Dish Network 2002 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2002 Dish Network annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

|

|

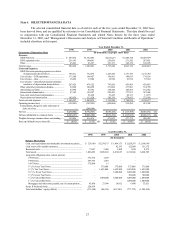

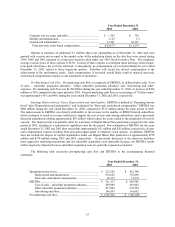

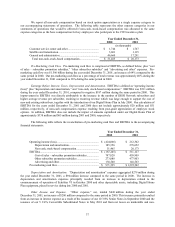

28

Year Ended December 31,

1998 1999 2000 2001 2002

(In thousands, except subscribers and per subscriber data)

Other Data

DISH Network subscribers ....................................... 1,940,000 3,410,000 5,260,000 6,830,000 8,180,000

Average monthly revenue per subscriber.................. $ 39.25 $ 42.71 $ 45.33 $ 49.32 $ 49.17

EBITDA(4)................................................................ (20,255) (172,803) (187,245) 511,127 805,585

Less amortization of subscriber acquisition costs..... (18,869) – – – –

EBITDA, as adjusted to exclude amortization of

subscriber acquisition costs .................................. (39,124) (172,803) (187,245) 511,127 805,585

Net cash flows from:

Operating activities............................................... (16,890) (58,513) (118,677) 489,483 66,744

Investing activities ................................................ (8,048) (62,826) (911,957) (1,279,119) (682,387)

Financing activities............................................... (13,722) 920,091 982,153 1,610,707 420,832

(1) Net loss in 2002 includes $690 million related to merger termination costs.

(2) The net loss attributable to common shares in 2002 of $444 million differs significantly from net loss in 2002 of $882 million due to a gain on

repurchase of Series D Convertible Preferred Stock of approximately $437 million.

(3) The loss per share amount in 1999 of $(1.92) includes $(1.28) per share relating to basic and diluted loss per share before extraordinary charges

and $(0.64) per share relating to the extraordinary charge for early retirement of debt, net of tax.

(4) We believe it is common practice in the telecommunications industry for investment bankers and other investors to use various multiples of

current or projected EBITDA (operating income (loss) plus depreciation and amortization, and non-cash, stock-based compensation) for purposes

of estimating current or prospective enterprise value and as one of many measures of operating performance. Conceptually, EBITDA measures

the amount of income generated each period that could be used to service debt, pay taxes and fund capital expenditures because EBITDA is

independent of the actual leverage employed by the business. We use EBITDA, as defined above, as one of the key measurements of operating

efficiency and overall financial performance and believe EBITDA can be a helpful measure for those evaluating companies in the multi-channel

video programming distribution market. Some investment analysts track the relationship of EBITDA to total debt as one measure of financial

strength. However, EBITDA does not purport to represent cash provided or used by operating activities and should not be considered in isolation

or as a substitute for measures of performance prepared in accordance with generally accepted accounting principles.

EBITDA differs significantly from cash flows from operating activities reflected in the consolidated statement of cash flows. Cash flows from

operating activities is net of interest and taxes paid and is a more comprehensive determination of periodic income on a cash (vs. accrual) basis,

exclusive of non-cash items of income and expenses such as depreciation and amortization. In contrast, EBITDA is derived from accrual basis

income and is not reduced for cash invested in working capital. Consequently, EBITDA is not affected by the timing of receivable collections or

when accrued expenses are paid. We are not aware of any uniform standards for determining EBITDA and believe presentations of EBITDA

may not be calculated consistently by different entities in the same or similar businesses. We have shown EBITDA with the add-back of the

amortization of subscriber acquisition costs, which were deferred through September 1997 and amortized over one year. EBITDA for the years

ended December 31, 1999, 2000, 2001 and 2002 also excludes approximately $61 million, $51 million, $20 million and $11 million, respectively,

in non-cash, stock-based compensation expense resulting from significant post-grant appreciation of stock options granted to employees. In

addition, EBITDA does not include the impact of capital expenditures under our Digital Home Plan of approximately $65 million, $338 million

and $278 million during the years ended December 31, 2000, 2001 and 2002, respectively. See Item 7 “Management’s Discussion and Analysis

of Financial Condition and Results of Operations” for the quantitative reconciliation of EBITDA to the accompanying financial statements.