Family Dollar 2012 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2012 Family Dollar annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

The transfers out of Level 3 during fiscal 2011 resulted from issuer call notices (at par). The Company treated the

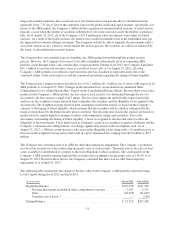

call notices as quoted prices in an inactive market (Level 2 inputs).

Additional Fair Value Disclosures

The estimated fair value of the Company’s current and long-term debt was $576.4 million as of August 25, 2012,

and $566.0 million as of August 27, 2011. The Company has both public notes and private placement notes. The

fair value for the public notes is determined using Level 1 inputs as quoted prices in active markets for identical

assets or liabilities are available. The fair value of the portion of the debt that are private placement notes is

determined through the use of a discounted cash flow analysis using Level 3 inputs as there are no quoted prices

in active markets for these notes. The discount rate used in the analysis was based on borrowing rates available to

the Company for debt of the same remaining maturities, issued in the same private placement debt market. The

fair value of the Company’s current and long-term debt was greater than the carrying value of the debt by $43.9

million as of August 25, 2012, and $16.0 million as of August 27, 2011. See Note 5 for more information on the

Company’s long-term debt.

3. Investment Securities:

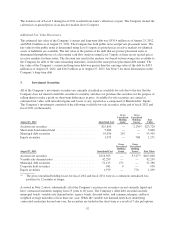

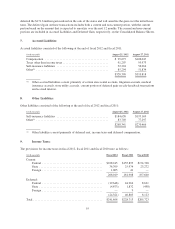

All of the Company’s investment securities are currently classified as available-for-sale due to the fact that the

Company does not intend to hold the securities to maturity and does not purchase the securities for the purpose of

selling them to make a profit on short-term differences in price. Available-for-sale securities are carried at

estimated fair value, with unrealized gains and losses, if any, reported as a component of Shareholders’ Equity.

The Company’s investments consisted of the following available-for-sale securities at the end of fiscal 2012 and

fiscal 2011 (in thousands):

August 25, 2012 Amortized Cost

Gross

Unrealized

Holding

Gains

Gross

Unrealized

Holding

Losses

Fair

Value

Auction rate securities ................................ $25,850 — 2,130(1) $23,720

Short-term bond mutual fund ........................... 5,000 — — 5,000

Municipal debt securities .............................. 55,036 267 — 55,303

Equity securities ..................................... 1,979 — 708 1,271

August 27, 2011 Amortized Cost

Gross

Unrealized

Holding

Gains

Gross

Unrealized

Holding

Losses Fair Value

Auction rate securities ............................... $116,925 — 9,317(1) $107,608

Variable rate demand notes ............................ 42,299 — — 42,299

Municipal debt securities ............................. 51,125 273 — 51,398

Corporate debt securities ............................. 941 9 — 950

Equity securities .................................... 1,979 — 770 1,209

(1) The gross unrealized holding losses for fiscal 2012 and fiscal 2011 were in a continuous unrealized loss

position for 12 months or longer.

As noted in Note 2 above, substantially all of the Company’s auction rate securities are not currently liquid and

have contractual maturities ranging from 15 years to 46 years. The Company’s other debt securities include

municipal bonds, variable-rate demand notes, agency bonds, discount notes, and commercial paper, and have

weighted average maturities of less than one -year. While the variable rate demand notes have underlying

contractual maturities beyond one year, the securities are traded in the short-term as a result of 7-day put options.

52