Red Lobster 2009 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2009 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

MD&A Management’s Discussion and Analysis

of Financial Condition and Results of Operations

2009 Annual Report Darden Restaurants, Inc. 35

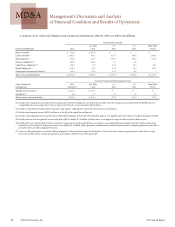

FINANCIAL CONDITION

Our total current assets were $554.8 million at May 31, 2009,

compared with $467.9 million at May 25, 2008. The increase resulted

primarily from an increase in prepaid income taxes due to current

year overpayments, an increase in inventory levels due to the timing

of purchases of inventory and the timing of promotions, and an

increase in current deferred income tax assets based on current

period activity of taxable timing differences.

Our total current liabilities were $1.10 billion at May 31, 2009,

compared with $1.14 billion at May 25, 2008. The decrease in current

liabilities resulted primarily from a pay down of short-term debt with

excess cash from operations.

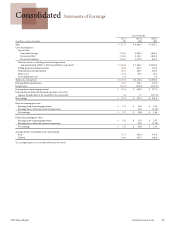

QUANTITATIVE AND QUALITATIVE

DISCLOSURES ABOUT MARKET RISK

We are exposed to a variety of market risks, including fluctuations

in interest rates, foreign currency exchange rates, compensation and

commodity prices. To manage this exposure, we periodically enter

into interest rate, foreign currency exchange, equity forwards and

commodity instruments for other than trading purposes (see Notes 1

and 10 of the Notes to Consolidated Financial Statements, included

elsewhere in this report and incorporated herein by reference).

We use the variance/covariance method to measure value at

risk, over time horizons ranging from one week to one year, at the

95 percent confidence level. At May 31, 2009, our potential losses

in future net earnings resulting from changes in foreign currency

exchange rate instruments, commodity instruments, equity forwards

and floating rate debt interest rate exposures were approximately

$21.9 million over a period of one year (including the impact of

the interest rate swap agreements discussed in Note 10 of the Notes

to Consolidated Financial Statements, included elsewhere in this

report). The value at risk from an increase in the fair value of all of

our long-term fixed rate debt, over a period of one year, was approxi-

mately $149.0 million. The fair value of our long-term fixed rate debt

during fiscal 2009 averaged $1.51 billion, with a high of $1.60 billion

and a low of $1.41 billion. Our interest rate risk management objec-

tive is to limit the impact of interest rate changes on earnings and cash

flows by targeting an appropriate mix of variable and fixed rate debt.

APPLICATION OF NEW ACCOUNTING STANDARDS

In September 2006, the FASB issued SFAS No. 157, “Fair Value

Measurements.” SFAS No. 157 defines fair value, establishes a framework

for measuring fair value and enhances disclosures about fair value

measures required under other accounting pronouncements, but does

not change existing guidance as to whether or not an instrument is

carried at fair value. For financial assets and liabilities, SFAS No. 157

is effective for fiscal years beginning after November 15, 2007, which

required us to adopt these provisions in fiscal 2009. For nonfinancial

assets and liabilities, SFAS No. 157 is effective for fiscal years beginning

after November 15, 2008, which will require us to adopt these provisions

in fiscal 2010. The adoption of SFAS No. 157 did not have a significant

impact on our consolidated financial statements.

In September 2006, the FASB issued SFAS No. 158. Effective

May 27, 2007, we implemented the recognition and measurement

provision of SFAS No. 158. The purpose of SFAS No. 158 is to improve

the overall financial statement presentation of pension and other

postretirement plans, but SFAS No. 158 does not impact the deter-

mination of net periodic benefit cost or measurement of plan assets

or obligations. SFAS No. 158 requires companies to recognize the over

or under funded status of the plan as an asset or liability as measured

by the difference between the fair value of the plan assets and the

benefit obligation and requires any unrecognized prior service costs

and actuarial gains and losses to be recognized as a component of

accumulated other comprehensive income (loss). Additionally, SFAS

No. 158 requires measurement of the funded status of pension and

postretirement plans as of the date of a company’s fiscal year ending

after December 15, 2008, the year ended May 31, 2009 for Darden.

Certain of our plans currently have measurement dates that do not

coincide with our fiscal year end and thus we were required to change

their measurement dates in fiscal 2009. As permitted by SFAS No. 158,

we used the measurements performed in fiscal 2008 to estimate the

effects of our changes to fiscal year end measurement dates. The impact

of the transition to fiscal year end measurement dates, which was

recorded as an adjustment to retained earnings as of May 31, 2009

was $0.6 million, net of tax.

In February 2007, the FASB issued SFAS No. 159 “The Fair Value

Option for Financial Assets and Financial Liabilities.” SFAS No. 159

provides companies with an option to report selected financial assets

and financial liabilities at fair value. Unrealized gains and losses on

items for which the fair value option has been elected are reported in

earnings at each subsequent reporting date. SFAS No. 159 is effective

for fiscal years beginning after November 15, 2007, which was our

fiscal 2009. The adoption of SFAS No. 159 did not have a significant

impact on our consolidated financial statements.

In March 2008, the FASB issued SFAS No. 161, “Disclosures

about Derivative Instruments and Hedging Activities.” SFAS No. 161

provides companies with requirements for enhanced disclosures

about derivative instruments and hedging activities to enable

investors to better understand their effects on a company’s financial

position, financial performance and cash flows. These requirements

include the disclosure of the fair values of derivative instruments and

their gains and losses in a tabular format. SFAS No. 161 is effective

for fiscal years beginning after November 15, 2008, which required

us to adopt these provisions in fiscal 2009. We adopted the disclosure

provisions of SFAS No. 161 as of our third quarter of fiscal 2009.

In December 2007, the FASB issued SFAS No. 141R, “Business

Combinations.” SFAS No. 141R provides companies with principles

and requirements on how an acquirer recognizes and measures in its

financial statements the identifiable assets acquired, liabilities assumed,

and any noncontrolling interest in the acquiree as well as the recogni-

tion and measurement of goodwill acquired in a business combination.

SFAS No. 141R also requires certain disclosures to enable users of the

financial statements to evaluate the nature and financial effects of the

business combination. Acquisition costs associated with the business