RBS 2006 Annual Report Download - page 152

Download and view the complete annual report

Please find page 152 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

151

RBS Group • Annual Report and Accounts 2006

Financial statements

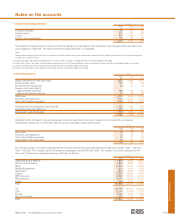

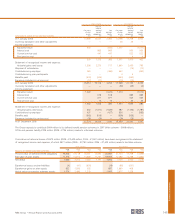

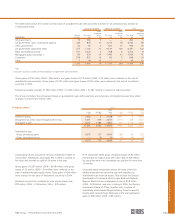

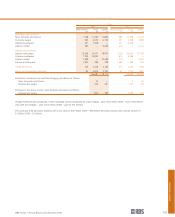

Key economic assumptions used in measuring the value of retained interests at the date of securitisation resulting from

securitisations completed during the year were as follows:

US Agency Consumer Commercial

retained retained retained

Assumptions interests interests interests

Prepayment speed 100 – 500 PSA 0 – 40% CPR (1) 0 – 50 CPY (2)

Weighted average life 2 – 18 years 0 – 13 years 1 – 10 years

Cash flow discount rate 0 – 20% 6 – 55% 5 – 9%

Credit losses N/A (3) 0 – 2% CDR (4) 0 – 2% CDR (4)

Key economic assumptions and the sensitivity of the current fair value of retained interests at 31 December 2006 to immediate

adverse changes, as indicated below, in those assumptions are as follows:

US Agency Consumer Commercial

retained retained retained

Assumptions/impact on fair value interests interests interests

Fair value of retained interests at 31 December 2006 (£m) 1,148 818 113

Prepayment speed(5) 10 – 32% CPR (1) 0 – 40% CPR (1) 0 – 100% CPY (2)

Impact on fair value of 10% adverse change (£m) 2.1 15.3 0.1

Impact on fair value of 20% adverse change (£m) 3.7 29.3 0.1

Weighted average life 1 – 18 years 0 – 13 years 1 – 18 years

Cash flow discount rate 0 – 20% 6 – 73% 5 – 9%

Impact on fair value of 10% adverse change (£m) 23.8 23.7 3.3

Impact on fair value of 20% adverse change (£m) 46.5 46.0 6.4

Credit losses N/A (3) 0 – 3% CDR (4) 0 – 2% CDR (4)

Impact on fair value of 10% adverse change (£m) N/A 36.2 0.1

Impact on fair value of 20% adverse change (£m) N/A 50.8 0.1

Notes:

(1) Constant prepayment rate (“CPR”) – the CPR range represents the low and high points of a dynamic CPR curve.

(2) CPR with yield maintenance provision and thus prepayment risk is limited.

(3) US Agency retained interests are securities whose principal and interest have been guaranteed by various United States government sponsored enterprises (‘GSEs’). These

GSEs include the Federal National Mortgage Association (‘Fannie Mae’), the Federal Home Loan Mortgage Corporation (‘Freddie Mac’), and the Government National Mortgage

Association (‘Ginnie Mae’). Fannie Mae and Freddie Mac are federally regulated but are privately owned. These GSEs guarantee that the holders of their mortgage-backed

securities will receive payments of interest and principal. Securities guaranteed by either of these two GSEs, although not formally rated, are regarded as having a credit rating

equivalent to AAA. Ginnie Mae guarantees the timely payment of principal and interest on all of its mortgage-backed securities, and its guarantee is backed by the full faith and

credit of the United States Government.

(4) Constant default rate.

(5) Prepayment speed has been stressed on an overall portfolio basis for US Agency retained interests due to the overall homogeneous nature of the collateral. Consumer and

commercial retained interests have been stressed on a security level basis.

The sensitivities depicted in the preceding table are

hypothetical and should be used with caution. The likelihood of

those percent variations selected for sensitivity testing is not

necessarily indicative of expected market movements because

the relationship of the change in the assumptions to the

change in fair value may not be linear. Also, the effect of a

variation in a particular assumption on the fair value of a

retained interest is calculated without changing any other

assumptions. This might not be the case in actual market

conditions since changes in one factor might result in changes

to other factors. Further, the sensitivities depicted above do not

consider any corrective actions that the Group might take to

mitigate the effect of any adverse changes in one or more key

assumptions.

Mortgage-backed securities

The Group sells originated mortgage loans to US government

sponsored enterprises in return for securities backed by these

loans and guaranteed by the Agency whilst retaining the rights

to service the mortgages. These securities may be

subsequently sold. The purchaser has recourse to the Group

for losses up to pre-determined levels on certain designated

mortgages. The Group is not obliged, and does not intend, to

support losses that may be suffered by the Agencies. Under

the terms of the sale agreements, the Agencies have agreed

to seek repayment only from the cash from the mortgage

loans. Once the securities exchanged for the loans have been

sold the Group’s exposure is restricted to the amount of the

recourse. At 31 December 2006 mortgages amounting to

£144 million (2005 – £385 million) had been sold with recourse

to US GSEs. These loans have been derecognised.