Xcel Energy 2005 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2005 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

measured and recognized based on the grant-date fair value using an option-pricing model (such as Black-Scholes or Binomial) that considers at

least six factors identified in SFAS No. 123R. An expense related to the difference between the grant-date fair value and the purchase price

would be recognized over the vesting period of the options. Under previous guidance, companies were allowed to initially estimate forfeitures

or recognize them as they actually occurred. SFAS No. 123R requires companies to estimate forfeitures on the date of grant and to adjust

that estimate when information becomes available that suggests actual forfeitures will differ from previous estimates. Revisions to forfeiture

estimates will be recorded as a cumulative effect of a change in accounting estimate in the period in which the revision occurs.

Previous accounting guidance allowed for compensation expense related to performance share plans to be reversed if the target was not met.

However, under SFAS No. 123R, compensation expense for performance share plans that expire unexercised due to the company’s failure to

reach a certain target stock price cannot be reversed. Any accruals made for Xcel Energy’s restricted stock unit plan that were granted in 2004

and based on a total shareholder return could not be reversed if the target was not met. Implementation of SFAS No. 123R is required for

annual periods beginning after June 15, 2005. Xcel Energy is required to adopt the provisions in the first quarter of 2006. Implementation is

not expected to have a material impact on net income or earnings per share.

Accounting for Uncertain Tax Positions

In July 2004, the FASB discussed potential changes or clarifications in the criteria for recognition

of income tax benefits, which may result in raising the threshold for recognizing tax benefits that have some degree of uncertainty. In July 2005,

the FASB issued an exposure draft on accounting for uncertain tax positions under SFAS No. 109 – “Accounting for Income Taxes.” As issued,

the exposure draft would have been effective Dec. 31, 2005, and only tax benefits that meet the “ probable” recognition threshold would be

recognized or continue to be recognized on the effective date. Initial derecognition amounts would be reported as a cumulative effect of a

change in accounting principle.

Subsequent to the comment period that closed in September 2005, the FASB announced that the effective date of its new interpretation will

be delayed, with a revised pronouncement to be released no earlier than the first quarter of 2006. In redeliberations in November 2005, the

FASB decided that the benefit recognition approach in the exposure draft should be retained, but that the initial recognition threshold should

be “ more likely than not” rather than “ probable.” In redeliberations on Jan. 11, 2006, the FASB addressed the issues of transition and effective

date. For Xcel Energy, the new interpretation, if and when issued, is likely to be effective beginning Jan. 1, 2007, with any cumulative effect of

the change reflected in retained earnings. Although Xcel Energy has not assessed the impact of a new recognition threshold on all of its open

tax positions, based on available information, it believes that its COLI tax position meets the “ more likely than not” threshold, and therefore

it plans to continue to recognize all COLI tax benefits in full. See Factors Affecting Results of Continuing Operations – Tax Matters for further

discussion of this matter.

DERIVATIVES, RISK MANAGEMENT AND MARKET RISK

In the normal course of business, Xcel Energy and its subsidiaries are exposed to a variety of market risks. Market risk is the potential loss

that may occur as a result of changes in the market or fair value of a particular instrument or commodity. All financial and commodity-related

instruments, including derivatives, are subject to market risk. These risks, as applicable to Xcel Energy and its subsidiaries, are discussed in

further detail later.

Commodity Price Risk

Xcel Energy and its subsidiaries are exposed to commodity price risk in their electric and natural gas operations.

Commodity price risk is managed by entering into both long- and short-term physical purchase and sales contracts for electric capacity, energy

and energy-related products, and for various fuels used in generation and distribution activities. Commodity price risk is also managed through

the use of financial derivative instruments. Xcel Energy’s risk-management policy allows it to manage commodity price risk within each

rate-regulated operation to the extent such exposure exists.

Short-Term Wholesale and Commodity Trading Risk

Xcel Energy’s subsidiaries conduct various short-term wholesale and commodity

trading activities, including the purchase and sale of capacity, energy and energy-related instruments. These marketing activities are primarily

focused on specific regions where market knowledge and experience have been obtained and are generally less than one year in length.

Xcel Energy’s risk-management policy allows management to conduct these activities within approved guidelines and limitations as approved

by the company’s risk-management committee, which is made up of management personnel not directly involved in the activities governed

by the policy.

Certain contracts and financial instruments within the scope of these activities qualify for hedge accounting treatment under SFAS No. 133 –

“Accounting for Derivative Instruments and Hedging Activities,” as amended (SFAS No. 133).

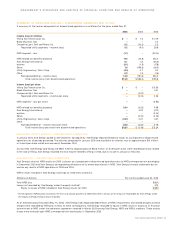

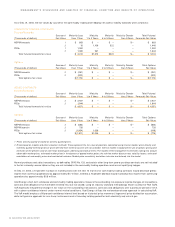

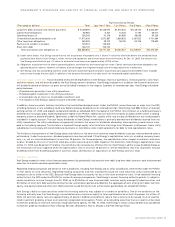

The fair value of the commodity trading contracts as of Dec. 31, 2005, was as follows:

(Millions of dollars)

Fair value of trading contracts outstanding at Jan. 1, 2005 $ –

Contracts realized or settled during the year (6.1)

Fair value of trading contract additions and changes during the year 10.0

Fair value of contracts outstanding at Dec. 31, 2005 $ 3.9

XCEL ENERGY 2005 ANNUAL REPORT 31

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS