Air New Zealand 2009 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2009 Air New Zealand annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

Upon initial recognition, assets held under finance leases are measured at amounts equal to the lower of their fair value and the present value of the

minimum lease payments at inception of the lease. A corresponding liability is also established.

Subsequent to initial recognition, the asset is accounted for in accordance with the accounting policy applicable to that asset.

Manufacturers’ credits

The Group receives credits from manufacturers in connection with the acquisition of certain aircraft and engines. These credits are recorded as a

reduction to the cost of the related aircraft and engines. When the aircraft are held under operating leases, the credits are deferred and deducted from

the operating lease rentals on a straight-line basis over the period of the related lease as deferred credits.

DEPRECIATION

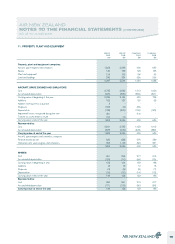

Aircraft

Depreciation of the aircraft fleet is calculated to write down the cost of these assets on a straight line basis to an estimated residual value over their

economic lives. The aircraft and related engines, simulators and spares are being depreciated on a straight line basis as follows:

Airframe 10 - 22 years

Engines 5 – 22 years

Airframe inspections period to next similar inspection

Engine overhauls period to next overhaul

The residual values of aircraft are reviewed annually by reference to Avitas projected values.

Non-aircraft

Non-aircraft assets are depreciated on a straight line basis using the following estimated economic lives:

Buildings 50 – 100 years

Aircraft specific plant and equipment 10 – 20 years

Non-aircraft specific leasehold improvements, plant, equipment, furniture and vehicles 3 - 10 years

Gains and losses on disposal are determined by comparing proceeds with carrying amounts. These are included in the Statement of Financial

Performance.

INTANGIBLE ASSETS

Goodwill

Goodwill represents the cost of an acquisition over and above the fair value of the Group’s share of the net identifiable assets acquired. Goodwill arising

on acquisition of a subsidiary is included in intangible assets. Goodwill arising on acquisition of an associate is included in the carrying value of the

investment in that associate. Goodwill is tested annually for impairment and carried at cost less accumulated impairment losses. Gains and losses on the

disposal of an entity include the carrying amount of goodwill relating to the entity sold.

Computer software and licences

Computer software acquired, which is not an integral part of a related hardware item, is recognised as an intangible asset. The costs incurred internally

in developing computer software are also recognised as intangible assets where the Group has a legal right to use the software and the ability to obtain

future economic benefits from that software. Acquired software licences are capitalised on the basis of the costs incurred to acquire and bring to use the

specific software.

These assets have a finite life and are amortised on a straight-line basis over their estimated useful lives of three to five years.

Expenditure on research activities is recognised as an expense in the period in which it is incurred.

IMPAIRMENT

Non-financial assets are reviewed at each reporting date to determine whether there are any indicators that the carrying amount may not be recoverable.

If any such indicators exist, the asset’s recoverable amount is estimated. The recoverable amount is the higher of an asset’s fair value less costs to

sell and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a discount rate that reflects

current market assessments of the time value of money and the risks specific to the asset. An impairment loss is recognised in the Statement of

Financial Performance for the amount by which the asset’s carrying amount exceeds its recoverable amount. For the purposes of assessing impairment,

assets are grouped at the lowest level for which there are separately identifiable cash flows (cash-generating units).

Aircraft are operated by the airline as a single network and are assessed for impairment as one cash-generating unit, inclusive of related infrastructural

assets. Estimated net cash flows used in determining recoverable amounts are based on the directors’ current assessment of the Group’s future trading

prospects and the assets’ ultimate net sale proceeds and have been discounted to their net present value. Aircraft which have been withdrawn from

service and have no intention of being reintroduced into the operating fleet are assessed for impairment on an individual basis.

AIR NEW ZEALAND

STATEMENT OF ACCOUNTING POLICIES (CONTINUED)

FOR THE YEAR TO 30 JUNE 2009

10