Under Armour 2007 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2007 Under Armour annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

Intangible Assets

Intangible assets that are determined to have a definite life are amortized over the asset’s estimated useful

life and are evaluated and measured for impairment in accordance with our Long-Lived Assets critical accounting

policy discussed above.

Income Taxes

Income taxes are accounted for under the asset and liability method. Deferred income tax assets and

liabilities are established for temporary differences between the financial reporting basis and the tax basis of our

assets and liabilities at tax rates expected to be in effect when such assets or liabilities are realized or settled.

Deferred income tax assets are reduced by a valuation allowance if, in the judgment of our management, it is

more likely than not that such assets will not be realized.

Income taxes include the largest amount of tax benefit for an uncertain tax position that is more likely than

not to be sustained upon audit based on the technical merits of the tax position. Settlements with tax authorities,

the expiration of statutes of limitations for particular tax positions, or obtaining new information on particular tax

positions may cause a change to the effective tax rate.

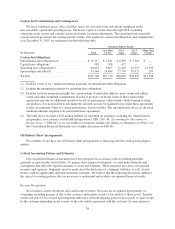

Stock-Based Compensation

Compensation expense is recognized in accordance with the Statement of Financial Accounting Standards

(“SFAS”) No. 123R, Share-Based Payment (revised 2004) (“SFAS 123R”). Compensation expense under SFAS

123R includes the expense of stock-based compensation awards granted on and subsequent to January 1, 2006

and the expense for the remaining vesting term of stock-based compensation awards issued subsequent to our

initial filing of the S-1 Registration Statement with the SEC on August 26, 2005. Stock-based compensation

awards granted prior to our initial filing of the S-1 Registration Statement are excluded from SFAS 123R and

will continue to be accounted for in accordance with Accounting Principles Board (“APB”) Opinion No. 25,

Accounting for Stock Issued to Employees (“APB 25”) and Financial Interpretation (“FIN”) No. 28, Accounting

for Stock Appreciation Rights and Other Variable Stock Option or Award Plans, until fully amortized through

2010. With the adoption of SFAS 123R, no material cumulative adjustments were recorded. As of December 31,

2007, we had $16.2 million of unrecognized compensation expense expected to be recognized over a weighted

average period of 4.0 years.

Determining the appropriate fair value model and calculating the fair value of stock-based compensation

awards require the input of highly subjective assumptions, including the expected life of the stock-based

compensation awards and stock price volatility. We use the Black-Scholes option-pricing model to determine the

fair value of stock-based compensation awards. The assumptions used in calculating the fair value of stock-based

compensation awards represent management’s best estimates, but the estimates involve inherent uncertainties

and the application of management judgment. As a result, if factors change and we use different assumptions, our

stock-based compensation expense could be materially different in the future (see Note 2 to the Consolidated

Financial Statements for a further discussion on stock-based compensation).

New Accounting Pronouncements

In December 2007, the Securities and Exchange Commission issued SAB No. 110, Share-Based Payment

(“SAB 110”). SAB 110 amends SAB 107, and allows for the continued use, under certain circumstances, of the

“simplified method” in developing an estimate of the expected term on stock options accounted for under SFAS

123R. SAB 110 is effective for stock options granted after December 31, 2007. We are currently evaluating the

impact of the new provisions of SAB 110 for stock option awards granted in the future.

In February 2007, the FASB issued SFAS No. 159, The Fair Value Option for Financial Assets and

Financial Liabilities—Including an amendment of FASB Statement No. 115 (“SFAS 159”). SFAS 159 permits

40