Freddie Mac 2010 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2010 Freddie Mac annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

|

|

more classes designed to meet the investment criteria and portfolio needs of different investors by creating classes of

securities with varying maturities, payment priorities and coupons, each of which represents a beneficial ownership interest

in a separate portion of the cash flows of the underlying collateral. Usually, the cash flows are divided to modify the relative

exposure of different classes to interest-rate risk, or to create various coupon structures. The simplest division of cash flows

is into principal-only and interest-only classes. Other securities we issue can involve the creation of sequential payment and

planned or targeted amortization classes. In a sequential payment class structure, one or more classes receive all or a

disproportionate percentage of the principal payments on the underlying mortgage assets for a period of time until that class

or classes is retired, following which the principal payments are directed to other classes. Planned or targeted amortization

classes involve the creation of classes that have relatively more predictable amortization schedules across different

prepayment scenarios, thus reducing prepayment risk, extension risk, or both.

Our REMICs and Other Structured Securities represent beneficial interests in pools of PCs and/or certain other types of

mortgage-related assets. We create these securities primarily by using PCs or previously issued REMICs and Other

Structured Securities as the underlying collateral. Similar to our PCs, we guarantee the payment of principal and interest to

the holders of tranches of our REMICs and Other Structured Securities. We do not charge a management and guarantee fee

for these securities if the underlying collateral is already guaranteed by us since no additional credit risk is introduced.

Because the collateral underlying nearly all of our single-family REMICs and Other Structured Securities consists of other

mortgage-related securities that we guarantee, there are no concentrations of credit risk in any of the classes of these

securities that are issued, and there are no economic residual interests in the related securitization trust. The following

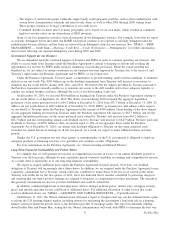

diagram provides a general example of how we create REMICs and Other Structured Securities.

REMICs and Other Structured Securities

Security Dealer

PCs

Freddie Mac

(administrator)

TRUST

PCs

Security

Classes

Security

Classes

Transaction Fee

We issue many of our REMICs and Other Structured Securities in transactions in which securities dealers or investors

sell us mortgage-related assets or we use our own mortgage-related assets (e.g., PCs and REMICs and Other Structured

Securities) in exchange for the REMICs and Other Structured Securities. Since the creation of REMICs and Other Structured

Securities allows for setting differing terms for specific classes of investors, our issuance of these securities can expand the

range of investors in our mortgage-related securities to include those seeking specific security attributes. For REMICs and

Other Structured Securities that we issue to third parties, we typically receive a transaction, or resecuritization, fee. This

transaction fee is compensation for facilitating the transaction, as well as future administrative responsibilities.

15 Freddie Mac