Huntington National Bank 2014 Annual Report Download - page 2

Download and view the complete annual report

Please find page 2 of the 2014 Huntington National Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

|

|

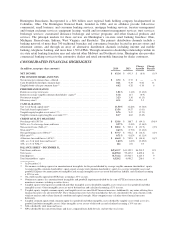

Huntington Bancshares Incorporated is a $66 billion asset regional bank holding company headquartered in

Columbus, Ohio. The Huntington National Bank, founded in 1866, and its affiliates provide full-service

commercial, small business, and consumer banking services; mortgage banking services; treasury management

and foreign exchange services; equipment leasing; wealth and investment management services; trust services;

brokerage services; customized insurance brokerage and service programs; and other financial products and

services. The principal markets for these services are Huntington’s six-state retail banking franchise: Ohio,

Michigan, Pennsylvania, Indiana, West Virginia, and Kentucky. The primary distribution channels include a

banking network of more than 700 traditional branches and convenience branches located in grocery stores and

retirement centers, and through an array of alternative distribution channels including internet and mobile

banking, telephone banking, and more than 1,500 ATMs. Through automotive dealership relationships within its

six-state retail banking franchise area and selected other Midwest and Northeast states, Huntington also provides

commercial banking services to the automotive dealers and retail automobile financing for dealer customers.

CONSOLIDATED FINANCIAL HIGHLIGHTS

(In millions, except per share amounts) 2014 2013

Change

Amount

Change

Percent

NET INCOME $ 632.4 $ 641.3 $ (8.9) (1)%

PER COMMON SHARE AMOUNTS

Net income per common share – diluted .......................................... $ 0.72 $ 0.72 $ — — %

Cash dividend declared per common share ........................................ 0.21 0.19 0.02 11

Tangible book value per common share(1) ......................................... 6.62 6.26 0.36 6

PERFORMANCE RATIOS

Return on average total assets .................................................. 1.01% 1.14% (0.13)%

Return on average tangible common shareholders’ equity(2) ........................... 11.8 12.7 (0.9)

Net interest margin(3) ......................................................... 3.23 3.36 (0.13)

Efficiency ratio(4) ............................................................ 65.1 62.6 2.5

CAPITAL RATIOS

Tier 1 risk-based capital ratio(1) ................................................. 11.50% 12.28% (0.78)%

Total risk-based capital ratio(1) .................................................. 13.56 14.57 (1.01)

Tangible equity/tangible assets ratio(1)(5)(6) ......................................... 8.76 9.47 (0.71)

Tangible common equity/tangible asset ratio(1)(6)(7) .................................. 8.17 8.82 (0.65)

CREDIT QUALITY MEASURES

Net charge-offs (NCOs) ....................................................... $ 124.6 $ 188.7 $ (64.1) (34)%

NCOs as a % of average loans and leases ......................................... 0.27% 0.45% (0.18)%

Non-accrual loans (NALs)(1) ................................................... $ 300.2 $ 322.1 $ (21.9) (7)%

NAL ratio(1)(8) ............................................................... 0.63% 0.75% (0.12)%

Non-performing assets (NPAs)(1) ................................................ $ 337.7 $ 352.2 $ (14.5) (4)%

NPA ratio(1)(9) ............................................................... 0.71% 0.82% (0.11)%

Allowance for credit losses (ACL)(1) ............................................. $ 666.0 $ 710.8 $ (44.8) (6)%

ACL as a % of total loans and leases(1) ........................................... 1.40% 1.65% (0.25)%

ACL as a % of NALs(1) ....................................................... 222 221 1.0

BALANCE SHEET – DECEMBER 31,

Total loans and leases ........................................................ $47,655.7 $43,120.5 $4,535.2 11%

Total assets ................................................................. 66,298.0 59,467.2 6,830.8 11

Total deposits ............................................................... 51,732.2 47,506.7 4,225.5 9

Total shareholders’ equity ..................................................... 6,328.2 6,090.2 238.0 4

(1) At December 31.

(2) Net income excluding expense for amortization of intangibles for the period divided by average tangible common shareholders’ equity.

Average tangible common shareholders’ equity equals average total common shareholders’ equity less average intangible assets and

goodwill. Expense for amortization of intangibles and average intangible assets are net of deferred tax liability, and calculated assuming

a 35% tax rate.

(3) On a fully-taxable equivalent (FTE) basis assuming a 35% tax rate.

(4) Noninterest expense less amortization of intangibles and goodwill impairment divided by the sum of FTE net interest income and

noninterest income excluding securities losses.

(5) Tangible equity (total equity less goodwill and other intangible assets) divided by tangible assets (total assets less goodwill and other

intangible assets). Other intangible assets are net of deferred tax and calculated assuming a 35% tax rate.

(6) Tangible equity, tangible common equity, and tangible assets are non-GAAP financial measures. Additionally, any ratios utilizing these

financial measures are also non-GAAP. These financial measures have been included as they are considered to be critical metrics with

which to analyze and evaluate financial condition and capital strength. Other companies may calculate these financial measures

differently.

(7) Tangible common equity (total common equity less goodwill and other intangible assets) divided by tangible assets (total assets less

goodwill and other intangible assets). Other intangible assets are net of deferred tax and calculated assuming a 35% tax rate.

(8) NALs divided by total loans and leases.

(9) NPAs divided by the sum of total loans and leases, impaired loans held-for-sale, and net other real estate.