Public Storage 2014 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2014 Public Storage annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

5

Economics

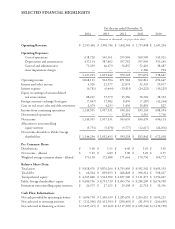

Our business has excellent economics. Our properties generally break-even (revenues equaling expenses)

at about 30% occupancy and we operate them above 90%. There are nominal marginal costs required in

improving occupancies (see earlier comment on customer acquisition costs), which means most of the

incremental revenue is profit. Our overall operating margins are above 70%, in part because of our brand

and market focus/scale.

Our business requires little maintenance capital expenditures, about half as much as other types of

real estate. In addition, we are able to grow our revenues a little better than apartment rents (the

government doesn’t provide capital to our industry) and almost double other types of real estate

( generally 4% versus 2%), as we benefit from increased population, population density and higher incomes

and are relatively immune to changes in general business conditions (technology, patents, business

cycle, oil prices, etc.). We also have ancillary businesses that generate significant additional income

but require little capital.

As a result of exceptional economic characteristics, we generate a tremendous amount of free cash flow

that can either be re-invested or distributed. Over the last 20 years, our cash flow and dividends per share have

each grown at about 9% per year. Few companies grow cash flow per share as much while also distributing

most of their earnings.

Brand and People

We have the BEST brand in the industry and one of the few brands in the real estate business. Our brand

consistently lands at the top of the Google search page. Because of our market scale, we pay much less than our

competitors on a “cost per click.” Our brand helps us to consistently operate at higher occupancies and

achieve greater rents and cash flow per foot than our competitors.

Our brand is protected and enhanced by our 5,000 plus employees. Candy Krol, who leads our human

resources group, devotes tremendous time and resources to hiring, training and developing our people.

We have many employees who have been with us for over ten years, some as long as 30 years. Over

2,000 live “on-site” at our properties. They treat our customers like family and we work hard to treat our

employees the same way.

Shareholder Attitude

Nearly all of our managers own stock in our company in one form or another. We think this helps create an

environment of “ownership,” longer-term thinking and customer-focused behavior. Our incentive plans

and culture are focused on generating long-term growth in cash flow per share. We rarely issue common

shares and when we do, we negotiate to obtain at least as much value as we give up. We prefer paying cash

versus issuing shares in most cases.

In summary, we have a phenomenal business with exceptional economics. We work hard to avoid what

Warren Buffett calls the ABCs of business decay: arrogance, bureaucracy and complacency. If we

remain disciplined in the allocation of capital (see below), continue to drive operational excellence and

avoid the ABCs, our company will continue to generate prodigious free cash flow.

European Self-Storage

Shurgard Europe had an excellent 2014. Lead by Marc Oursin, Shurgard Europe’s CEO, the company achieved

the first year-over-year increase in same store occupancies in seven years, moving from 82.3% to 87.8%–an

incredible performance! This growth was achieved by lower rental rates and higher promotional discounts,

resulting in 2.9% of revenue growth in the same store pool of properties.