Suzuki 2005 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2005 Suzuki annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

|

|

expected future tax consequences of temporary differences between the carrying

amounts and the tax bases of assets and liabilities.

In making a valuation for the possibility of collection of deferred tax assets, the

Company and its subsidiaries estimate our future taxable income reasonably. If the

estimated amount of future taxable income decrease, deferred tax assets may

decrease and income taxes expenses may be posted.

(l)Accrued retirement and severance benefits

In order to allow for payment of employees' retirement benefits, based on the

estimated amount of retirement benefits liabilities and pension assets at the end of

this fiscal year, the allowable amount which occurs at the end of this fiscal year is

appropriated.

With regard to prior service costs, the amount, prorated on a straight line basis

over the period of average length of employees' remaining service years at the time

when it

occurs, is treated as expenses. As for the actuarial differences, the amounts

prorated on a straight line basis over the period of average length of employees'

remaining service years in each year in which the differences occur are

respectively treated as expenses from the next term of the year in which they arise.

As for directors, the amount payable to be paid at the end of year is posted

pursuant to the Company's regulations on the retirement allowance of directors.

Retirement benefit cost and retirement benefit obligation are calculated on the

actuarial assumptions, which include discount rate, assumed return of investment

ratio,

revaluation ratio, salary rise ratio, retirement ratio and mortality ratio. Discount rate

is decided on the basis of yield on low-risk, long-term bonds, and assumed return

of investment ratio is decided based on the investment policies of pension assets of

each pension system etc. Decreased yield on long-term bond leads to a decrease

in discount rate and has an adverse influence on the calculation of retirement

benefit cost. However, the pension system adopted by the Company has a cash

balance type plan, and thus the revaluation ratio, which is one of the base ratios,

can offset any adverse effects caused by a decrease in the discount rate.

If the investment yield of pension assets is less than the assumed return of

investment ratio, it will have an adverse effect on the calculation of retirement

benefit cost. But by focusing on low-risk investments, this influence should be

minimal in the case of the pension fund systems of the Company and its

subsidiaries.

(m)Revenue recognition

Sales of products are generally recognized in the accounts as delivery is made.

(n)Amounts per share

Primary net income per share is computed based on the weighted average

number of shares issued during the respective years. Fully diluted net income per

share is computed assuming that all convertible bonds were converted into

common stock, with an applicable adjustment for related interest expense and net

of tax. Cash dividends per share are the amounts applicable to the respective

periods including dividends to be paid after the end of the period.

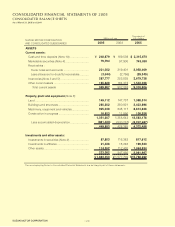

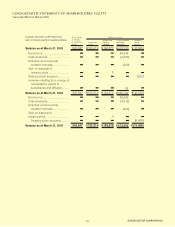

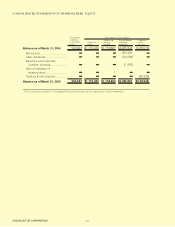

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

SUZUKI MOTOR CORPORATION

−32−