Huntington National Bank 2014 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2014 Huntington National Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

|

|

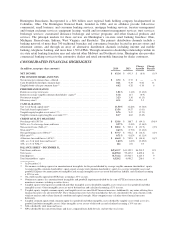

impacted by the net mortgage servicing rights hedging activity. Double-digit electronic banking income growth,

driven by customer growth, combined with increased securities gains, as we adjusted the mix of our securities

portfolio to prepare for LCR, offset a decrease in other fee income, trust services, and lower fees associated with

commercial loan and capital market activity.

Noninterest expense increased $124 million, or 7%, from the prior year. When adjusting for the net $76

million of Significant Items discussed in the attached SEC Form 10-K, noninterest expense increased $48

million, or 3%. We continued to invest in the franchise to plan, build, and deliver differentiated products and

services. Professional services increased due to outside consultant expenses related to the refresh of our five-year

strategic plan and legal services. Outside data processing and other services increased, primarily reflecting higher

debit and credit card processing costs and increased other technology investment expense, as we continue to

invest in technology supporting our products, services, and our Continuous Improvement initiatives.

We remain diligent with respect to maintaining our aggregate moderate-to-low risk profile. We continue to

invest in our risk and credit infrastructure. Credit quality continued to improve with nonaccrual loans,

nonperforming assets, and net charge-offs all decreasing from the prior year levels. However, criticized and

classified loans did increase. Net charge-offs, at 0.27% of average loans and leases, were below our long-term

expected range of 0.35% to 0.55%.

For the previous five years, we diligently rebuilt our capital levels in excess of all capital adequacy

requirements. The Board and management now believe that Huntington’s capital is at a level above what is

required to operate day-to-day and robust enough to weather future stressed environments. This belief is based on

the implementation of controls and risk management processes related to our aggregate moderate-to-low risk

profile, the advanced modeling developed as part of our annual stress testing process, and the significant

remixing of the loan portfolio that has occurred over the last several years. With that as the starting point, we

allowed our capital to modestly decrease over the last year as we drove double-digit balance sheet growth,

increased the dividend, increased share repurchase activity, and completed two acquisitions. Tangible common

equity to tangible assets ratio ended the year at 8.17%, down 65 basis points from a year ago, and Tier 1 common

risk-based capital ratio was 10.23%, down from 10.90% at the end of 2013.

The full detail of our financial performance can be found or is outlined in the Management Discussion and

Analysis section found later in the attached SEC Form 10-K. Please take the opportunity to read this. It provides

additional insight and commentary related to our 2014 financial performance.

Turning to 2015 expectations, although we again expect to face challenges from interest rates and the

regulatory environment, we believe that with our successful strategies, focused execution, and business model we

will continue to overcome these challenges and deliver solid performance.

2015 will be a year focused around sales execution, enhancing our digital platform, and driving deep

relationships with our growing customer base. We built our plan with an assumption of no change in interest

rates and with the flexibility to quickly adjust to an evolving operating environment, if necessary. We remain

committed to investing in the business, disciplined expense control, and delivering full-year positive operating

leverage through growing revenue faster than our expected 2%-4% noninterest expense growth. Overall, asset

quality metrics are expected to remain near current levels, although moderate quarterly volatility also is expected

given the absolute low level of problem assets and credit costs. We anticipate net charge-offs will remain within

or below our long-term normalized range of 35 to 55 basis points.

We are committed to delivering long-term value to our shareholders and meeting the last two long-term

goals of an efficiency ratio of 56%-59% and return on tangible common equity of 13%-15%. At Huntington, we

believe that “doing the right thing” for our shareholders, colleagues, customers, and communities is the path to

developing a robust franchise that can produce the stable returns needed to create long-term value.

2