Porsche 2012 Annual Report Download - page 185

Download and view the complete annual report

Please find page 185 of the 2012 Porsche annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

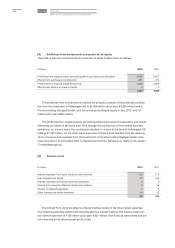

|

|

Provisions are not offset against reimbursement claims from third parties. Reimbursement

claims are recognized separately in other assets if it is virtually certain that the Porsche SE

group will receive the reimbursement when it settles the obligation.

Accruals are not presented under provisions, but under trade payables or other liabilities,

depending on their nature.

Liabilities

Non-current liabilities are recognized at amortized cost. Differences between their historical cost

and their repayment amount are accounted for using the effective interest method. Current liabil-

ities are recognized at their repayment or settlement value.

Revenue and expenses

Revenue is generally recognized to the extent that it is probable that the economic benefits will

flow to the group and the revenue can be reliably measured.

Revenue from the sale of products is generally not recognized until the point in time when

the significant opportunities and risks associated with ownership of the goods and products

being sold are transferred to the buyer. Revenue is reported net of discounts, customer bonuses

and rebates.

Income from assets for which a group entity has a buyback obligation cannot be realized

until the assets have definitely left the group. If a fixed repurchase price was agreed when the

contract was concluded, the difference between the selling and repurchase price is recognized

as income ratably over the term of the contract. Prior to that time, the assets are accounted for

as inventories.

Revenue from receivables from financial services is realized using the effective interest

method.

Revenue is generally recorded separately for each business transaction. If two or more

transactions are linked in such a way that the commercial effect cannot be understood without

reference to the series of transactions as a whole, the criteria for revenue recognition are applied

to these transactions as a whole. If, for example, loans in the financial services sector are issued

at below market interest rates to promote sales of new vehicles, revenue is reduced by the in-

centive arising from the loan.

Revenue from long-term development contracts is recognized in accordance with the per-

centage of completion method.

181