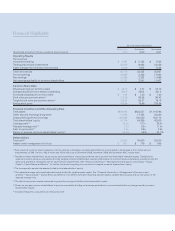

Goldman Sachs 2009 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2009 Goldman Sachs annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

9

The markets for residential mortgage-related products, and

subprime mortgage securities in particular, were volatile and

unpredictable in the rst half of 2007. Investors in these markets

held very different views of the future direction of the U.S.

housing market based on their outlook on factors that were

equally available to all market participants, including housing

prices, interest rates and personal income and indebtedness

data. Some investors developed aggressively negative views

on the residential mortgage market. Others believed that any

weakness in the residential housing markets would be relatively

mild and temporary. Investors with both sets of views came

to GoldmanSachs and other nancial intermediaries to establish

long and short exposures to the residential housing market

through RMBS, CDOs, CDS and other types of instruments

or transactions.

The investors who transacted with GoldmanSachs in CDOs

in 2007, as in prior years, were primarily large, global nancial

institutions, insurance companies and hedge funds (no pension

funds invested in these products, with one exception: a

corporate-related pension fund that had long been active in this

area made a purchase of less than $5 million). These investors

had signi cant resources, relationships with multiple nancial

intermediaries and access to extensive information and research

ow, performed their own analysis of the data, formed their

own views about trends, and many actively negotiated at arm’s

length the structure and terms of transactions.

We certainly did not know the future of the residential

housing market in the rst half of 2007 any more than we can

predict the future of markets today. We also did not know

whether the value of the instruments we sold would

increase or decrease. It was well known that housing prices

were weakening in early 2007, but no one — including

GoldmanSachs — knew whether they would continue to fall or

to stabilize at levels where purchasers of residential mortgage-

related securities would have received their full interest and

principal payments.

Although GoldmanSachs held various positions in residential

mortgage-related products in 2007, our short positions were not

a “bet against our clients.” Rather, they served to offset our long

positions. Our goal was, and is, to be in a position to make markets

for our clients while managing our risk within prescribed limits.

LOOKING AHEAD

We want to recognize the extraordinary focus and commitment

of our people despite the turbulence and challenges of the past

year. In many ways, our nancial performance masks the

considerable pressures and distractions that we had to confront.

Of course, in this way, we are no different from many other

organizations that are coping with a complex and dif cult

environment. But, our people stayed focused, they worked

together, and, today, we are well-positioned to continue delivering

strong returns for our shareholders.

Heading into 2010, we are grati ed that our core constituencies

—

our shareholders, our clients, and our people — remain close

and committed to GoldmanSachs. Our shareholders continue

to convey a strong belief in our business model and strategy,

and in the importance of protecting the quality of our franchise.

Our clients look to us to advise, execute and co-invest on

their most signi cant transactions, translating into strong market

shares. And our people remain as committed as ever to our

culture of teamwork, to the belief in their responsibility to

help allocate capital for the bene t of clients, and to the rm’s

tradition of service and philanthropy.

As the last two years demonstrated, no one can predict

the future. While we are encouraged by the prospects for a

sustainable economic recovery, we continue to place a premium

on conservatism and prudence. At the same time, we are

focused on opportunities that can continue to grow our business

and generate industry-leading returns through the strength of

the rm’s core attributes. We have a clear strategy to integrate

advice and capital with risk management for our clients.

We have a diverse set of businesses. We have an expanding

global footprint. We have established a proven culture of risk

management. And, we have deep client relationships with a

broad range of companies, institutions, investing organizations

and high-net-worth individuals.

We are keenly aware that our legacy of client service and

performance, which every person at GoldmanSachs is charged

with protecting and advancing, must be continually nurtured

and passed on from one generation to the next. To our fellow

shareholders, we are pleased to report that we have never

been more con dent of that commitment or long-term outcome.

Lloyd C. Blankfein

Chairman and Chief Executive Of cer

Gary D. Cohn

President and Chief Operating Of cer

Goldman Sachs 2009 Annual Report