Red Lobster 2009 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2009 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74

|

|

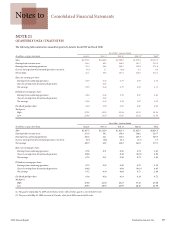

2009 Annual Report Darden Restaurants, Inc. 63

Notes to Consolidated Financial Statements

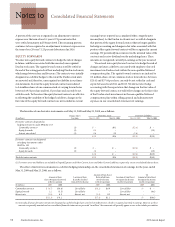

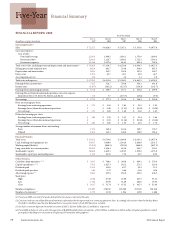

Components of net periodic benefit cost included in continuing operations are as follows:

Defined Benefit Plans Postretirement Benefit Plan

(In millions)

2009 2008 2007 2009 2008 2007

Service cost $ 6.0 $ 6.1 $ 6.0 $ 0.7 $ 0.7 $ 0.7

Interest cost 9.9 9.7 9.0 1.7 1.2 1.0

Expected return on plan assets (16.3) (14.8) (13.7) – – –

Amortization of unrecognized prior service cost 0.2 0.1 0.1 – (0.1) –

Recognized net actuarial loss 0.4 4.3 5.4 0.6 0.3 0.2

Net periodic benefit cost $ 0.2 $ 5.4 $ 6.8 $ 3.0 $ 2.1 $ 1.9

The amortization of the net actuarial loss component of our fiscal

2010 net periodic benefit cost for the defined benefit plans and post-

retirement benefit plan is expected to be approximately $0.4 million

and $0.6 million, respectively.

The following benefit payments are expected to be paid between

fiscal 2010 and fiscal 2019:

Defined Postretirement

(In millions)

Benefit Plans Benefit Plan

2010 $11.6 $1.0

2011 10.2 1.0

2012 10.6 0.9

2013 11.1 1.0

2014 11.7 1.2

2015-2019 68.5 8.3

POSTEMPLOYMENT SEVERANCE PLAN

We accrue for postemployment severance costs in accordance with

SFAS No. 112, “Employers’ Accounting for Postemployment Benefits –

an amendment of FASB Statements No. 5 and 43,” and use guidance

found in SFAS No. 106, “Employers’ Accounting for Postretirement

Benefits Other Than Pensions,” to measure the cost recognized in our

consolidated financial statements. As a result, we use the provisions

of SFAS No. 158 to recognize actuarial gains and losses related to our

postemployment severance accrual as a component of accumulated

other comprehensive income (loss). As of May 31, 2009 and May 25,

2008, $4.5 million and $5.4 million, respectively, of unrecognized

actuarial losses related to our postemployment severance plan were

included in accumulated other comprehensive income (loss) on a net

of tax basis.

DEFINED CONTRIBUTION PLAN

We have a defined contribution plan covering most employees age

21 and older. We match contributions for participants with at least

one year of service up to six percent of compensation, based on our

performance. The match ranges from a minimum of $0.25 to $1.20

for each dollar contributed by the participant. The plan had net assets

of $477.9 million at May 31, 2009 and $469.0 million at May 25, 2008.

Expense recognized in fiscal 2009, 2008 and, 2007 was $2.0 million,

$1.3 million and $0.8 million, respectively. Employees classified as

“highly compensated” under the Internal Revenue Code are not

eligible to participate in this plan. Instead, highly compensated

employees are eligible to participate in a separate non-qualified

deferred compensation plan. This plan allows eligible employees

to defer the payment of part of their annual salary and all or part of

their annual bonus and provides for awards that approximate the

matching contributions and other amounts that participants would

have received had they been eligible to participate in our defined

contribution and defined benefit plans. Amounts payable to highly

compensated employees under the non-qualified deferred compen-

sation plan totaled $132.1 million and $143.8 million at May 31,

2009 and May 25, 2008, respectively. These amounts are included in

other current liabilities.

The defined contribution plan includes an Employee Stock

Ownership Plan (ESOP). This ESOP originally borrowed $50.0 million

from third parties, with guarantees by us, and borrowed $25.0 million

from us at a variable interest rate. The $50.0 million third party loan

was refinanced in 1997 by a commercial bank’s loan to us and a

corresponding loan from us to the ESOP. Compensation expense is

recognized as contributions are accrued. In addition to matching plan

participant contributions, our contributions to the plan are also made

to pay certain employee incentive bonuses. Fluctuations in our stock

price impact the amount of expense to be recognized. Contributions

to the plan, plus the dividends accumulated on unallocated shares

held by the ESOP, are used to pay principal, interest and expenses of

the plan. As loan payments are made, common stock is allocated to

ESOP participants. In fiscal 2009, 2008 and 2007, the ESOP incurred

interest expense of $0.3 million, $0.9 million and $1.2 million,

respectively, and used dividends received of $1.8 million, $4.4 million

and $3.6 million, respectively, and contributions received from us

of $2.4 million, $0.0 million and $0.7 million, respectively, to pay

principal and interest on our debt.

ESOP shares are included in weighted-average common shares

outstanding for purposes of calculating net earnings per share. At

May 31, 2009, the ESOP’s debt to us had a balance of $11.6 million with

a variable rate of interest of 0.69 percent and is due to be repaid no later

than December 2014. The number of our common shares held in the

ESOP at May 31, 2009 approximated 5.9 million shares, representing

3.7 million allocated shares and 2.2 million suspense shares.