Carphone Warehouse 2015 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2015 Carphone Warehouse annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

Dixons Carphone plc Annual Report and Accounts 2014/15

Strategic report

Key performance indicators

15

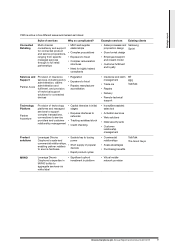

Financial and operational

Definition Performance

Total

Headline

sales*

Growth in total Headline sales. The ability to grow sales is an important

measure of a brand’s appeal to customers and its competitive position.

2014/15

£9,936m

2013/14†

£9,752m

Like-for-

like sales

Like-for-like sales are calculated based on Headline store and internet

sales using constant exchange rates. New stores are included where they

have been open for a full financial year both at the beginning and end of

the financial period. Sales from franchise stores are excluded and closed

stores are excluded for any period of closure during either period.

Customer support agreement, insurance and wholesale revenues along

with revenue from Connected World Services and other non-retail

businesses are excluded from like-for-like calculations. Revenue from

Carphone Warehouse SWAS are included in like-for-like.

2014/15

6%

2013/14†

4%

Market

position

In line with the Group’s strategy to be the leading specialist electrical and

mobile retailer in Europe, this is an important measure of how well

customers are being engaged by the Group’s brands in each market.

Retailing operations should be, or be capable of becoming, the number

one or number two specialist electrical retailer in their market, measured

by market share.

Market leading

positions in:

UK & Ireland

Nordics

Greece

Headline

EBIT*

Continued growth of Headline EBIT enables the Group to invest in its

future and provide a return for shareholders. Targets are set relative to

expected market performance.

2014/15

£414m

2013/14†

£359m

Headline

profit before

tax*

Continued growth of Headline profit before tax represents a measure of

Group performance to external investors and shareholders. Targets are

set relative to expected market performance.

2014/15

£381m

2013/14†

£316m

Free Cash

Flow*

The Group defines Free Cash Flow as net cash generated from

operations, less net finance costs, taxation and net capital expenditure

and excluding certain discrete items such as special pension

contributions. The management of cash usage, in particular working

capital employed in the business, optimises resources available for the

Group to invest in its future growth and to generate shareholder value.

2014/15

£(112)m

2013/14†

£280m

Return on

Capital

Employed

(ROCE)

The Group calculates ROCE on a pre-tax and lease adjusted basis. The

return is based on Headline EBIT, adjusted to add back the estimated

interest component associated with capitalising operating lease costs.

Capital employed is based on net assets including capitalised leases, but

excluding goodwill, cash, tax and the defined benefit pension obligations.

The calculation is performed on a moving annual total in order to best

match the return on assets in a year with the assets in use during the

year to generate the return.

2014/15

20%

2013/14†

N/A

Shareholder

Definition Performance

Headline basic

earnings per

share* (EPS)

The level of growth in EPS provides a suitable measure of the financial

health of the Group and its ability to deliver returns to shareholders

each year. The Group targets growth in EPS commensurate with growth

in earnings.

2014/15

25.5p

2013/14†

20.5p

Total

shareholder

return (TSR)

This metric provides a relative performance measure over the longer term

of the Group’s ability to deliver returns for shareholders. The Group

previously used the FTSE 250 index but in 2015 changed to measure

itself against the FTSE 350 index reflecting the Group’s increased

market capitalisation.

3 Year Compound Annual Growth

Dixons Carphone plc 44%

FTSE 350 Index 12%

* Headline performance measures are as defined in the Performance Review. These have been reported on a pro forma basis as if the CPW

Europe Acquisition and the Merger had occurred at the start of the comparative period.

† Headline figures for the year ended 29 March 2014 have been re-presented to exclude the results of discontinued operations.