

to regulation, depreciation expense is recorded to match the recovery of future cost of decommissioning, or retirement,

of its nuclear generating plants. This recovery is calculated using an annuity approach designed to provide for full rate

recovery of the future decommissioning costs.

Amounts recorded for nuclear AROs, in excess of decommissioning expense and investment returns, both realized and

unrealized, cumulatively are deferred through the establishment of a regulatory asset for future recovery pursuant to

SFAS No. 71.

A portion of the rates charged to customers is deposited into an external trust fund, during the facilities’ operating lives,

in order to provide for this obligation. The fair value of external nuclear decommissioning trust fund investments are

estimated based on quoted market prices for those or similar investments. Realized investment returns from these

investments and recovery to date is used by regulators when determining future decommissioning recovery.

NSP-Minnesota conducts periodic decommissioning cost studies to estimate the costs that will be incurred to

decommission the facilities. The costs are initially presented in amounts prior to inflation adjustments and then inflated

to future periods using decommissioning specific cost inflators. Decommissioning of NSP-Minnesota’s nuclear facilities

is planned for the period from cessation of operations through 2067 assuming the prompt dismantlement method. The

following key assumptions have a significant effect on these estimates:

• Escalation Rate — The MPUC determines the escalation rate based on various presumptions surrounded by the

fact that associated costs will escalate at a certain rate over time. The most recent decommissioning study set the

escalation rate at 3.61 percent. An escalation rate for the cost of disposing of nuclear fuel waste was set at

6.0 percent. Over the short-term, these rates can differ from the set rates and accrual estimates can be

significantly affected by small changes in assumed escalation rates.

• Life Extension — Currently, decommissioning recovery periods end in 2020 for Monticello and in 2013 and

2014 for Prairie Island’s two facilities. Changes made to decommissioning cost estimates, the escalation rate and

the earnings rate can be amplified by these short end-of-license life periods. With the recent re-licensing of

Monticello and the application for the re-licensing of Prairie Island, any change in license life could have a

material effect on the accrual. Under FASB Statement No. 143, Accounting for AROs (SFAS No. 143), current

calculations have assumed full life extension, which brings the regulatory recovery period up to 2020. An

65