Huntington National Bank 2003 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2003 Huntington National Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

LETTER TO SHAREHOLDERS

4

Where We Are

A year ago, I said we were positioned to win. And financially in 2003, we did. But winning is also a long-term objective

and more than just making short-term numbers.

You will recall, we spent much of 2002 building a new culture, one that “values each associate’s contribution, encourages

active participation, demands teamwork, creates a sense of urgency, and holds everyone personally responsible for

making Huntington better.” I am pleased to report that this culture began to take hold in 2003. Associates are

increasingly making decisions on the spot that benefit our customers. We are seeing increased cooperation and business

referrals between our various lines of business.

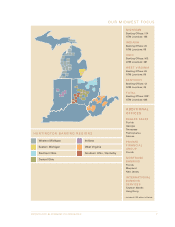

It is equally rewarding to see validation of our business model concept, the “local bank with national resources,” with

local decision-making close to customers whenever possible. Supporting our strong financial performance were

increased sales, higher customer satisfaction ratings and higher deposit market share in most of our markets. Our

name recognition is also higher. When asked about what bank they would most likely switch their banking relationship

to, more and more potential customers are saying “Huntington.” And, as the word is getting out about how enabling

our culture is, we are increasingly attracting top-flight talent to all levels of the company.

We have come a very long way, and associates can be justifiably proud of their contributions.

Where We Want to Be

But there is still much more to be done. Our aspiration is to be “high-performing,” though we are not there yet.

Financially, we must strive for consistent annual earnings per share growth of 10% to 12% and return on shareholders’

equity of 18% to 20%. We believe that by doing so we will deliver superior dividend growth and stock price improvement.

Critical to our success will be our ability to deliver service that customers view as “simply the best.” As the “local

bank,” our value proposition for customers must be service excellence. This requires a daily dedication by all

Huntington associates to meet and exceed customer expectations. We hope that when we succeed consistently in this

effort, customers will view Huntington as an “essential partner,” which is our vision.

To support associates serving customers in banking offices and through our Direct Bank call center, we will upgrade sales

and service technology in 2004. And to provide added customer convenience, we will open new banking offices, expand

our ATM network and capabilities and upgrade our nationally recognized on-line banking and bill paying services.

2004 Outlook

We anticipate that the economy will be somewhat stronger, with inflation and interest rates remaining at low levels.

As a result, we should see a modest increase in commercial loan demand and continued strong growth in small business,

home equity and auto loans. Our net interest margin should remain close to the 2003 fourth quarter level.

We also expect capital and equity markets to gain momentum. This may make deposit growth more of a challenge,

but it should benefit growth in brokerage and insurance fees and in trust and investment management income.

Net charge-offs should continue to decline reflecting both a better economy and our improved and higher under-

writing standards of the last couple of years.

Despite higher pension and healthcare costs in 2004, we expect that our efficiency ratio will improve.

In summary, I am confident 2004 will be another good year for Huntington.