Abercrombie & Fitch 2001 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2001 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18

|

|

1716

Ab e r cr omb i e&Fitch Ab e rcrombi e &Fitch

have the right to draw upon the standby letters of credit if the

Company has authorized or filed a voluntary petition in

bankruptcy. To date, the beneficiaries have not drawn upon the

standby letters of credit.

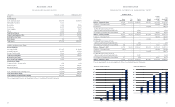

As of Fe b ru a ry 2, 2002, the Company was committed to non-

cancelable leases with remaining terms of one to fourteen years.

These commitments include store leases with initial terms ranging

primarily from ten to fifteen years. A summary of minimum rent

commitments under noncancelable leases follows (thousands):

Payments Due by Period

Total Less than 1 Ye a r 1-3 Years 4-5 Years After 5 Years

$822,920 $104,085 $211,270 $198,459 $309,106

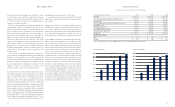

STORES AND GROSS SQ U ARE FEET Store count and gross

square footage by division were as follows:

February 2, 2002 February 3, 2001

Number Gross Square Number Gross Square

of Stores Feet (thousands) of Stores Feet (thousands)

Abercrombie & Fitch 309 2,798 265 2,443

abercrombie 148 662 84 375

Hollister Co. 34 213 5 31

Total 491 3,673 354 2,849

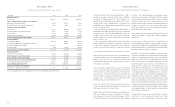

C A P I TAL EXPENDITURES Capital expenditures, net of con-

s t ruction allowances, totaled $126.5 million, $153.5 million and

$73.4 million for 2001, 2000 and 1999, respectively. Ad d i t i o n a l l y,

the noncash accrual for construction in progress totaled $1.0

million, $9.5 million and $10.4 million in 2001, 2000 and 1999,

r e s p e c t i v e l y. Capital expenditures related to the construction of

a new office and distribution center, including the noncash

a c c r ual for construction in progress, accounted for approxi-

mately $17 million, $92 million and $27 million of total capital

expenditures in 2001, 2000 and 1999, respectively. The office and

distribution center were completed in 2001. The balance of

capital expenditures related primarily to new stores.

The Company anticipates spending $105 to $115 million in

2002 for capital expenditures, of which $85 to $95 million will be

for new stores construction. The balance of expenditures pri-

marily relates to improving the in-store information technology

s t ructure and improvements in the distribution center. The

Company intends to add approximately 815,000 gross square feet

in 2002, which will represent a 22% increase over year-end 2001.

It is anticipated the increase will result from the addition of

approximately 40 new Abercrombie & Fitch stores, 30 aber-

crombie stores and 60 Hollister Co. stores.

The Company estimates that the average cost for leasehold

improvements and furniture and fixtures for Abercrombie & Fi t c h

stores opened in 2002 will approximate $600,000 per store, aft e r

giving effect to landlord allowances. In addition, inventory pur-

chases are expected to average approximately $300,000 per store.

The Company estimates that the average cost for leasehold

improvements and furniture and fixtures for abercrombie stores

opened in 2002 will approximate $500,000 per store, after giving

effect to landlord allowances. In addition, inventory purchases

are expected to average approximately $150,000 per store.

The Company estimates that the average cost for leasehold

improvements and furniture and fixtures for Hollister Co. stores

opened in 2002 will approximate $750,000 per store, after giving

effect to landlord allowances. However, the Company is in the

early stages of developing Hollister Co. and, as a result, current

average costs for leasehold improvements and furniture and fixtures

are not representative of future costs. In addition, inventory pur-

chases are expected to average approximately $250,000 per store.

The Company expects that substantially all future capital

expenditures will be funded with cash from operations. In addi-

tion, the Company has available a $150 million credit agreement

to support operations.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES T h e

C o m p a n y’s discussion and analysis of its financial condition

and results of operations are based upon the Company’s con-

solidated financial statements, which have been prepared in

accordance with accounting principles generally accepted in

the United States of America. The preparation of these finan-

cial statements requires the Company to make estimates and

assumptions that affect the reported amounts of assets, liabilities,

revenues and expenses. Since actual results may differ from those

estimates, the Company revises its estimates and assumptions as

new information becomes available.

The Company’s significant accounting policies can be found

in the Notes to Consolidated Financial Statements (Note 2).

The Company believes that the following policies are most

critical to the portrayal of the Company’s financial condition and

results of operations.

Revenue Recognition - The Company recognizes retail sales at

the time the customer takes possession of the merchandise and

purchases are paid for, primarily with either cash or credit card.

Catalogue and e-commerce sales are recorded upon shipment of

merchandise. Amounts relating to shipping and handling billed

to customers in a sale transaction are classified as revenue and the

related costs are classified as cost of goods sold. Employee dis-

counts are classified as a reduction of revenue. The Company

reserves for sales returns through estimates based on historical

experience and various other assumptions that management

believes to be reasonable.

I n v e n t o ry Valuation - Inventories are principally valued at the

lower of average cost or market, on a first-in first-out basis, utilizing

the retail method. The retail method of inventory valuation is an

averaging technique applied to different categories of inventory. At

A & F, the averaging is determined at the stock keeping unit (SKU )

level by averaging all costs for each SKU. An initial markup is

applied to inventory at cost in order to establish a cost-to-retail ratio.

Permanent markdowns, when taken, reduce both the retail and cost

components of inventory on hand so as to maintain the already

established cost–to-retail relationship. The use of the retail method

and the taking of markdowns effectively values inventory at the

lower of cost or market. The Company further reduces inventory

by recording an additional markdown reserve using the retail

c a r rying value of inventory from the season just passed.

Markdowns on this carryover inventory represent the future

anticipated selling prices. Ad d i t i o n a l l y, as part of inventory val-

uation, an inventory shrinkage estimate is made each period

that reduces the value of inventory for lost or stolen items.

Inherent in the retail method calculation are certain significant

judgments and estimates including, among others, initial markup,

markdowns and shrinkage, which could significantly impact

the ending inventory valuation at cost as well as resulting gross

margins. Management believes that this inventory valuation

method provides a conservative inventory valuation as it preserv e s

the cost-to-retail relationship in inventory.

Property and Equipment - Depreciation and amortization of

property and equipment are computed for financial reporting

purposes on a straight-line basis, using service lives ranging prin-

cipally from 10-15 years for leasehold improvements and 3-10

years for other property and equipment. Beneficial leaseholds

represent the present value of the excess of fair market rent over

contractual rent of existing stores at the 1988 purchase of the

Abercrombie & Fitch business by T he Limited, Inc. (“The

Limited”) and are being amortized over the lives of the related

leases. The cost of assets sold or retired and the related accumu-

lated depreciation or amortization are removed from the accounts

with any resulting gain or loss included in net income.

Maintenance and repairs are charged to expense as incurred.

Major renewals and betterments that extend service lives are cap-

italized. Long-lived assets are reviewed at the store level at least

annually for impairment or whenever events or changes in cir-

cumstances indicate that full recoverability is questionable. Fa c t o r s

used in the evaluation include, but are not limited to, manage-

ment's plans for future operations, recent operating results and

projected cash flows.

Income Taxes - Income taxes are calculated in accordance with

Statement of Financial Accounting Standards (“SFAS”) No.

109, “Accounting for Income Taxes,” which requires the use of the

liability method. Deferred tax assets and liabilities are recognized

based on the difference between the financial statement carry i n g

amounts of existing assets and liabilities and their respective tax

bases. Inherent in the measurement of deferred balances are cer-

tain judgments and interpretations of enacted tax law and

published guidance with respect to applicability to the Company’ s

operations. Significant examples of this concept include capital-

ization policies for various tangible and intangible costs, income

and expense recognition and inventory valuation methods. No

valuation allowance has been provided for deferred tax assets

because management believes the full amount of the net deferred

tax assets will be realized in the future. The effective tax rate uti-

lized by the Company reflects management’s judgment of the

expected tax liabilities within the various taxing jurisdictions.

R E C E N T LY ISSUED ACCOUNTING PRONOUNCEMENTS

In June 2001, the Financial Accounting Standards Board (“FA S B” )

issued SFAS No. 142, “Goodwill and Other Intangible Assets.”

The standard is effective starting with fiscal years beginning aft e r

December 15, 2001 (Fe b ru a ry 3, 2002 for the Company). SFA S

No. 142 addresses how intangible assets that are acquired indi-

vidually or with a group of other assets should be accounted for

in financial statements upon their acquisition. It also addresses