Progressive 2004 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2004 Progressive annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

|

|

APP.-B-8

Loss and Loss Adjustment Expense Reserves Loss reserves represent the estimated liability on claims reported to the Company, plus

reserves for losses incurred but not recorded (IBNR). These estimates are reported net of amounts recoverable from salvage and subrogation.

Loss adjustment expense reserves represent the estimated expenses required to settle these claims and losses. The methods of making

estimates and establishing these reserves are reviewed regularly, and resulting adjustments are reflected in income currently. Such loss

and loss adjustment expense reserves could be susceptible to significant change in the near term.

Reinsurance The Company’s reinsurance transactions include premiums written under state-mandated involuntary plans for commercial

vehicles (Commercial Auto Insurance Procedures/Plans- “CAIP”), for which the Company retains no loss indemnity risk (see

Note 6 —

Reinsurance

for further discussion). In addition, the Company cedes auto premiums to state-provided reinsurance facilities. The Company

also cedes premiums in its non-auto programs to limit its exposure in those particular markets. Beginning in 2004, prepaid reinsurance

premiums are being earned on a pro rata basis over the period of risk, based on a daily earnings convention, which is consistent with

premiums written. Prior to 2004, prepaid reinsurance premiums were recognized primarily using a mid-month convention, which was

consistent with premiums written. Because the Company’s primary line of business, auto insurance, is written at relatively low limits of

liability, the Company does not believe that it needs to mitigate its risk through voluntary reinsurance.

Earnings Per Share Basic earnings per share are computed using the weighted average number of Common Shares outstanding. Diluted

earnings per share include common stock equivalents assumed outstanding during the period. The Company’s common stock equivalents

include stock options and qualified restricted stock awards.

Deferred Acquisition Costs Deferred acquisition costs include commissions, premium taxes and other variable underwriting and direct

sales costs incurred in connection with writing business. These costs are deferred and amortized over the policy period in which the related

premiums are earned. The Company considers anticipated investment income in determining the recoverability of these costs. Management

believes that these costs will be fully recoverable in the near term. The Company does not defer advertising costs.

Guaranty Fund Assessments The Company is subject to state guaranty fund assessments which provide for the payment of covered

claims or other insurance obligations of insurance companies deemed insolvent. These assessments are accrued after a formal determination

of insolvency has occurred and the Company has written the premiums on which the assessments will be based.

Service Revenues and Expenses Service revenues consist primarily of fees generated from processing business for involuntary plans and

are earned on a pro rata basis over the term of the related policies. Acquisition expenses are deferred and amortized over the period in

which the related revenues are earned.

Stock Compensation The Company follows the provisions of Statement of Financial Accounting Standards (SFAS) 123, “Accounting for

Stock-Based Compensation,” to account for its stock compensation activity in the financial statements. Prior to January 1, 2003, the

Company followed the provisions of Accounting Principles Board (APB) Opinion No. 25, “Accounting for Stock Issued to Employees,” to

account for its stock option activity.

The change to the fair value method of accounting under SFAS 123 was applied prospectively to all non-qualified stock option awards

granted, modified, or settled after January 1, 2003. No stock options were granted after December 31, 2002. As a result, there is no

compensation cost for stock options included in net income for 2003 or 2004; however, compensation expense would have been recognized

if the fair value method had been used for all awards since the original effective date of SFAS 123 (January 1, 1995). Prior to 2003, the

Company granted all options currently outstanding at an exercise price equal to the market price of the Company’s Common Shares at the

date of grant and, therefore, under APB 25, no compensation expense was recorded.

In 2003, the Company began issuing restricted stock awards. Compensation expense for restricted stock awards is recognized over the

respective vesting periods. The current year expense is not representative of the effect on net income for future years since each subsequent

year will reflect expense for additional awards.

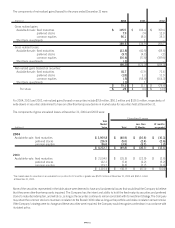

The following table shows the effects on net income and earnings per share had the fair value method been applied to all outstanding

and unvested stock option awards for the periods presented. The Company used the modified Black-Scholes pricing model to calculate the

fair value of the options awarded as of the date of grant.