BP 2011 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2011 BP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

BP Annual Report and Form 20-F 2011 103

Business review: BP in more depth

Business review

Liquidity and capital resources

Following the Deepwater Horizon oil spill in 2010, the group initially faced

significant costs relating to the immediate response activities as well as

significant uncertainty regarding the ultimate magnitude of its liabilities and

timing of cash outflows. During 2011 the impact on the group’s liquidity

and capital resources has stabilized, allowing steps to be taken to enhance

the strength of the balance sheet.

The group’s long-term credit ratings are A (stable outlook) from

Standard & Poor’s, strengthened from A (negative outlook) in July 2011,

and A2 (stable outlook) from Moody’s Investor Services.

BP renegotiated its committed bank facilities during 2011 putting in

place $6.9 billion of facilities with 25 international banking counterparties,

mostly for a term of three years. In addition the group has increased

its access to commercial bank letters of credit (LC) by putting in place

committed LC facilities of $5.1 billion and secured LC arrangements of $2.2

billion, to supplement its uncommitted and unsecured LC lines.

The disposal programme of $30 billion initially announced in 2010

has been increased to $38 billion, for completion by the end of 2013. By

the end of 2011 agreements had been signed for more than $21 billion,

with cash receipts totalling $17 billion in 2010 and $2.7 billion in 2011.

BP accessed US and European capital markets throughout the year

with bond issuances amounting to $10.7 billion in 2011.

A further $0.8 billion of US Industrial Revenue/Municipal bonds

were re-issued in term-out mode of between three to 10 years during

the year.

During 2011 BP repaid $2.9 billion of the $5.3 billion of borrowings

raised in 2010 that were secured against working capital and other assets,

or backed by future crude oil sales from BP’s interests in specific offshore

Angola and Azerbaijan fields.

Financial framework

BP continues to refine its financial framework to support the pursuit of

value growth for shareholders, while maintaining a secure financial base.

BP intends to increase operating cash flowa by 50% in 2014 compared to

2011b. Half of the increase will arise as the remaining payments into the

Deepwater Horizon Oil Spill Trust fund complete by the end of 2012, and

half from operations. BP plans to use half of the expected additional cash

flows to increase investments and half for other purposes.

We intend to maintain a significant liquidity buffer and to reduce our

net debt ratio to the lower half of the 10-20% gearing range over time. See

Financial statements – Note 35 on page 230 for gross debt, which is the

nearest equivalent measure to net debt on an IFRS basis, and for further

information on net debt and net debt ratio.

a Operating cash flow is net cash provided by (used in) operating activities, as stated in the group

cash flow statement on page 181.

b Assuming an oil price of $100 per barrel in 2014. The projection reflects our expectation that all

required payments into the $20-billion trust fund will have been completed by the end of 2012.

It does not reflect any cash flows relating to other liabilities, contingent liabilities, settlements or

contingent assets arising from the Gulf of Mexico oil spill which may or may not arise at that time.

See Financial statements – Note 43 on page 249, for further information on contingent liabilities.

Dividends and other distributions to shareholders

On 1 February 2011, BP announced the resumption of quarterly dividend

payments, with a fourth-quarter 2010 dividend of 7 cents per share. The

resumption followed the suspension of dividend payments for the first

three quarters of 2010 announced in June 2010 in light of the Deepwater

Horizon oil spill and commitments to fund the $20-billion Trust. The same

level of dividend was maintained for the first three quarters of 2011.

The total dividend paid to BP shareholders in 2011 was $4.1 billion

with shareholders also having the option to receive a scrip dividend,

compared with $2.6 billion paid in 2010. The dividend is determined in US

dollars, the economic currency of BP.

On 7 February 2012, BP announced a dividend of 8 cents per share

in respect of the fourth quarter 2011.

During 2011 and 2010, the company did not repurchase any of

its own shares. Details of purchases to satisfy requirements of certain

employee share-based payment plans are set out on page 170.

Financing the group’s activities

The group’s principal commodity, oil, is priced internationally in US dollars.

Group policy has generally been to minimize economic exposure to

currency movements by financing operations with US dollar debt. Where

debt is issued in other currencies, including euros, it is generally swapped

back to US dollars using derivative contracts, or else hedged by maintaining

offsetting cash positions in the same currency. The overall cash balances

of the group are mainly held in US dollars or swapped to US dollars and

holdings are well-diversified to reduce concentration risk. The group is not

therefore exposed to significant currency risk, such as in relation to the

euro, regarding its borrowings. Also see Risk factors on page 59 for further

information on risks associated with the general macroeconomic outlook,

including the stability of the eurozone and Financial statements – Note 26

on page 217.

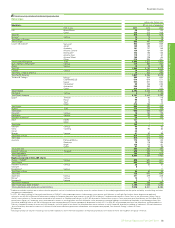

The group’s finance debt at 31 December 2011 amounted to $44.2

billion (2010 $45.3 billion). Of the total finance debt, $9.0 billion is classified

as short term at the end of 2011 (2010 $14.6 billion). The short-term

balance includes $4.9 billion for amounts repayable within the next 12

months relating to long-term borrowings (2010 $6.9 billion). Commercial

paper markets in the US and Europe are a further source of short-term

liquidity for the group to provide timing flexibility. At 31 December 2011,

outstanding commercial paper amounted to $3.6 billion (2010 $1.0 billion).

Also included within short-term debt at the end of 2010 was $6.2 billion

relating to deposits received for announced disposal transactions still

pending legal completion post the balance sheet date. At the end of 2011

the balance was de minimis at $30 million.

We have in place a European Debt Issuance Programme (DIP)

under which the group may raise up to $20 billion of debt for maturities

of one month or longer. At 31 December 2011, the amount drawn down

against the DIP was $11.6 billion (2010 $12.3 billion). In addition, the group

has in place an unlimited US shelf registration statement under which it

may raise debt with maturities of one month or longer. None of the capital

market bond issuances since the Deepwater Horizon oil spill contain any

additional financial covenants compared with the group’s capital markets

issuances prior to the incident.

The maturity profile and fixed/floating rate characteristics of the

group’s debt are described in Financial statements – Note 34 on page 229.

Net debt was $29.0 billion at the end of 2011, an increase of $3.1

billion from the 2010 year-end position of $25.9 billion. The ratio of net

debt to net debt plus equity was 20.5% at the end of 2011 (2010 21.2%).

Net debt and the ratio of net debt to net debt plus equity are non-GAAP

measures. We believe that these measures provide useful information to

investors. Net debt enables investors to see the economic effect of gross

debt, related hedges and cash and cash equivalents in total. The net debt

ratio enables investors to see how significant net debt is relative to equity

from shareholders. See Financial statements – Note 35 on page 230 for

gross debt, which is the nearest equivalent measure on an IFRS basis, and

for further information on net debt.

Included in net debt are cash and cash equivalents of $14.1 billion

at 31 December 2011 (2010 $18.6 billion). BP manages its cash position

to ensure the group has adequate cover to respond to potential short-term

market illiquidity, and expects to maintain a strong cash position. Cash

balances are pooled centrally where permissible, and deployed globally

as required. Cash surpluses are deposited with creditworthy banks and

money market funds with short maturities to ensure availability. The

group holds $1.2 billion of cash outside the UK and it is not expected

that any significant tax will arise on repatriation. Further information on

the management of liquidity risk and credit risk is provided in Financial

statements – Note 26 on pages 217-222, and on the cash position in

Financial statements – Note 30 on page 223.

The group also has access to significant sources of liquidity in the

form of committed bank facilities. At 31 December 2011, the group had

available undrawn committed standby borrowing facilities of $6.9 billion

(2010 $12.5 billion), made up of:

• $6.8 billion of standby facilities available to draw and repay by mid-March

2014.

• 625 million Chinese yuan ($0.1 billion) of 365-day standby facilities

available to draw and repay until the second half of 2012.

During 2011 $7.2 billion of 364-day facilities expired and were not renewed.