Google 2014 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2014 Google annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

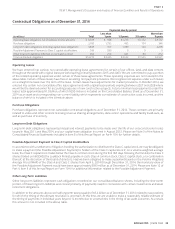

O-Balance Sheet Arrangements

is material to investors.

Critical Accounting Policies and Estimates

policies and estimates. In some cases, changes in the accounting estimates are reasonably likely to occur from period to period.

experience and other assumptions that we believe are reasonable under the circumstances, and we evaluate these estimates

on an ongoing basis. We refer to accounting estimates of this type as critical accounting policies and estimates, which we discuss

further below. We have reviewed our critical accounting policies and estimates with the audit committee of our board of directors.

Income Taxes

uncertain tax positions and determining our provision for income taxes.

in which such determination is made. The provision for income taxes includes the impact of reserve provisions and changes

to reserves that are considered appropriate, as well as the related net interest and penalties. In addition, we are subject to the

continuous examination of our income tax returns by the IRS and other tax authorities which may assert assessments against

us. We regularly assess the likelihood of adverse outcomes resulting from these examinations and assessments to determine

the adequacy of our provision for income taxes.

Loss Contingencies

We are regularly subject to claims, suits, government investigations, and other proceedings involving competition and antitrust,

intellectual property, privacy, indirect taxes, labor and employment, commercial disputes, content generated by our users, goods and

claims for substantial or indeterminate amounts of damages. We record a liability when we believe that it is both probable that a

loss has been incurred, and the amount can be reasonably estimated. If we determine that a loss is possible and a range of the

loss can be reasonably estimated, we disclose the range of the possible loss in the Notes to the Consolidated Financial Statements.

accrued, and the matters and related ranges of possible losses disclosed, and make adjustments and changes to our disclosures

recorded, and such amounts could be material. Should any of our estimates and assumptions change or prove to have been

See Note 10 of Notes to Consolidated Financial Statements included in Item 8 of this Annual Report on Form 10-K for additional

information regarding contingencies.

Business Combinations

We allocate the fair value of purchase consideration to the tangible assets acquired, liabilities assumed and intangible assets

acquired based on their estimated fair values. The excess of the fair value of purchase consideration over the fair values of these

34

GOOGLE INC.

PART II