Xcel Energy 2002 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2002 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

|

|

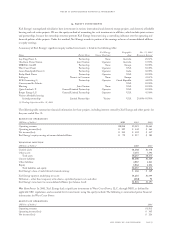

17.derivative valuation and financial impacts

use of derivatives to manage risk

Business and Operational Risk Xcel Energy and its subsidiaries are exposed to commodity price risk in their generation, retail distribution

and energy trading operations. In certain jurisdictions, purchased power expenses and natural gas costs are recovered on a dollar-for-dollar

basis. However, in other jurisdictions, Xcel Energy and its subsidiaries are exposed to market price risk for the purchase and sale of electric

energy and natural gas. In such jurisdictions, we recover purchased power expenses and natural gas costs based on fixed price limits or

under established sharing mechanisms.

Commodity price risk is managed by entering into purchase and sales commitments for electric power and natural gas, long-term contracts

for coal supplies and fuel oil, and derivative financial instruments. Xcel Energy’s risk management policy allows us to manage the market

price risk within each rate-regulated operation to the extent such exposure exists. Management is limited under the policy to enter into only

transactions that manage market price risk where the rate regulation jurisdiction does not already provide for dollar-for-dollar recovery.

One exception to this policy exists in which we use various physical contracts and derivative instruments to reduce the cost of natural

gas and electricity we provide to our retail customers even though the regulatory jurisdiction provides dollar-for-dollar recovery of actual

costs. In these instances, the use of derivative instruments and physical contracts is done consistently with the local jurisdictional cost

recovery mechanism.

Xcel Energy and its subsidiaries are exposed to market price risk for the sale of electric energy and the purchase of fuel resources, including

coal, natural gas and fuel oil used to generate the electric energy within its nonregulated operations. Xcel Energy manages this market

price risk by entering into firm power sales agreements for approximately 55 to 75 percent of its electric capacity and energy from each

generation facility, using contracts with terms ranging from one to 25 years. In addition, we manage the market price risk covering the

fuel resource requirements to provide the electric energy by entering into purchase commitments and derivative instruments for coal,

natural gas and fuel oil as needed to meet fixed-priced electric energy requirements. Xcel Energy’s risk management policy allows us to

manage the market price risks and provides guidelines for the level of price risk exposure that is acceptable within our operations.

Xcel Energy is exposed to market price risk for the sale of electric energy and the purchase of fuel resources used to generate the

electric energy from our equity method investments that own electric operations. Xcel Energy manages this market price risk

through our involvement with the management committee or board of directors of each of these ventures. Our risk management

policy does not cover the activities conducted by the ventures. However, other policies are adopted by the ventures as necessary and

mandated by the equity owners.

Interest Rate Risk Xcel Energy and its subsidiaries are exposed to fluctuations in interest rates where we enter into variable rate debt

obligations to fund certain power projects being developed or purchased. Exposure to interest rate fluctuations may be mitigated by

entering into derivative instruments known as interest rate swaps, caps, collars and put or call options. These contracts reduce exposure

to the volatility of cash flows for interest and result in primarily fixed-rate debt obligations when taking into account the combination of

the variable rate debt and the interest rate derivative instrument. Xcel Energy’s risk management policy allows us to reduce interest rate

exposure from variable rate debt obligations.

Currency Exchange Risk Xcel Energy and its subsidiaries have certain investments in foreign countries exposing us to foreign currency

exchange risk. The foreign currency exchange risk includes the risk relative to the recovery of our net investment in a project, as well as

the risk relative to the earnings and cash flows generated from such operations. Xcel Energy manages its exposure to changes in foreign

currency by entering into derivative instruments as determined by management. Our risk management policy provides for this risk

management activity.

Trading Risk Xcel Energy and its subsidiaries conduct various trading operations and power marketing activities, including the purchase

and sale of electric capacity and energy and natural gas. The trading operations are conducted both in the United States and Europe

with primary focus on specific market regions where trading knowledge and experience have been obtained. Xcel Energy’s risk

management policy allows management to conduct the trading activity within approved guidelines and limitations as approved by

our risk management committee made up of management personnel not involved in the trading operations.

derivatives as hedges

2001 Accounting Change On Jan. 1, 2001, Xcel Energy and its subsidiaries adopted SFAS No. 133 – “Accounting for Derivative

Instruments and Hedging Activities.” This statement requires that all derivative instruments as defined by SFAS No. 133 be recorded on the

balance sheet at fair value unless exempted. Changes in a derivative instrument’s fair value must be recognized currently in earnings unless

the derivative has been designated in a qualifying hedging relationship. The application of hedge accounting allows a derivative instrument’s

gains and losses to offset related results of the hedged item in the statement of operations, to the extent effective. SFAS No. 133 requires that

the hedging relationship be highly effective and that a company formally designate a hedging relationship to apply hedge accounting.

A fair value hedge requires that the effective portion of the change in the fair value of a derivative instrument be offset against the change

in the fair value of the underlying asset, liability or firm commitment being hedged. That is, fair value hedge accounting allows the

page 82 xcel energy inc. and subsidiaries

notes to consolidated financial statements