Xcel Energy 2005 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2005 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

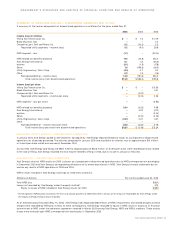

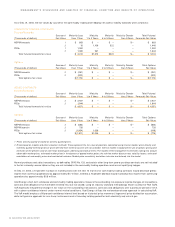

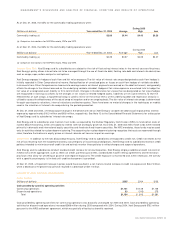

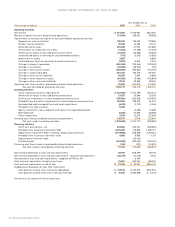

As of Dec. 31, 2005, the VaRs for the commodity trading operations were:

During 2005

(Millions of dollars) Year ended Dec. 31, 2005 Average High Low

Commodity trading

(a)

$2.06 $1.44 $4.43 $0.26

(a) Comprises transactions for NSP-Minnesota, PSCo and SPS.

As of Dec. 31, 2004, the VaRs for the commodity trading operations were: During 2004

(Millions of dollars) Year ended Dec. 31, 2004 Average High Low

Commodity trading

(a)

$0.29 $0.97 $2.09 $0.27

(a) Comprises transactions for NSP-Minnesota, PSCo and SPS.

Interest Rate Risk

Xcel Energy and its subsidiaries are subject to the risk of fluctuating interest rates in the normal course of business.

Xcel Energy’s policy allows interest rate risk to be managed through the use of fixed rate debt, floating rate debt and interest rate derivatives

such as swaps, caps, collars and put or call options.

Xcel Energy engages in hedges of cash flow and fair value exposure. The fair value of interest rate swaps designated as cash flow hedges is

initially recorded in Other Comprehensive Income. Reclassification of unrealized gains or losses on cash flow hedges of variable rate debt

instruments from Other Comprehensive Income into earnings occurs as interest payments are accrued on the debt instrument, and generally

offsets the change in the interest accrued on the underlying variable rate debt. Hedges of fair value exposure are entered into to hedge the

fair value of a recognized asset, liability or firm commitment. Changes in the derivative fair values that are designated as fair value hedges

are recognized in earnings as offsets to the changes in fair values of related hedged assets, liabilities or firm commitments. To test the

effectiveness of such swaps, a hypothetical swap is used to mirror all the critical terms of the underlying debt and regression analysis is

utilized to assess the effectiveness of the actual swap at inception and on an ongoing basis. The fair value of interest rate swaps is determined

through counterparty valuations, internal valuations and broker quotes. There have been no material changes in the techniques or models

used in the valuation of interest rate swaps during the periods presented.

At Dec. 31, 2005 and 2004, a 100-basis-point change in the benchmark rate on Xcel Energy’s variable rate debt would impact pretax interest

expense by approximately $10.3 million and $6.8 million, respectively. See Note 12 to the Consolidated Financial Statements for a discussion

of Xcel Energy and its subsidiaries’ interest rate swaps.

Xcel Energy and its subsidiaries also maintain trust funds, as required by the Nuclear Regulatory Commission (NRC), to fund certain costs of

nuclear decommissioning, which are subject to interest rate risk and equity price risk. As of Dec. 31, 2005 and 2004, these funds were invested

primarily in domestic and international equity securities and fixed-rate fixed-income securities. Per NRC mandates, these funds may be used

only for activities related to nuclear decommissioning. The accounting for nuclear decommissioning recognizes that costs are recovered through

rates; therefore fluctuations in equity prices or interest rates do not have an impact on earnings.

Credit Risk

In addition to the risks discussed previously, Xcel Energy and its subsidiaries are exposed to credit risk. Credit risk relates to the

risk of loss resulting from the nonperformance by a counterparty of its contractual obligations. Xcel Energy and its subsidiaries maintain credit

policies intended to minimize overall credit risk and actively monitor these policies to reflect changes and scope of operations.

Xcel Energy and its subsidiaries conduct standard credit reviews for all counterparties. Xcel Energy employs additional credit risk control

mechanisms when appropriate, such as letters of credit, parental guarantees, standardized master netting agreements and termination

provisions that allow for offsetting of positive and negative exposures. The credit exposure is monitored and, when necessary, the activity

with a specific counterparty is limited until credit enhancement is provided.

At Dec. 31, 2005, a 10-percent increase in prices would have resulted in a net mark-to-market increase in credit risk exposure of $44.2 million,

while a decrease of 10 percent would have resulted in a decrease of $41.1 million.

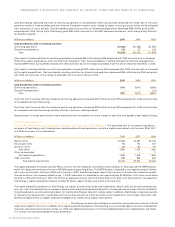

LIQUIDITY AND CAPITAL RESOURCES

CASH FLOWS

(Millions of dollars) 2005 2004 2003

Cash provided by (used in) operating activities

Continuing operations $1,131 $1,128 $1,106

Discontinued operations 53 (315) 275

Total $1,184 $ 813 $1,381

Cash provided by operating activities for continuing operations was basically unchanged for 2005 and 2004. Cash provided by operating

activities for discontinued operations increased $368 million during 2005 compared with 2004. During 2004, Xcel Energy paid $752 million

pursuant to the NRG settlement agreement, which was partially offset by tax benefits received.

XCEL ENERGY 2005 ANNUAL REPORT 33

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS