Thrifty Car Rental 2007 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2007 Thrifty Car Rental annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

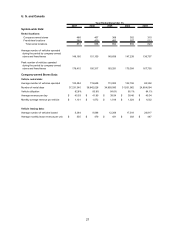

¾ Separation costs relating to the elimination of certain positions from the organizational structure

were $2.4 million.

¾ The market value of investments in the Company’s deferred compensation and retirement plans

increased $2.1 million, which is offset in other revenue and, therefore, did not impact net income.

¾ Personnel related expenses decreased $1.1 million due primarily to lower personnel costs of

approximately $6.2 million, which was primarily related to IT employees outsourced in October

2006 and a $1.5 million reduction in group health insurance. These reductions in personnel

related costs were partially offset by a $6.6 million increase in performance share expense. The

increase in performance share expense included $2.2 million related to a change in estimate for

the final calculation of the vested 2003 performance share awards paid in 2006, $2.9 million for

higher costs related to the 2006 performance share awards and $1.5 million to reflect current

performance estimates.

Net interest expense increased $7.8 million in 2006 primarily due to higher average vehicle debt and

higher interest rates, partially offset by higher interest rates on cash invested and to an increase in the

rate received on interest reimbursements relating to vehicle programs. As a percent of revenue, net

interest expense was 5.8% in 2006 and 2005.

The change in fair value of the Company’s interest rate swap agreements was a decrease of $9.4 million

in 2006 compared to an increase of ($29.7) million in 2005 resulting in a year over year decrease of $39.1

million.

The income tax provision for 2006 was $36.7 million. The effective income tax rate was 41.5% for 2006

and 2005. The Company reports taxable income for the U.S. and Canada in separate tax jurisdictions

and establishes provisions separately for each jurisdiction. On a separate, domestic basis, the U.S.

effective tax rate approximates the statutory tax rate including the effect of state income taxes. However,

no income tax benefit was recorded for Canadian losses in 2006 or 2005, thus, increasing the

consolidated effective tax rate compared to the U.S. effective tax rate.

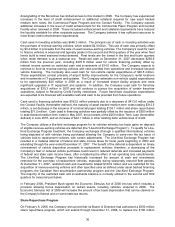

Liquidity and Capital Resources

The Company’s primary uses of liquidity are for the purchase of vehicles for its rental and leasing fleets,

non-vehicle capital expenditures, franchisee acquisitions and for working capital. The Company uses

both cash and letters of credit to support asset backed vehicle financing programs. The Company also

uses letters of credit or insurance bonds to secure certain commitments related to airport concession

agreements, insurance programs, and for other purposes.

The Company’s primary sources of liquidity are cash generated from operations, secured vehicle

financing, the Senior Secured Credit Facilities and insurance bonds. Cash generated by operating

activities of $537.3 million for 2007 is primarily the result of net income, adjusted for depreciation and the

change in fair value of derivatives. The liquidity necessary for purchasing vehicles is primarily obtained

from secured vehicle financing, most of which is proceeds from sale of asset backed medium term notes

and asset backed commercial paper programs, sales proceeds from disposal of used vehicles and cash

generated by operating activities. The asset backed medium term notes and commercial paper programs

require varying levels of credit enhancement or overcollateralization, which are provided by a combination

of cash, vehicles, letters of credit and proceeds from the Term Loan. These letters of credit are provided

under the Company’s Revolving Credit Facility.

The Company believes that its cash generated from operations, availability under its Revolving Credit

Facility, insurance bonding programs, proceeds from its Term Loan and secured vehicle financing

programs are adequate to meet its liquidity requirements for the foreseeable future. A significant portion

of the secured vehicle financing is available through the asset backed commercial paper programs and

bank facilities, which are 364-day commitments that are renewable annually. The successful annual

renewal of these facilities along with the Company’s existing asset backed medium term notes and other

secured vehicle financing facilities are expected to be sufficient to meet 2008 vehicle financing

requirements. The asset backed medium term notes have varying maturities through 2012. The

Company generally issues additional asset backed medium term notes each year to increase or replace

maturing vehicle financing capacity. Recent volatility in the credit markets and the downgrading or risk of

35