Red Lobster 2013 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2013 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

Darden

Darden Restaurants, Inc. 2013 Annual Report 21

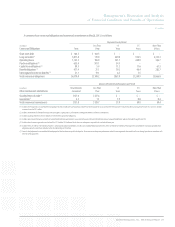

improved wage-rate management and lower manager incentive compensation,

partially offset by an increase in FICA taxes on higher reported tips. The increase in

FICA tax expense on higher reported tips is fully offset in our consolidated earnings

from continuing operations by a corresponding income tax credit, which reduces

income tax expense. Manager incentive compensation paid out at approximately

65.0 percent of the targeted amount in fiscal 2013, as compared to 84.0 percent

and 93.0 percent in fiscal 2012 and 2011, respectively.

Restaurant expenses (which include utilities, repairs and maintenance, credit

card, lease, property tax, workers’ compensation, new restaurant pre-opening and

other restaurant-level operating expenses) increased $133.8 million, or 11.1 percent,

from $1.20 billion in fiscal 2012 to $1.33 billion in fiscal 2013. Restaurant expenses

increased $71.6 million, or 6.3 percent, from $1.13 billion in fiscal 2011 to

$1.20 billion in fiscal 2012. As a percent of sales, restaurant expenses increased

in fiscal 2013 as compared to fiscal 2012 primarily as a result of Yard House’s higher

restaurant expenses as a percentage of sales compared to our consolidated average

prior to the acquisition. Additionally, restaurant expenses as a percentage of sales

increased due to lost sales leverage, partially offset by lower utilities expenses.

As a percent of sales, restaurant expenses decreased in fiscal 2012 as compared

to fiscal 2011 primarily due to sales leveraging and lower credit card fees partially

offset by higher workers’ compensation costs.

Selling, general and administrative expenses increased $101.0 million, or

13.5 percent, from $746.8 million in fiscal 2012 to $847.8 million in fiscal 2013.

Selling, general and administrative expenses increased $4.1 million, or 0.6 percent,

from $742.7 million in fiscal 2011 to $746.8 million in fiscal 2012. As a percent of

sales, selling, general and administrative expenses increased from fiscal 2012 to

fiscal 2013 primarily due to higher media costs and acquisition and integration

costs associated with the Yard House acquisition, partially offset by sales leverage

and lower performance-based compensation. As a percent of sales, selling,

general and administrative expenses decreased from fiscal 2011 to fiscal 2012

primarily due to sales leveraging, lower performance incentive compensation

and favorable market-driven changes in fair value related to our non-qualified

deferred compensation plans, partially offset by higher media costs.

Depreciation and amortization expense increased $45.7 million, or 13.1 percent,

from $349.1 million in fiscal 2012 to $394.8 million in fiscal 2013. Depreciation and

amortization expense increased $32.3 million, or 10.2 percent, from $316.8 million

in fiscal 2011 to $349.1 million in fiscal 2012. As a percent of sales, depreciation

and amortization expense increased in fiscal 2013 primarily due to an increase in

depreciable assets related to new restaurants and remodel activities. As a percent

of sales, depreciation and amortization expense increased in fiscal 2012 primarily

due to an increase in depreciable assets related to new restaurants and remodel

activities, partially offset by sales leveraging.

Net interest expense increased $24.3 million, or 23.9 percent, from

$101.6 million in fiscal 2012 to $125.9 million in fiscal 2013. Net interest expense

increased $8.0 million, or 8.5 percent, from $93.6 million in fiscal 2011 to

$101.6 million in fiscal 2012. As a percent of sales, net interest expense increased

in fiscal 2013 compared to fiscal 2012 due to higher average debt balances in fiscal

2013 principally driven by the acquisition of Yard House. As a percent of sales, net

interest expense increased in fiscal 2012 compared to fiscal 2011 due to higher

average debt balances in fiscal 2012, partially offset by sales leveraging.

INCOME TAXES

The effective income tax rates for fiscal 2013, 2012 and 2011 continuing operations

were 21.0 percent, 25.3 percent and 26.1 percent, respectively. The decrease in our

effective rate for fiscal 2013 is primarily attributable to an increase in the impact

of FICA tax credits for employee reported tips due to a decrease in our earnings

before income taxes and the impact of market-driven changes in the value of our

trust-owned life insurance that are excluded for tax purposes, partially offset by a

decrease in federal income tax credits related to the HIRE Act. The decrease in our

effective rate for fiscal 2012 is primarily attributable to an increase in federal income

tax credits related to the HIRE Act, an increase in the impact of FICA tax credits for

employee reported tips, partially offset by the impact of market-driven changes

in the value of our trust-owned life insurance that are excluded for tax purposes.

NET EARNINGS AND NET EARNINGS PER SHARE

FROM CONTINUING OPERATIONS

Net earnings from continuing operations for fiscal 2013 were $412.6 million

($3.14 per diluted share) compared with net earnings from continuing operations

for fiscal 2012 of $476.5 million ($3.58 per diluted share) and net earnings from

continuing operations for fiscal 2011 of $478.7 million ($3.41 per diluted share).

Net earnings from continuing operations for fiscal 2013 decreased 13.4 percent

and diluted net earnings per share from continuing operations decreased 12.3 per-

cent compared with fiscal 2012, primarily due to higher selling, general and

administrative expenses, restaurant expenses, depreciation and amortization

expenses and net interest expense as a percent of sales, partially offset by increased

sales and a lower effective income tax rate. Costs associated with the Yard House

acquisition adversely affected diluted net earnings per share from continuing

operations by approximately $0.09.

Net earnings from continuing operations for fiscal 2012 decreased 0.5 percent

and diluted net earnings per share from continuing operations increased 5.0 percent

compared with fiscal 2011. The decrease in net earnings from continuing opera-

tions was primarily due to higher food and beverage costs and depreciation and

amortization expense as a percent of sales, which were partially offset by increased

sales, lower restaurant labor expenses, and selling, general and administrative

expenses as a percent of sales, and a lower effective income tax rate. While net

earnings from continuing operations decreased, diluted net earnings per share

from continuing operations increased for fiscal 2012 due to a reduction in the

average diluted shares outstanding primarily as a result of the cumulative impact

of our continuing repurchase of our common stock.

LOSSES FROM DISCONTINUED OPERATIONS

On an after-tax basis, losses from discontinued operations for fiscal 2013 were

$0.7 million ($0.01 per diluted share) compared with losses from discontinued

operations for fiscal 2012 of $1.0 million ($0.01 per diluted share) and fiscal 2011

of $2.4 million ($0.02 per diluted share).