EasyJet 2011 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2011 EasyJet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

14

easyJet plc

Annual report

and accounts 2011

Chief Executive’s introduction

Continued

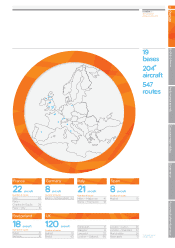

has gained share on routes to London, Milan and

Madrid as competitors have retreated. Switzerland has

also seen a stable economic environment and easyJet’s

focus in 2011 has been on defending its leading position

at Basel and Geneva whilst increasing its focus on

passengers travelling on business.

Spain continues to be one of the most competitive

markets in Europe. In 2011 easyJet refocused capacity

to enable the network to improve profitability and

attract more passengers travelling on business. In Spain

more than 60% of air travel is purchased in offline

channels and consequently easyJet is implementing

measures to improve its presence in these areas.

Despite a difficult economic environment in Italy the

short-haul intra-European market remains buoyant

easyJet grew capacity by around 11% as it built its

presence in selected key Italian markets of Milan, Rome,

Naples and Venice. At Milan Malpensa easyJet further

consolidated its leading share as Lufthansa announced

the closure of its base.

easyJet consolidated its position as the number two

airline in France and increased its capacity by 29% as it

continued with its strategy to build its position as the

alternative airline to Air France in major French airports.

easyJet’s share of the French short-haul market is now

12%. easyJet also announced that it intends to open

bases in 2012 at Toulouse and Nice. easyJet already has

a 20% market share at these airports.

Looking forward to 2012

Hedging positions

easyJet operates under a clear set of treasury policies

agreed by the Board. The aim of easyJet’s hedging

policy is to reduce short-term earnings volatility.

Therefore easyJet hedges forward, on a rolling basis,

between 65% and 85% of the next 12 months

anticipated fuel and currency requirements and

between 45% and 65% of the following 12 months

anticipated requirements.

Details of our current hedging arrangements are set

out below:

Percentage of anticipated requirement / surplus hedged Fuel requirement US dollar requirement Euro surplus sale

Six months ending 31 March 2012 80% 80% 76%

Rate/$ per MT $950 per MT $1.60 €1.13

Full year ending 30 September 2012 73% 69% 71%

Rate/$ per MT $956 per MT $1.59 €1.13

Full year ending 30 September 2013 49% 46% 50%

Rate/$ per MT $979 per MT $1.61 €1.14

Sensitivities

– A $10 movement per metric tonne impacts the 2012

fuel bill by $5 million

– A one cent movement in £/$ impacts the 2012 profit

before tax by £3 million

Outlook

The macroeconomic environment remains challenging

for all airlines as weak consumer confidence across

Europe slows the rate at which higher fuel prices and

increased taxation can be passed on to passengers.

Against this backdrop easyJet is taking a cautious

approach to capacity deployment. As a result, capacity

in the first half of the year is planned to be flat

(adjusting for disruption in the first part of the prior

year), with growth of around 4% for the full year.

With around 45% of winter seats now sold, in line with

the prior year, first half passenger revenue per seat is

expected to grow by mid-single digits with planned

improvement in yields, bag charges and other ancillary

revenues.

Cost per seat excluding fuel and currency7 impact is

expected to grow by 2 to 3% for the full year and by

4% in the first half, assuming normal levels of disruption,

of the year driven by price increases at regulated

airports and investments in new revenue streams.

Example only. Not a current offer.