Red Lobster 2013 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2013 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74

|

|

Notes to Consolidated Financial Statements

Darden

64 Darden Restaurants, Inc. 2013 Annual Report

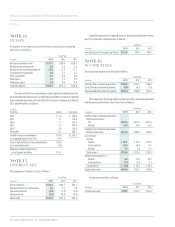

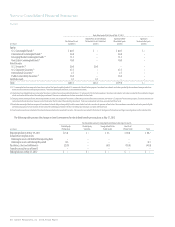

All performance stock units outstanding as of May 26, 2013 will be settled in

cash upon vesting. As of May 26, 2013, our total performance stock unit liability

was $16.8 million, including $9.0 million recorded in other current liabilities and

$7.8 million recorded in other liabilities on our consolidated balance sheets. As

of May 27, 2012, our total performance stock unit liability was $31.3 million,

including $18.9 million recorded in other current liabilities and $12.4 million

recorded in other liabilities on our consolidated balance sheets.

Performance stock units cliff vest 3 years from the date of grant, where

0.0 percent to 150.0 percent of the entire grant is earned or forfeited at the end

of 3 years. The number of units that actually vests will be determined for each

year based on the achievement of Company performance criteria set forth in the

award agreement and may range from 0.0 percent to 150.0 percent of the annual

target. All awards will be settled in cash. The awards are measured based on the

market price of our common stock each period, are amortized over the service

period and the vested portion is carried as a liability in our accompanying consoli-

dated balance sheets. As of May 26, 2013, there was $11.1 million of unrecognized

compensation cost related to unvested performance stock units granted under

our stock plans. This cost is expected to be recognized over a weighted-average

period of 1.7 years. The total fair value of performance stock units that vested in

fiscal 2013 was $21.5 million.

We maintain an Employee Stock Purchase Plan to provide eligible employees

who have completed one year of service (excluding senior officers subject to

Section 16(b) of the Securities Exchange Act of 1934, and certain other employees

who are employed less than full time or own 5 percent or more of our capital stock

or that of any subsidiary) an opportunity to invest up to $5.0 thousand per calendar

quarter to purchase shares of our common stock, subject to certain limitations.

Under the plan, up to an aggregate of 3.6 million shares are available for purchase

by employees at a purchase price that is 85.0 percent of the fair market value of

our common stock on either the first or last trading day of each calendar quarter,

whichever is lower. Cash received from employees pursuant to the plan during fiscal

2013, 2012 and 2011 was $7.3 million, $7.2 million and $7.4 million, respectively.

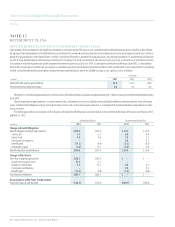

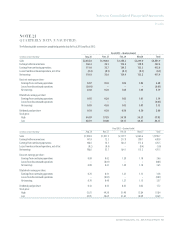

NOTE 19

COMMITMENTS AND

CONTINGENCIES

As collateral for performance on contracts and as credit guarantees to banks

and insurers, we were contingently liable for guarantees of subsidiary obliga-

tions under standby letters of credit. At May 26, 2013 and May 27, 2012, we had

$107.0 million and $99.2 million, respectively, of standby letters of credit related

to workers’ compensation and general liabilities accrued in our consolidated

financial statements. At May 26, 2013 and May 27, 2012, we had $20.6 million

and $20.3 million, respectively, of standby letters of credit related to contractual

operating lease obligations and other payments. All standby letters of credit are

renewable annually.

At May 26, 2013 and May 27, 2012, we had $4.2 million and $5.4 million,

respectively, of guarantees associated with leased properties that have been

assigned to third parties. These amounts represent the maximum potential amount

of future payments under the guarantees. The fair value of these potential payments

discounted at our pre-tax cost of capital at May 26, 2013 and May 27, 2012,

amounted to $3.4 million and $4.1 million, respectively. We did not accrue for the

guarantees, as the likelihood of the third parties defaulting on the assignment

agreements was deemed to be less than probable. In the event of default by a

third party, the indemnity and default clauses in our assignment agreements

govern our ability to recover from and pursue the third party for damages incurred

as a result of its default. We do not hold any third-party assets as collateral related

to these assignment agreements, except to the extent that the assignment

allows us to repossess the building and personal property. These guarantees

expire over their respective lease terms, which range from fiscal 2015 through

fiscal 2021.

We are subject to private lawsuits, administrative proceedings and claims

that arise in the ordinary course of our business. A number of these lawsuits,

proceedings and claims may exist at any given time. These matters typically

involve claims from guests, employees and others related to operational issues

common to the restaurant industry, and can also involve infringement of, or

challenges to, our trademarks. While the resolution of a lawsuit, proceeding or

claim may have an impact on our financial results for the period in which it is

resolved, we believe that the final disposition of the lawsuits, proceedings and

claims in which we are currently involved, either individually or in the aggregate,

will not have a material adverse effect on our financial position, results of opera-

tions or liquidity. The following is a brief description of the more significant of

these matters.

In September 2012, a collective action under the Fair Labor Standards Act

was filed in the United States District Court for the Southern District of Florida,

Alequin v. Darden Restaurants, Inc., in which named plaintiffs claim that the

Company required or allowed certain employees at Olive Garden, Red Lobster,

LongHorn Steakhouse, Bahama Breeze and Seasons 52 to work off the clock and

required them to perform tasks unrelated to their tipped duties while taking a

tip credit against their hourly rate of pay. The plaintiffs seek an unspecified

amount of alleged back wages, liquidated damages, and attorneys’ fees. In July

2013, the District Court conditionally certified a nationwide class of servers and

bartenders who worked in the aforementioned restaurants at any point from

September 6, 2009 through September 6, 2012. Unlike a class action, a collective

action requires potential class members to “opt in” rather than “opt out,” and

members of the class will have 90 days to opt in following the issuance of a notice.

The Company will have an opportunity to seek to have the class de-certified

and/or seek to have the case dismissed on its merits. We believe that our wage

and hour policies comply with the law and that we have meritorious defenses to

the substantive claims and strong defenses supporting de-certification. An esti-

mate of the possible loss, if any, or the range of loss cannot be made at this stage

of the proceeding.

NOTE 20

SUBSEQUENT EVENT

On June 19, 2013, the Board of Directors declared a cash dividend of $0.55 per

share to be paid August 1, 2013 to all shareholders of record as of the close of

business on July 10, 2013.