Airtran 2004 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2004 Airtran annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

23

2004 Annual Report

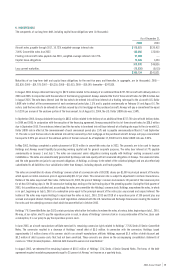

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

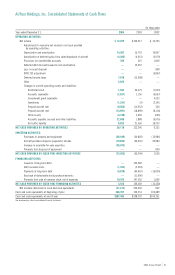

BASIS OF PRESENTATION AND BUSINESS

Our consolidated financial statements include the accounts of AirTran Holdings, Inc. (Holdings) and our wholly-owned subsidiaries, including our

principal subsidiary, AirTran Airways, Inc. (Airways). Significant intercompany accounts and transactions have been eliminated in consolidation.

Airways, Inc. offers scheduled air transportation of passengers, serving short-haul markets primarily in the eastern United States.

USE OF ESTIMATES

The preparation of consolidated financial statements in conformity with accounting principles generally accepted in the United States requires us to

make estimates and assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes. Actual results

inevitably will differ from those estimates.

CASH, CASH EQUIVALENTS AND RESTRICTED CASH

We consider all highly liquid investments with maturities of three months or less when purchased to be cash equivalents. Restricted cash primarily

represents amounts escrowed relating to aircraft leases and amounts relating to air traffic liability.

SHORT-TERM INVESTMENTS

Short-term investments consist of auction rate securities with auction reset periods of less than 12 months, classified as available-for-sale

securities and stated at fair value.

ACCOUNTS RECEIVABLE

Accounts receivable are due primarily from major credit card processors, travel agents, co-branded credit card arrangements, overpayments made

to a wet-lease partner, and from municipalities related to guaranteed revenue agreements. We provide an allowance for doubtful accounts equal to

the estimated losses expected to be incurred in the collection of accounts receivable based on historical credit card chargebacks and miscellaneous

receivables based on specific analysis. Collateral is generally not required on accounts receivable.

INVENTORIES

Inventories consist of expendable aircraft spare parts, supplies and prepaid aircraft fuel. These items are stated at the lower of cost or market using

the first-in, first-out method (FIFO). These items are charged to expense when used. Allowances for obsolescence are provided over the estimated

useful life of the related aircraft and engines for spare parts expected to be on hand at the date aircraft are retired from service.

PROPERTY AND EQUIPMENT

Property and equipment are stated on the basis of cost. Flight equipment is depreciated to its salvage values of 10%, using the straight-line method.

The estimated salvage values and depreciable lives are periodically reviewed for reasonableness, and revised if necessary. The estimated useful lives

for airframes, engines and aircraft parts are 30 years. Other property and equipment is depreciated over three to 10 years.

MEASUREMENT OF IMPAIRMENT

Effective January 1, 2002, we adopted Statement of Financial Accounting Standards No. 144 (SFAS 144), “Accounting for the Impairment or Disposal

of Long-Lived Assets.” SFAS 144 supercedes Statement of Financial Accounting Standards No. 121 (SFAS 121), “Accounting for the Impairment of

Long-Lived Assets and for Long-Lived Assets to be Disposed Of.” The adoption of SFAS 144 had no effect on our results of operations. We record

impairment losses on long-lived assets used in operations when events or circumstances indicate that the assets may be impaired, the undiscounted

cash flows estimated to be generated by those assets are less than the net book value of those assets and the fair value is less than the net book

value.

INTANGIBLES

The trade name and intangibles resulting from business acquisitions (goodwill) consist of cost in excess of net assets acquired. We adopted

Statement of Financial Accounting Standards No. 142 (SFAS 142), “Goodwill and Other Intangible Assets,” effective January 1, 2002. Pursuant to

SFAS 142, goodwill and indefinite-lived intangibles, such as trade names, are no longer amortized but are subject to periodic impairment reviews.

We performed annual impairment tests in the fourth quarter of 2004, 2003 and 2002. Our tests indicated that we did not have any impairment of

our trade name or of our goodwill. Accumulated amortization was $6.5 million at December 31, 2004, 2003 and 2002.

CAPITALIZED INTEREST

Interest attributable to funds used to finance the acquisition of new aircraft is capitalized as an additional cost of the related asset. Interest

is capitalized at our weighted-average interest rate on long-term debt or, where applicable, the interest rate related to specific borrowings.

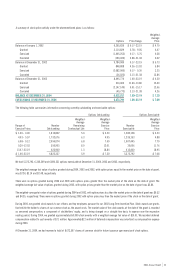

Capitalization of interest ceases when the asset is placed in service. For the years ended December 31, 2004, 2003 and 2002, the Company incurred

approximately $19.4 million, $28.3 million and $29.2 million in interest expense, respectively, net of capitalized interest of $7.3 million, $2.0 million

and $4.8 million, respectively.

Notes to Consolidated Financial Statements