O'Reilly Auto Parts 2008 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2008 O'Reilly Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

cohesive management direction. Facing serious constraints

on access to capital, CSK began exploring strategic alternatives

in early 2008. Due to a complementary geographic

distribution of stores, it had long been speculated that we

would be a likely acquirer of CSK. While we had, at various

times, undertaken cursory discussions along those lines, it

was never a serious consideration given the high price that

would have been necessary to acquire CSK and their public

unwillingness to entertain overtures to be acquired. In light of

their financial condition and public announcement to explore

strategic alternatives, we saw a tremendous opportunity

inherent in CSK at a much more reasonable acquisition

price, and we became very active both inside and outside of

their strategic evaluation process. The difficulty in raising

capital in a historically bad credit market in 2008 presented

a major obstacle to any potential acquirer of CSK. Based

on the strength of our balance sheet and the merits of our

consistently strong historical operating results, we were able

to obtain debt commitments sufficient for us to acquire CSK

in an all-cash deal. With the financing commitments in hand,

we were able to effectively negotiate to acquire CSK. We

were then able to alter the structure of the transaction to an

exchange offer, which allowed us to maintain the financial

flexibility necessary for strategic investments in CSK’s

distribution infrastructure and inventory position.

The true opportunity at CSK is to maintain CSK’s strong

retail base and dramatically increase the commercial business

by successfully implementing our dual market strategy. To

realize the value potential at CSK, we will convert all of the

CSK stores to the O’Reilly brand and implement our dual

market strategy. At the time of the acquisition, only 10% of

CSK’s sales were to commercial installers as compared to 50%

at O’Reilly. To successfully implement our proven dual market

strategy, we will focus on distribution, inventory availability

and culture.

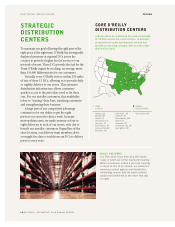

CSK operated a retail-focused distribution network with

four main distribution centers (DCs) servicing stores on a

weekly basis. We are closing one CSK DC that overlaps with

an existing O’Reilly DC, renovating the remaining three

CSK DCs, adding four new DCs and utilizing three existing

O’Reilly DCs to service the acquired CSK stores. This large

investment in distribution infrastructure will allow for nightly

deliveries to all stores and multiple daily store deliveries in the

seven metropolitan areas where the DCs are located.

Prior to the acquisition, the average CSK store stocked

18,000 SKUs. We will eliminate non-core automotive

merchandise and bring the SKU count up to the O’Reilly

average of 21,000 with a clear focus on hard parts.

MARKET FACTORS

The fundamental drivers in our industry

remain strong. During challenging economic

conditions, our customers are more willing

to maintain and repair their current vehicle

rather than purchase a new vehicle. This

increase in the average age of vehicles on

the road drives demand for our products.

249 MILLION

VEHICLE POPULATION

2.9 TRILLION

MILES DRIVEN

9.8 YEARS

AVERAGE AGE OF VEHICLE

ROAD TESTED. RESULTS DRIVEN.

PG.2 O’REILLY AUTOMOTIVE 2008 ANNUAL REPORT

MARKET

CONSOLIDATION

OPPORTUNITY

The largest suppliers in the automotive

aftermarket make up a relatively small

percentage of the overall market, even

after several years of steady consolidation.

We continue to opportunistically pursue

strategic acquisitions to take advantage

of further market consolidation.

AUTOZONE ................................... 12%

ADVANCED AUTO PARTS ..................... 9%

O’REILLY AUTO PARTS .................... 9%

GENERAL PARTS INC./CARQUEST ....... 5%

GENERAL PARTS/NAPA .............. 3%

REMAINING MARKET .............. 62%