Stein Mart 2008 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2008 Stein Mart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

shall be included in the computation of earnings-per-share pursuant to the two-class method. The Company’s restricted stock awards

are considered “participating securities” because they contain non-forfeitable rights to dividends. FSP EITF No. 03-6-1 is effective for

financial statements issued for fiscal years beginning after December 15, 2008 and all prior-period earnings per share data presented

shall be adjusted retrospectively. Early application is not permitted. The adoption of FSP EITF No. 03-6-1 will not have a material

impact on our consolidated financial statements.

In February 2007, the FASB issued SFAS No. 159, The Fair Value Option for Financial Assets and Financial Liabilities, which permits

entities to choose to measure many financial instruments and certain other items at fair value that are not currently required to be

measured at fair value. SFAS No. 159 was effective for the Company on February 3, 2008 and had no effect on the Company’s

financial position or results of operations.

In September 2006, the EITF issued EITF No. 06-4, Accounting for Deferred Compensation and Postretirement Benefit Aspects of

Endorsement Split-Dollar Life Insurance Arrangements. EITF No. 06-4 states that an employer accounting for endorsement split-

dollar life insurance arrangements that provide a benefit to an employee that extends to postretirement periods should recognize a

liability for future benefits in accordance with SFAS No. 106, Employers' Accounting for Postretirement Benefits Other Than Pensions,

or Accounting Principles Board Opinion No. 12, Omnibus Opinion-1967. The Company adopted EITF 06-4 on February 3, 2008 and

recorded a $4.5 million liability (included in other liabilities) through a reduction to retained earnings to reflect the cumulative effect of

the change in accounting principle.

In September 2006, the FASB issued SFAS No. 157, Fair Value Measurements, which defines fair value, establishes a framework for

measuring fair value in generally accepted accounting principles, and expands disclosures about fair value measurements. SFAS No.

157 does not require any new fair value measurements, but rather eliminates inconsistencies in guidance provided in previous

accounting pronouncements. In February 2008, the FASB issued FASB Staff Position ("FSP") No. FAS 157-2, Effective Date of

FASB Statement No. 157, that deferred the effective date of SFAS No. 157 for one year for nonfinancial assets and liabilities that are

recognized or disclosed at fair value in the financial statements on a non-recurring basis. The Company adopted the provisions of

SFAS No. 157 for financial assets and liabilities effective February 3, 2008 and it had no effect on our consolidated financial

statements. Management does not expect the full adoption of FAS No. 157, effective February 1, 2009, to have a material impact on

our consolidated financial statements.

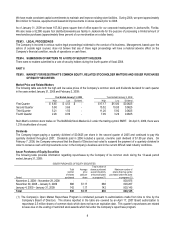

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

The Company is exposed to interest rate risk primarily through borrowings under its revolving credit facility which are at variable rates.

The facility permits debt commitments up to $150 million, has a January 2011 maturity date and bears interest at spreads over the

prime rate and LIBOR. At January 31, 2009, the Company had $100 million in direct borrowings under its credit facility and $69.5

million invested in short-term money market funds. Subsequent to year-end, the Company liquidated the money market funds and

repaid that portion of its borrowings.

For 2008, average borrowings under our revolving credit facility were $53 million. If interest rates on 2008 average borrowings

changed by 100 basis points, our annual interest expense would change by $530,000, assuming comparable borrowing levels.

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

The consolidated financial statements of the Company and the Report of Independent Registered Certified Public Accounting Firm

thereon are filed pursuant to this Item 8 and are included in this report beginning on page F-1.

ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

None.

ITEM 9A. CONTROLS AND PROCEDURES

Evaluation of Disclosure Controls and Procedures

The Company, under the supervision and with the participation of the Company’s management, including the Chief Executive Officer

and Chief Financial Officer, has carried out an evaluation of the effectiveness of the design and operation of the Company’s

disclosure controls and procedures, as defined in Rule 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934, as

amended, as of the end of the period covered by this report.

No system of controls, no matter how well designed and operated, can provide absolute assurance that the objectives of the system

of controls are met, and no evaluation of controls can provide absolute assurance that the system of controls has operated effectively

in all cases. The Company’s disclosure controls and procedures however are designed to provide reasonable assurance that the

objectives of disclosure controls and procedures are met.

19