Dillard's 2004 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2004 Dillard's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

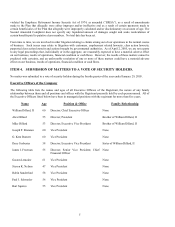

Management of the Company believes the following critical accounting policies, among others, affect its more

significant judgments and estimates used in preparation of the Consolidated Financial Statements.

Merchandise inventory. Approximately 97% of the inventories are valued at lower of cost or market using the retail

last-in, first-out (“LIFO”) inventory method. Under the retail inventory method (“RIM”), the valuation of inventories at

cost and the resulting gross margins are calculated by applying a calculated cost to retail ratio to the retail value of

inventories. RIM is an averaging method that is widely used in the retail industry due to its practicality. Additionally, it

is recognized that the use of RIM will result in valuing inventories at the lower of cost or market if markdowns are

currently taken as a reduction of the retail value of inventories. Inherent in the RIM calculation are certain significant

management judgments including, among others, merchandise markon, markups, and markdowns, which significantly

impact the ending inventory valuation at cost as well as the resulting gross margins. Management believes that the

Company’s RIM provides an inventory valuation which results in a carrying value at the lower of cost or market. The

remaining 3% of the inventories are valued at lower of cost or market using the specific identified cost method.

Allowance for doubtful accounts. In 2004, the Company sold substantially all of its accounts receivable to GE and no

longer maintains an allowance for doubtful accounts.

Prior to the sale, the accounts receivable from the Company’s private label credit card sales were subject to credit losses.

The Company maintained allowances for uncollectible accounts for estimated losses resulting from the inability of its

customers to make required payments. The adequacy of the allowance was based on historical experience with similar

customers including write-off trends, current aging information and year-end balances. Bankruptcies and recoveries

used in the allowance calculation were projected based on qualitative factors such as current and expected consumer and

economic trends.

Merchandise vendor allowances. The Company receives concessions from its merchandise vendors through a variety

of programs and arrangements, including co-operative advertising, payroll reimbursements and markdown

reimbursement programs. Co-operative advertising allowances are reported as a reduction of advertising expense in the

period in which the advertising occurred. Payroll reimbursements are reported as a reduction of payroll expense in the

period in which the reimbursement occurred. All other merchandise vendor allowances are recognized as a reduction of

cost purchases when received. Accordingly, a reduction or increase in vendor concessions has an inverse impact on cost

of sales and/or selling and administrative expenses.

Insurance accruals. The Company’s consolidated balance sheets include liabilities with respect to self-insured workers’

compensation and general liability claims. The Company estimates the required liability of such claims, utilizing an

actuarial method, based upon various assumptions, which include, but are not limited to, our historical loss experience,

projected loss development factors, actual payroll and other data. The required liability is also subject to adjustment in

the future based upon the changes in claims experience, including changes in the number of incidents (frequency) and

changes in the ultimate cost per incident (severity).

Finite-lived assets. The Company evaluates the fair value and future benefits of finite-lived assets whenever events and

changes in circumstances suggest. The Company performs an analysis of the anticipated undiscounted future net cash

flows of the related finite-lived assets. If the carrying value of the related asset exceeds the undiscounted cash flows, the

carrying value is reduced to its fair value. Various factors including future sales growth and profit margins are included

in this analysis. To the extent these future projections or the Company’s strategies change, the conclusion regarding

impairment may differ from the current estimates.

Goodwill. The Company evaluates goodwill annually and whenever events and changes in circumstances suggest that

the carrying amount may not be recoverable from its estimated future cash flows. To the extent these future projections

or our strategies change, the conclusion regarding impairment may differ from the current estimates.

Income taxes. Temporary differences arising from differing treatment of income and expense items for tax and financial

reporting purposes result in deferred tax assets and liabilities that are recorded on the balance sheet. These balances, as

well as income tax expense, are determined through management’s estimations, interpretation of tax law for multiple

jurisdictions and tax planning. If the Company’s actual results differ from estimated results due to changes in tax laws,

13