JetBlue Airlines 2015 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2015 JetBlue Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

|

|

JETBLUE AIRWAYS CORPORATION-2015Annual Report 59

PART II

ITEM 8Financial Statements and Supplementary Data

Interest rate swaps

The interest rate swap agreements we had outstanding as of December31,

2015 effectively swap floating rate debt for fixed rate debt, taking advantage

of lower borrowing rates in existence at the time of the hedge transaction

as compared to the date our original debt instruments were executed. As

of December 31, 2015, we had $16 million in notional debt outstanding

related to these swaps, which cover certain interest payments through

August 2016. The notional amount decreases over time to match scheduled

repayments of the related debt. Refer to Note 2 for information on the debt

outstanding related to these swap agreements.

All of our outstanding interest rate swap contracts qualify as cash flow hedges

in accordance with the Derivatives and Hedging topic of the Codification.

Since all of the critical terms of our swap agreements match the debt to

which they pertain, there was no ineffectiveness relating to these interest

rate swaps for the years ended December 31, 2015, 2014 or 2013, and all

related unrealized losses were deferred in accumulated other comprehensive

income. We recognized approximately $1 million, $1 million and $8 million

in additional interest expense as the related interest payments were made

during the years ended December 31, 2015, 2014 and 2013, respectively.

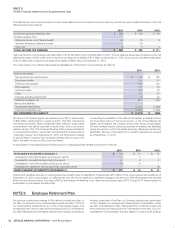

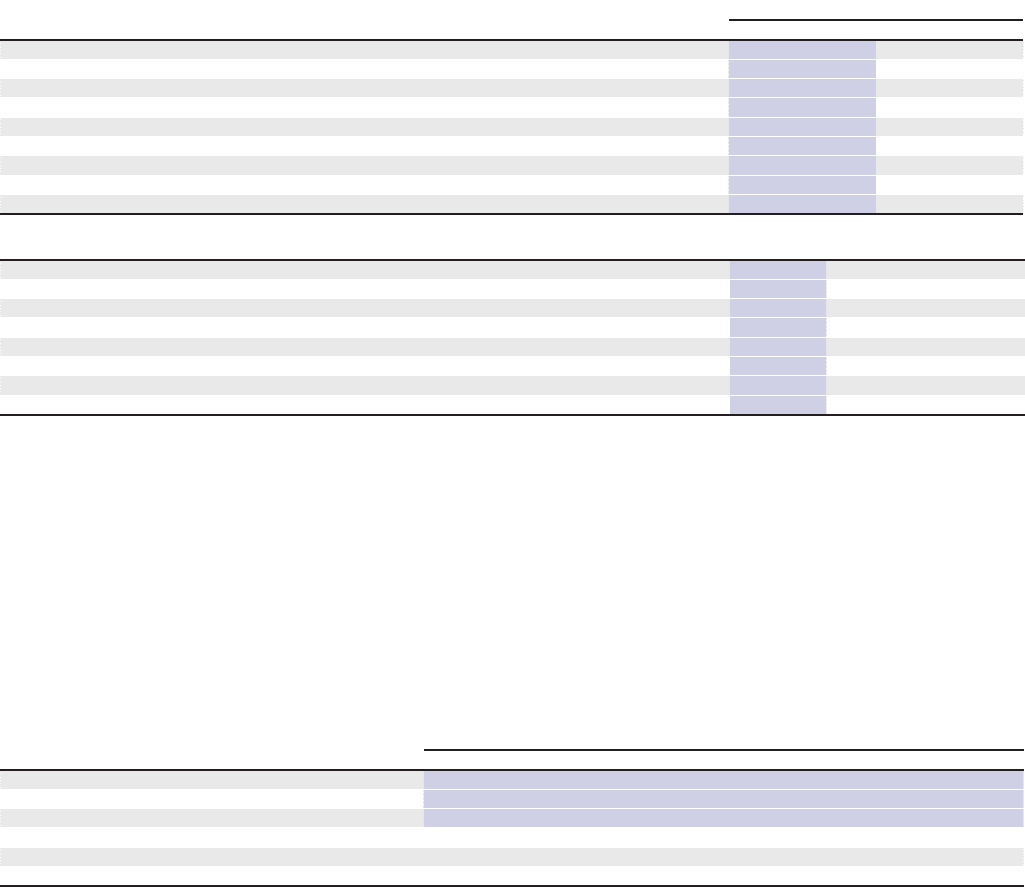

The table below reflects quantitative information related to our derivative instruments and where these amounts are recorded in our financial statements

(dollar amounts in millions).

As of December 31,

2015 2014

Fuel derivatives

Asset fair value recorded in prepaid expenses and other(1) $ — $ —

Liability fair value recorded in other accrued liabilities(1) 5 102

Longest remaining term (months) 12 12

Hedged volume (barrels, in thousands) 900 2,808

Estimated amount of existing losses expected to be reclassified into earnings in the next 12 months 4 102

Interest rate derivatives

Liability fair value recorded in other long term liabilities(2) — 1

Estimated amount of existing losses expected to be reclassified into earnings in the next 12 months — 1

2015 2014 2013

Fuel derivatives

Hedge effectiveness losses recognized in aircraft fuel expense $ 126 $ 30 $ 10

(Losses) gains on derivatives not qualifying for hedge accounting recognized in other expense (1) 2 —

Hedge losses on derivatives recognized in comprehensive income 29 134 6

Percentage of actual consumption economically hedged 17% 20% 21%

Interest rate derivatives

Hedge losses on derivatives recognized in interest expense 1 1 8

Hedge gains on derivatives recognized in comprehensive income — — 1

(1) Gross asset or liability of each contract prior to consideration of offsetting positions with each counterparty and prior to impact of collateral paid.

(2) Gross liability prior to impact of collateral posted.

Any outstanding derivative instrument exposes us to credit loss in connection

with our fuel contracts in the event of nonperformance by the counterparties

to the agreements, but we do not expect any of our counterparties will

fail to meet their obligations. The amount of such credit exposure is

generally the fair value of our outstanding contracts for which we are in a

liability position. To manage credit risks we select counterparties based on

credit assessments, limit our overall exposure to any single counterparty

and monitor the market position with each counterparty. Some of our

agreements require cash deposits from either counterparty if market risk

exposure exceeds a specified threshold amount.

We have master netting arrangements with our counterparties allowing

us the right of offset to mitigate credit risk in derivative transactions. The

financial derivative instrument agreements we have with our counterparties

may require us to fund all, or a portion of, outstanding loss positions

related to these contracts prior to their scheduled maturities. The amount

of collateral posted, if any, is periodically adjusted based on the fair value

of the hedge contracts. Our policy is to offset the liabilities represented

by these contracts with any cash collateral paid to the counterparties.

The impact of offsetting derivative instruments is depicted below (in millions):

Gross Amount of

Recognized

Gross Amount of

Cash Collateral

Net Amount Presented

in Balance Sheet

Assets Liabilities Offset Assets Liabilities

As of December 31, 2015

Fuel derivatives $ — $ 5 $ — $ — $ 5

Interest rate derivatives — — — — —

As of December 31, 2014

Fuel derivatives $ — $ 102 $ 51 $ — $ 51

Interest rate derivatives — 1 1 — —