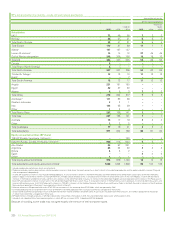

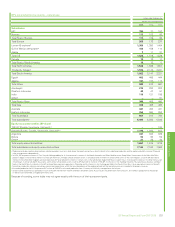

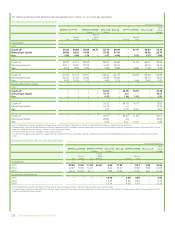

BP 2015 Annual Report Download - page 240

Download and view the complete annual report

Please find page 240 of the 2015 BP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

|

|

Environmental maritime regulations

BP’s shipping operations are subject to extensive national and

international regulations governing liability, operations, training, spill

prevention and insurance. These include:

• In US waters, OPA 90 imposes liability and spill prevention and

planning requirements governing, among others, tankers, barges and

offshore facilities. It also mandates a levy on imported and

domestically produced oil to fund oil spill responses. Some states,

including Alaska, Washington, Oregon and California, impose additional

liability for oil spills. Outside US territorial waters, BP shipping tankers

are subject to international liability, spill response and preparedness

regulations under the UN’s International Maritime Organization,

including the International Convention on Civil Liability for Oil Pollution,

the International Convention for the Prevention of Pollution from Ships

(MARPOL) Convention, the International Convention on Oil Pollution,

Preparedness, Response and Co-operation and the International

Convention on Civil Liability for Bunker Oil Pollution Damage. In April

2010, the Hazardous and Noxious Substance (HNS) Protocol 2010 was

adopted to address issues that have inhibited ratification of the

International Convention on Liability and Compensation for Damage in

Connection with the Carriage of Hazardous and Noxious Substances by

Sea 1996. As at year end, as the required minimum number of

contracting states had not been achieved, the HNS Convention has not

yet entered into force.

• Changes to the permitted level of sulphur in marine fuels under EU

mandated reductions for European waters and International Maritime

Organization (IMO) regulations are being phased in until 2020, when

the low sulphur rules for shipping in global waters are scheduled to

take effect. Depending on the outcome of ongoing IMO deliberations,

the regulations impacting operations in global waters may be delayed

until 2025. Regulations requiring the reduction of sulphur oxides

emissions will require ships to either burn low sulphur marine fuels or

continue using higher sulphur fuel along with approved on-board

sulphur abatement technology. Compliance with the IMO regulations

may place additional costs on refineries producing marine fuel,

including costs to dispose of sulphur, as well as increased GHG

emissions and energy costs for additional refining.

To meet its financial responsibility requirements, BP shipping maintains

marine liability pollution insurance in respect of its operated ships to a

maximum limit of $1 billion for each occurrence through mutual

insurance associations (P&I Clubs), although there can be no assurance

that a spill will necessarily be adequately covered by insurance or that

liabilities will not exceed insurance recoveries.

Greenhouse gas regulation

In 2011, parties to the UN Framework Convention on Climate Change

(Framework Convention) at the Conference of the Parties (COP17) in

Durban agreed to several measures. One was a ‘roadmap’ for negotiating

a legal framework for action on climate change by 2015 that would

involve all countries by 2020 and would close the ‘ambition gap’ between

existing GHG reduction pledges and what is required to achieve the goal

of limiting global temperature rise to 2°C. Another was a second

commitment period for the Kyoto Protocol to begin immediately after the

first period. An amendment was subsequently adopted at the 2012

conference of parties in Doha (COP18) establishing a second

commitment period to run until the end of 2020. However, it did not

include the US, Canada, Japan and Russia and thus covers only about

15% of global emissions.

The 2014 conference in Lima (COP20) adopted the Lima Call for Climate

Action. This included the elements of a negotiating text for a new

international agreement, as specified in Durban in 2011, that would be

finalized at COP21 in Paris in December 2015. This text covers long-term

ambitions and pathways and a framework for reaching it. COP20 also

agreed on the rules for providing and assessing information about each

country’s ’Intended Nationally Determined Contributions’ towards

reaching the overall ambition. The world’s three largest emitters – China,

the US and the EU – have all announced their intentions to limit their

GHG emissions.

In December 2015, 195 nations at the United Nations climate change

conference in Paris (COP21) adopted the Paris Agreement, for

implementation post-2020. This will come into force when it has been

ratified by at least 55 of the parties to the Framework Convention,

representing at least 55% of global GHG emissions. For the first time this

binds all participants to its provisions and encourages voluntary

contributions by developing countries. The Paris Agreement aims to hold

global average temperature rise to well below 2oC above pre-industrial

levels and to pursue efforts to limit temperature rise to 1.5oC above pre-

industrial levels. There is no quantitative long-term emissions goal but

countries aim to reach global peaking of GHG emissions as soon as

possible and to undertake rapid reductions thereafter to achieve a

balance between human caused emissions and natural absorption in the

second half of this century. The Paris Agreement places binding

commitments on all parties, from 2020, to make Nationally Determined

Contributions (NDCs) and pursue domestic measures aimed at achieving

the objectives of their NDCs. Developed country NDCs should include

absolute emission reduction targets, and developing countries are

encouraged to move over time towards them. The Paris Agreement

places binding commitments on countries, starting by 2023, to report on

their emissions and progress made on their NDCs; undergo international

review of collective progress; and submit new, more ambitious NDCs

every five years. The Paris Agreement extends the existing goal for

climate finance to a minimum of $100 billion after 2025.

More stringent national and regional measures can be expected in the

future. These measures could increase BP’s production costs for certain

products, increase demand for competing energy alternatives or products

with lower-carbon intensity, and affect the sales and specifications of

many of BP’s products. Current and announced measures and

developments potentially affecting BP’s businesses include the

following:

• The EU has agreed to an overall GHG reduction target of 20% by 2020.

To meet this, a ‘Climate and Energy Package’ of regulatory measures

was adopted that includes: a collective national reduction target for

emissions not covered by the EU ETS; binding national renewable

energy targets to double usage of renewable energy sources in the EU

including at least a 10% share of renewable energy in the transport

sector; a legal framework to promote carbon capture and storage

(CCS); and a revised EU ETS Phase 3. EU ETS revisions included a

GHG reduction of 21% from 2005 levels; a significant increase in

allowance auctioning; an expansion in the scope of the EU ETS to

encompass more industrial sectors (including the petrochemicals

sector) and gases; no free allocation for electricity generation (including

that which is self-generated off-shore) or production, but benchmarked

free allocation for energy-intensive and trade-exposed industrial

sectors. EU ETS revisions also included the adoption of a Market

Stability Reserve to reduce the supply of auctioned allowances. This

will take effect in 2019 and could potentially lead to higher carbon

costs. EU Energy efficiency policy is currently implemented via national

energy efficiency action plans and the Energy Efficiency Directive

adopted in 2012. The EU has also agreed to the 2030 Climate and

Energy Policy framework with a goal of at least a 40% reduction in

GHGs from 1990 and measures to achieve a 27% share of renewable

energy and a 27% increase in energy efficiency. The GHG reduction

target is to be achieved by a 43% reduction of emissions from sectors

covered by the EU ETS, and a 30% GHG reduction by Member States

for all other GHG emissions.

• Canada’s highest emitting province, Alberta, has regulations targeting

large final emitters (sites with over 100,000 tonnes of carbon dioxide

equivalent per annum) with intensity targets of 2% improvement per

year up to 20%. Compliance is possible via direct reductions, the

purchase of offsets or the payment of C$20/tonne to a technology fund

which will escalate to $30/tonne in 2017. A new policy direction has

just been announced for post-2018 where performance relative to a

best in sector benchmark (to be determined) will now determine the

volume of emissions subject to a cost ($30/tonne escalating in real

terms) or use of other compliance mechanisms such as offsets.

• In the US, the EPA continues to pursue regulatory measures to

address GHGs under the CAA.

– EPA regulations impose light, medium and heavy duty vehicle

emissions standards for GHGs and permitting requirements for

236 BP Annual Report and Form 20-F 2015