Red Lobster 2003 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2003 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

|

|

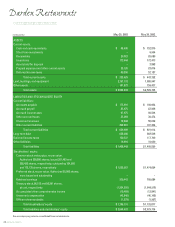

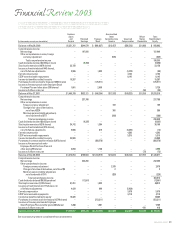

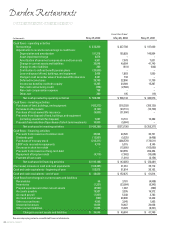

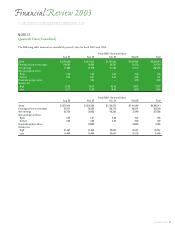

38 DARDEN RESTAURANTS

NOTE 7

Derivative Instruments and Hedging Activities

We use interest rate-related derivative instruments to manage

our exposure on debt instruments, as well as commodities deriv-

atives to manage our exposure to commodity price fluctuations.

By using these instruments, we expose ourselves, from time to

time, to credit risk and market risk. Credit risk is the failure of

the counterparty to perform under the terms of the derivative

contract. When the fair value of a derivative contract is positive,

the counterparty owes us, which creates credit risk for us. We

minimize this credit risk by entering into transactions with high-

quality counterparties. Market risk is the adverse effect on the

value of a financial instrument that results from a change in

interest rates or commodity prices. We minimize this market risk

by establishing and monitoring parameters that limit the types

and degree of market risk that may be undertaken.

Futures Contracts and Commodity Swaps

During fiscal 2003 and 2002, we entered into futures contracts

and commodity swaps to reduce the risk of natural gas and coffee

price fluctuations. To the extent these derivatives are effective in

offsetting the variability of the hedged cash flows, changes in the

derivatives’ fair value are not included in current earnings but are

reported as other comprehensive income. These changes in fair

value are subsequently reclassified into earnings when the natural

gas and coffee are purchased and used by us in our operations.

Net gains (losses) of $941 and ($276) related to these derivatives

were recognized in earnings during fiscal 2003 and 2002, respec-

tively. It is expected that $495 of net gains related to these contracts

at May 25, 2003, will be reclassified from accumulated other

comprehensive income into food and beverage costs or restaurant

expenses during the next 12 months. To the extent these derivatives

are not effective, changes in their fair value are immediately recog-

nized in current earnings. Outstanding derivatives are included in

other current assets or other current liabilities.

As of May 25, 2003, the maximum length of time over

which we are hedging our exposure to the variability in future

natural gas cash flows is 12 months. As of May 25, 2003, we are

not hedging our exposure to the variability in future coffee cash

flows. No gains or losses were reclassified into earnings during

fiscal 2003 or 2002 as a result of the discontinuance of natural

gas and coffee cash flow hedges.

Interest Rate Lock Agreement

During fiscal 2002, we entered into a treasury interest rate lock

agreement (treasury lock) to hedge the risk that the cost of a future

issuance of fixed-rate debt may be adversely affected by interest

rate fluctuations. The treasury lock, which had a $75,000 notional

principal amount of indebtedness, was used to hedge a portion

of the interest payments associated with $150,000 of debt subse-

quently issued in March 2002. The treasury lock was settled at

the time of the related debt issuance with a net gain of $267 being

recognized in other comprehensive income. The net gain on the

treasury lock is being amortized into earnings as an adjustment to

interest expense over the same period in which the related interest

costs on the new debt issuance are being recognized in earnings.

Amortization of $53 and $14 was recognized in earnings as an

adjustment to interest expense during fiscal 2003 and 2002,

respectively. It is expected that $53 of this gain will be recognized

in earnings as an adjustment to interest expense during the

next 12 months.

Interest Rate Swaps

We had interest rate swaps with a notional amount of $200,000,

which we used to convert variable rates on our long-term debt to

fixed rates effective May 30, 1995. We received the one-month

commercial paper interest rate and paid fixed-rate interest rang-

ing from 7.51 percent to 7.89 percent. The interest rate swaps

were settled during January 1996 at a cost to us of $27,670.

This cost is being recognized as an adjustment to interest expense

over the term of our 10-year, 6.375 percent notes and 20-year,

7.125 percent debentures (see Note 6).

NOTE 8

Financial Instruments

The fair values of cash equivalents, accounts receivable, and

accounts payable approximate their carrying amounts due to

their short duration. Short-term investments are carried at

amortized cost, which approximates fair value.

The carrying value and fair value of long-term debt at

May 25, 2003, was $658,086 and $740,130, respectively. The

carrying value and fair value of long-term debt at May 26, 2002,

was $662,506 and $680,115, respectively. The fair value of

long-term debt is determined based on market prices or, if

market prices are not available, the present value of the underly-

ing cash flows discounted at our incremental borrowing rates.

Darden Restaurants

Notes to Consolidated Financial Statements