Porsche 2011 Annual Report Download - page 173

Download and view the complete annual report

Please find page 173 of the 2011 Porsche annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

Amendments to IAS 19 “Employee Benefits”

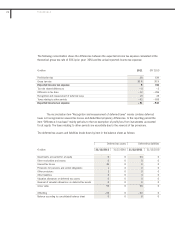

The amendments concern

· the elimination of the deferred recording of actuarial gains and losses (corridor method); in future actuarial

gains and losses must be recognized in other comprehensive income

· the presentation/allocation of changes in the net liabilities/assets from defined benefit plans

· additional disclosures on characteristics of and risks relating to such defined benefit plans

The amended IAS 19 is mandatory for fiscal years beginning on or after 1 January 2013. In connection

with the elimination of what is referred to as the corridor method, pension provisions have to be reduced or

increased by an amount equivalent to the unrecognized actuarial gains or losses and a corresponding counter-

adjustment has to be made in equity. The effects on pension provisions reported in the consolidated financial

statements of Porsche SE will be immaterial. In addition, this will give rise to effects on Porsche SE’s

accounting for its investments in Volkswagen AG and Porsche Zwischenholding GmbH at equity and on Porsche

SE’s group equity. These quantitative effects are still being analyzed.

Amendments to IFRS 9 “Financial Instruments” and IFRS 7 “Financial Instruments: Disclosures”

The IASB published an amendment to IFRS 9 “Financial Instruments”. This encompasses additions to

IFRS 7 “Financial Instruments”. It prescribes that IFRS 9 is not mandatory until fiscal years beginning on or after

1 January 2015. Earlier adoption is permitted.

Amendments to IAS 32 “Financial Instruments” and IFRS 7 “Financial Instruments: Disclosures”

The IASB published amendments to IAS 32 and IFRS 7. With these amendments the IASB clarifies

some details relating to the netting of financial assets against financial liabilities and requires additional

disclosures. The IASB does not intend this to alter the existing netting principle in IAS 32. The clarification of

the criteria “simultaneous settlement” and “legally enforceable right to set off the amounts” can only result in a

change in the accounting treatment if IAS 32 had been interpreted differently thus far. As a supplementary

mandatory disclosure, the gross and net amounts from offsetting as well as amounts related to existing

offsetting rights that do not satisfy the criteria for offsetting in the balance sheet will in future have to be

presented in a table. These amendments are applicable respectively for fiscal years beginning on and after

1 January 2013 (additional disclosures) or 2014 (clarifications).

In addition, the consolidated financial statements for SFY 2010 already presented amendments that

have still not been applied in the fiscal year 2011. Porsche SE will analyze the impact of the new standards and

the amendments on the presentation of its net assets, financial position and results of operations as well as the

cash flows.

Voluntary early adoption of the changes before they become mandatory under the transitional

provisions of IASB is not planned.

173

3