RBS 2006 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

RBS Group • Annual Report and Accounts 2006

90

Operating and financial review continued

Operating and financial review

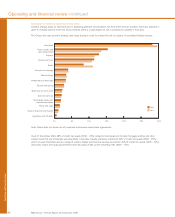

Short term wholesale deposits are taken from a wide range of

counterparties, with the largest single depositor continuing to

represent less than 1% of the Group’s total funding. The level

of funding from short term unsecured debt issuance and bank

deposits, excluding repos and short positions, has decreased

by £32.9 billion (25%) and now represents 13% of total funding

excluding other liabilities at 31 December 2006. This reflects

the increased use of secured and unsecured term issuance to

fund the higher rate of growth in customer loans and advances

(see ‘net customer activity’ below) and increased repo activity.

Short positions and repos with corporate, institutional customers

and banks are undertaken primarily by RBS Greenwich Capital

in the US and by Global Banking & Markets. Repos and short

positions increased by £50.1 billion (37%) to represent 26% of

total funding excluding other liabilities at 31 December 2006.

The Group remains well placed to access various wholesale

funding sources from a wide range of counterparties and

markets.

Net customer activity

Net customer lending, excluding repos, rose by £9.6 billion (as

the growth in loans and advances to customers continued to

exceed the growth in customer accounts, albeit to a lesser

degree than in previous years), thus increasing the degree of

reliance on wholesale market funding to support loan growth.

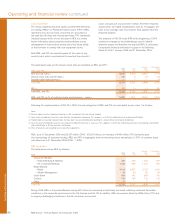

2006 2005 2004

Net customer activity £m £m £m

Loans and advances to customers (gross, excluding reverse repos) 407,918 372,223 299,235

Customer accounts (excluding repos) 320,238 294,113 241,181

Customer lending less customer accounts 87,680 78,110 58,054

Loans and advances to customers as a % of customer accounts (excluding repos) 127.4% 126.6% 124.1%

The Group evaluates on a regular basis its structural liquidity

risk and applies a variety of balance sheet management and

term funding strategies to maintain this risk within its normal

policy parameters.

Management of term structure

The degree of maturity mismatch within the overall long-term

structure of the Group’s assets and liabilities is managed

within internal policy guidelines, to ensure that term asset

commitments may be funded on an economic basis over their

life. In managing its overall term structure, the Group analyses

and takes into account the effect of retail and corporate

customer behaviour on actual asset and liability maturities

where they differ materially from the underlying contractual

maturities.

Stress testing

The maintenance of high quality credit ratings is recognised as

an important component in the management of the Group’s

liquidity risk. Credit ratings affect the Group’s ability to raise,

and the cost of raising, funds from the wholesale market and

the need to provide collateral in respect of, for example,

changes in the mark-to-market value of derivative transactions.

Given its strong credit ratings, the impact of a single notch

downgrade would, if it occurred, be expected to have a

relatively small impact on the Group’s economic access to

liquidity. More severe downgrades could have a progressively

greater impact but have an increasingly lower probability of

occurrence.

As part of its stress testing of its access to sufficient liquidity,

the Group regularly evaluates the potential impact of a range

of levels of downgrade in its credit ratings and carries out

stress tests of other relevant scenarios and sensitivity analyses.

Contingency funding plans are maintained to anticipate and

respond to any approaching or actual material deterioration in

market conditions or in the Group’s credit ratings, and the

Group remains confident of its ability to manage its liquidity

requirements effectively in all such circumstances.

Daily management

The primary focus of the Group’s daily management activity is

to ensure access to sufficient liquidity to meet its cashflow

obligations within key time horizons out to one month ahead.

The short-term maturity structure of the Group’s liabilities and

assets is managed on a daily basis to ensure that all material

cashflow obligations, and potential cashflows arising from

undrawn commitments and other contingent obligations, can

be met as they arise from day to day, either from cash inflows,

from maturing assets, new borrowing or the sale or repurchase

of various debt securities held (after allowing for appropriate

haircuts). Short-term liquidity risk is managed on a consolidated

basis for the whole Group including the Greenwich companies

but excluding the activities of Citizens and insurance

businesses, which are subject to regulatory regimes that

necessitate local management of liquidity.

Internal liquidity mismatch limits are set for all other

subsidiaries and non-UK branches which have material local

treasury activities in external markets, to ensure those activities

do not compromise daily maintenance of the Group’s overall

liquidity risk position within the Group’s policy parameters.

Citizens and the insurance companies have their own liquidity

policies which comply with their respective regulatory regimes.

The policies are also reviewed and monitored by Group Treasury.