Xcel Energy 2003 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2003 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

64 XCEL ENERGY 2003 ANNUAL REPORT

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

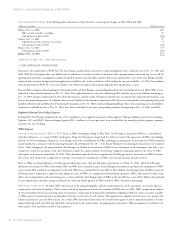

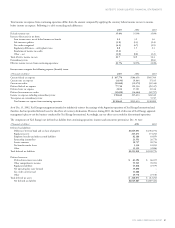

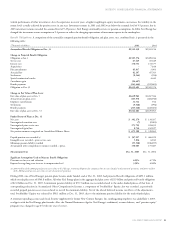

Registered holding companies and certain of their subsidiaries, including Xcel Energy and its utility subsidiaries, are limited, under PUHCA, in their

ability to issue securities. Such registered holding companies and their subsidiaries may not issue securities unless authorized by an exemptive rule or

order of the SEC. Because Xcel Energy does not qualify for any of the main exemptive rules, it sought and received financing authority from the SEC

under PUHCA for various financing arrangements. Xcel Energy’s current financing authority permits it, subject to satisfaction of certain conditions, to

issue through June 30, 2005, up to $2.5 billion of common stock and long-term debt and $1.5 billion of short-term debt at the holding company level.

Xcel Energy has $2 billion of long-term debt outstanding and common stock, including the $400 million credit facility.

Xcel Energy’s ability to issue securities under the financing authority is subject to a number of conditions. One of the conditions of the financing

authority is that Xcel Energy’s ratio of common equity to total capitalization, on a consolidated basis, be at least 30 percent. As of Dec. 31, 2003,

such common equity ratio was approximately 43 percent. Additional conditions require that a security to be issued that is rated, be rated investment grade by

at least one nationally recognized rating agency. Finally, all outstanding securities (except preferred stock) that are rated must be rated investment grade by at

least one nationally recognized rating agency. As of Dec. 31, 2003, Xcel Energy’s senior unsecured debt was considered investment grade by at least one

nationally recognized rating agency.

Stockholder Protection Rights Agreement In June 2001, Xcel Energy adopted a Stockholder Protection Rights Agreement. Each share of Xcel

Energy’s common stock includes one shareholder protection right. Under the agreement’s principal provision, if any person or group acquires 15 percent

or more of Xcel Energy’s outstanding common stock, all other shareholders of Xcel Energy would be entitled to buy, for the exercise price of $95 per

right, common stock of Xcel Energy having a market value equal to twice the exercise price, thereby substantially diluting the acquiring person’s or

group’s investment. The rights may cause substantial dilution to a person or group that acquires 15 percent or more of Xcel Energy’s common stock.

The rights should not interfere with a transaction that is in the best interests of Xcel Energy and its shareholders because the rights can be redeemed

prior to a triggering event for $0.01 per right.

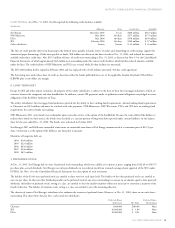

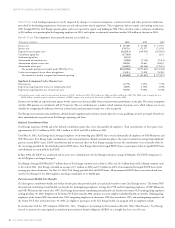

12. BENEFIT PLANS AND OTHER POSTRETIREMENT BENEFITS

Xcel Energy offers various benefit plans to its benefit employees. Approximately 51 percent of benefiting employees are represented by several local labor

unions under several collective-bargaining agreements. At Dec. 31, 2003, NSP-Minnesota had 2,244 and NSP-Wisconsin had 427 bargaining employees

covered under a collective-bargaining agreement, which expires at the end of 2004 but has been tentatively settled to extend until Dec. 31, 2007. PSCo

had 2,167 bargaining employees covered under a collective-bargaining agreement, which expires in May 2006. SPS had 739 bargaining employees

covered under a collective-bargaining agreement, which expires in October 2005.

Pension Benefits

Xcel Energy has several noncontributory, defined benefit pension plans that cover almost all employees. Benefits are based on a combination of years of

service, the employee’s average pay and Social Security benefits.

Xcel Energy’s policy is to fully fund into an external trust the actuarially determined pension costs recognized for ratemaking and financial reporting

purposes, subject to the limitations of applicable employee-benefit and tax laws.

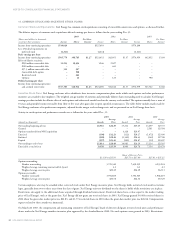

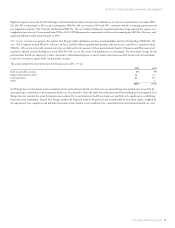

Pension Plan Assets Plan assets principally consist of the common stock of public companies, corporate bonds and U.S. government securities. The

target range for our pension asset allocation is 75 percent to 80 percent in equity investments, 5 percent to 10 percent in fixed income investments, no

cash investments and 10 percent to 15 percent in nontraditional investments, such as real estate, timber ventures, private equity and venture capital.

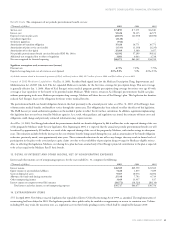

The actual composition of pension plan assets at Dec. 31 was:

2003 2002

Equity securities 75% 68%

Debt securities 14 16

Real estate 3–

Cash –4

Nontraditional investments 812

100% 100%

During 2003, Xcel Energy entered into a number of hedging arrangements within the pension trust designed to provide protection from a loss of asset

value in the event of a broad decline in equity prices. These arrangements are expected to expire at the end of 2004. At Dec. 31, 2003, the mark-to-market

value of these arrangements was not material to the value of pension trust assets.

Xcel Energy bases its investment-return assumption on expected long-term performance for each of the investment types included in its pension asset

portfolio. Xcel Energy considers the actual historical returns achieved by its asset portfolio over the past 20-year or longer period, as well as the long-term

return levels projected and recommended by investment experts. The historical weighted average annual return for the past 20 years for the Xcel Energy

portfolio of pension investments is 12.7 percent, which is in excess of the current assumption level. The pension cost determinations assume the continued

current mix of investment types over the long-term. The Xcel Energy portfolio is heavily weighted toward equity securities, includes nontraditional

investments that can provide a higher-than-average return, and in 2003 includes derivative financial instruments intended to hedge the risk of potentially