Red Lobster 2001 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2001 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

NET EARNINGS AND NET EARNINGS PER SHARE

BEFORE NET RESTRUCTURING AND ASSET

IMPAIRMENT CREDIT

Net earnings for 2001 of $197.0 million, or $1.59 per

diluted share, increased 13.8 percent, compared to 2000

net earnings before net restructuring and asset impair-

ment credit of $173.1 million, or $1.31 per diluted

share. Net earnings before net restructuring and asset

impairment credit for 2000 increased 27.9 percent,

compared to net earnings before restructuring credit for

1999 of $135.3 million, or $0.96 per diluted share.

NET EARNINGS AND NET EARNINGS PER SHARE

Net earnings for 2001 of $197.0 million ($1.59 per diluted

share) compared with net earnings after net restructuring

and asset impairment credit for 2000 of $176.7 million

($1.34 per diluted share) and net earnings after restruc-

turing credit of $140.5 million ($0.99 per diluted share).

During 1997, an after-tax restructuring and asset

impairment charge of $145.4 million ($0.93 per diluted

share) was taken related to low-performing restaurant

properties in the U.S. and Canada and other long-lived

assets, including those restaurants that have been closed.

The pre-tax charge included approximately $160.7 mil-

lion of non-cash charges primarily related to the write-

down of buildings and equipment to net realizable value

and approximately $69.2 million of charges to be settled

in cash related to carrying costs of buildings and equip-

ment prior to their disposal, lease buy-out provisions,

employee severance, and other costs. Cash required to

carry out these activities is being provided by operations

and the sale of closed properties.

After-tax restructuring credits of $5.2 million and

$5.2 million were taken in the fourth quarter of 2000 and

1999, respectively, as the Company reversed portions of

its 1997 restructuring liability. The 2000 reversal prima-

rily resulted from favorable lease terminations. The 1999

reversal primarily resulted from the Company’s decision

to close fewer restaurants than identified for closure as

part of the initial restructuring action. The credits had no

effect on the Company’s cash flow.

During 2000, an after-tax asset impairment charge

of $1.6 million was taken in the fourth quarter related

to additional write-downs of the value of properties

held for disposition.

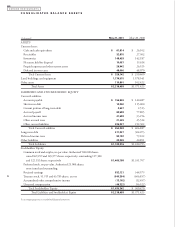

FINANCIAL CONDITION

Short-term debt totaled $12.0 million as of May 27,

2001, down from $115.0 million at May 28, 2000.

The decrease resulted primarily from the Company’s

issuance of long-term debt, in which the proceeds

were used to repay short-term debt.

LIQUIDITY AND CAPITAL RESOURCES

The Company intends to manage its business and its

financial ratios to maintain an investment grade bond

rating, which allows access to financing at reasonable

costs. Currently, the Company’s publicly issued long-term

debt carries “Baa1” (Moody’s Investors Service), “BBB+”

(Standard & Poor’s), and “BBB+” (Fitch) ratings. The

Company’s commercial paper has ratings of “P-2” (Moody’s

Investors Service), “A-2” (Standard & Poor’s), and “F-2”

(Fitch). Such ratings are only accurate as of the date of this

report and have been obtained with the understanding

that Moody’s Investors Service, Standard & Poor’s, and

Fitch will continue to monitor the credit of the Company

and make future adjustments to such ratings to the extent

warranted. The ratings may be changed, superseded, or

withdrawn at any time.

Darden’s long-term debt includes $150 million of

unsecured 6.375 percent notes due in February 2006

and $100 million of unsecured 7.125 percent deben-

tures due in February 2016. In September 2000, the

Company also issued $150 million of unsecured 8.375

percent senior notes due in September 2005. Proceeds

of the issuance were used to repay short-term debt.

In November 2000, Darden filed a prospectus

supplement with the Securities and Exchange Commis-

sion allowing the Company to offer up to $350 million

of medium-term notes from time to time. The notes will

be unsecured, may bear interest at either fixed or floating

rates, and may have maturity dates of nine months or

more after issuance. In April 2001, the Company issued

$75 million of 7.45 percent fixed rate notes under this

program with a maturity date of April 2011. Proceeds

of the issuance were used to repay short-term debt.

As of May 27, 2001, Darden’s long-term debt also

includes a $44.5 million commercial bank loan that is

used to support two loans from the Company to the

Employee Stock Ownership Plan portion of the Darden

Savings Plan.

19

2001

DARDEN RESTAURANTS