Qantas 2006 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2006 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148

|

|

137

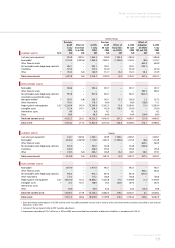

Qantas Annual Report 2006

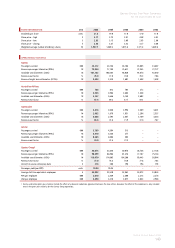

Notes to the Financial Statements

for the year ended 30 June 2006

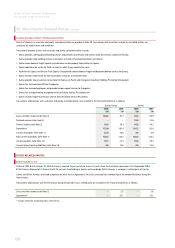

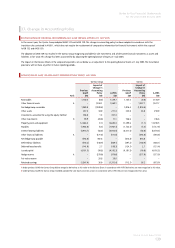

Other Leases

A-IFRS requires the lease expense to be recognised on a straight-line basis.

An A-IFRS transition adjustment is therefore required for leases with a pre-

determined rent escalation.

At the date of transition, an increase in payables of $9.2 million and

consequential decrease in retained earnings of $6.4 million is recognised

after a tax benefit of $2.8 million.

Applying A-IFRS to other leases for the year ended 30 June 2005 results

in a $11.7 million increase in profit before related income tax expense.

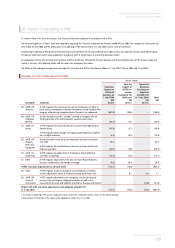

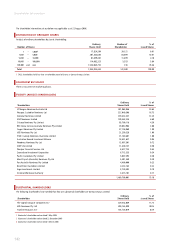

(D) PROPERTY, PLANT AND EQUIPMENT

Under both previous GAAP and A-IFRS, items of property, plant and

equipment are initially recorded at their cost of acquisition at the date of

acquisition, being the fair value of the consideration provided plus

incidental costs directly attributable to the acquisition. Major modifications

to aircraft and the costs associated with placing the aircraft into service are

capitalised as part of the cost of the asset to which they relate.

Transition Exemption

As permitted by AASB 1 – First-time Adoption of A-IFRS, Qantas has elected

to deem the cost of land and buildings under A-IFRS to be the carrying

value at the date of transition. At the date of transition, a decrease in the

asset revaluation reserve of $55.5 million (Qantas: $82.9 million) is

recognised with a consequential increase in retained earnings of $55.5

million (Qantas: $82.9 million).

Major Inspections

Under previous GAAP, all aircraft maintenance and inspection costs were

expensed as incurred. Under A-IFRS, the cost of major inspections of

airframes and engines is capitalised and depreciated over the scheduled

usage period to the next major inspection event. All other aircraft

maintenance costs were expensed as incurred.

At the date of transition, a decrease in property, plant and equipment of

$57.5 million with a consequential decrease in retained earnings of $40.3

million is recognised after a tax benefit of $17.2 million.

Applying A-IFRS to aircraft inspection costs for the year ended 30 June 2005

results in a $8.7 million increase in aircraft depreciation and operating costs.

Software Development Costs

Under A-IFRS, software development costs that meet the criteria to be

recognised as internally generated intangible assets are capitalised.

At the date of transition, a decrease in property, plant and equipment of

$141.8 million (Qantas: $141.8 million) and an increase in intangible assets

of $141.8 million (Qantas: $141.8 million) is recognised increasing to

$160.0 million (Qantas: $160.0 million) at 30 June 2005. There is no effect

on retained earnings.

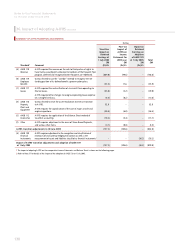

(E) INCOME TAXES

On transition to A-IFRS, the balance sheet method of tax effect accounting

was adopted, rather than the ‘profit and loss’ method previously applied

under previous GAAP. Under the balance sheet approach, income tax on

the profit and loss for the year comprises both current and deferred taxes.

Broadly, temporary differences were differences between the carrying

amount of assets and liabilities for financial reporting purposes and the

amount attributed to those assets and liabilities for taxation purposes.

Temporary differences may give rise to deferred tax assets or deferred

tax liabilities.

A deferred tax liability is required to be recognised, subject to some

exceptions. A deferred tax asset shall be recognised only to the extent that

it is probable that future taxable profits will be available against which the

deductible temporary difference can be utilised, subject to some exceptions.

At the date of transition, excluding the tax effect of adjustments generated

by the adoption of other A-IFRS standards, applying A-IFRS results in an

increase in deferred tax liabilities of $2.1 million and an increase in capital

of $8.2 million. These were recognised after a decrease in retained earnings

of $10.3 million.