JetBlue Airlines 2015 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2015 JetBlue Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

|

|

JETBLUE AIRWAYS CORPORATION-2015Annual Report60

PART II

ITEM 8Financial Statements and Supplementary Data

NOTE 13 Fair Value

Under the Fair Value Measurements and Disclosures topic of the Codification,

disclosures are required about how fair value is determined for assets and

liabilities and a hierarchy for which these assets and liabilities must be grouped

is established, based on significant levels of inputs as follows:

•

Level 1 quoted prices in active markets for identical assets or liabilities;

•Level 2 quoted prices in active markets for similar assets and liabilities

and inputs that are observable for the asset or liability; or

•

Level 3 unobservable inputs for the asset or liability, such as discounted

cash flow models or valuations.

The determination of where assets and liabilities fall within this hierarchy

is based upon the lowest level of input that is significant to the fair value

measurement.

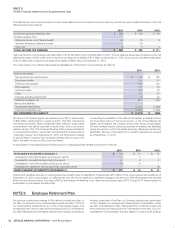

The following is a listing of our assets and liabilities required to be measured at fair value on a recurring basis and where they are classified within the

fair value hierarchy (in millions):

As of December 31, 2015

Level1 Level2 Level3 Total

Assets

Cash equivalents $ 147 $ — $ — $ 147

Available-for-sale investment securities 75 180 — 255

Aircraft fuel derivatives — — — —

$ 222 $ 180 $ — $ 402

Liabilities

Aircraft fuel derivatives — 5 — 5

Interest rate swap — — — —

$ — $ 5 $ — $ 5

As of December 31, 2014

Level1 Level2 Level3 Total

Assets

Cash equivalents $ 153 $ — $ — $ 153

Available-for-sale investment securities — 125 — 125

Aircraft fuel derivatives $ — $ — $ — $ —

$ 153 $ 125 $ — $ 278

Liabilities

Aircraft fuel derivatives $ — $ 102 $ — $ 102

Interest rate swap — 1 — 1

$ — $ 103 $ — $ 103

The carrying values of all other financial instruments approximated their

fair values at December 31, 2015 and 2014. Refer to Note 2 for fair value

information related to our outstanding debt obligations as of December

31, 2015 and 2014.

Cash equivalents

Our cash equivalents include money market securities and commercial

paper which are readily convertible into cash, have maturities of 90 days

or less when purchased and are considered to be highly liquid and easily

tradable. These securities are valued using inputs observable in active

markets for identical securities and are therefore classified as Level 1

within our fair value hierarchy.

Available-for-sale investment securities

Included in our available-for-sale investment securities are time deposits,

commercial paper and treasury bills. The fair values of these instruments

are based on observable inputs in non-active markets, which are therefore

classified as Level 2 in the hierarchy. We did not record any material gains

or losses on these securities during the year ended December 31, 2015

or 2014.

Aircraft fuel derivatives

Our aircraft fuel derivatives include swaps, caps, collars, and basis swaps

which are not traded on public exchanges. Their fair values are determined

using a market approach based on inputs that are readily available from

public markets for commodities and energy trading activities; therefore,

they are classified as Level 2 inputs. The data inputs are combined into

quantitative models and processes to generate forward curves and

volatilities related to the specific terms of the underlying hedge contracts.

Interest rate swaps

The fair values of our interest rate swaps are based on inputs received

from the related counterparty, which are based on observable inputs for

active swap indications in quoted markets for similar terms. Their fair

values are determined using a market approach based on inputs that

are readily available from public markets; therefore, they are classified

as Level 2 inputs.