CDW 2012 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2012 CDW annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

|

|

Table of Contents

Our sales are dependent on continued innovations in hardware, software and services offerings by our vendor partners and the

competitiveness of their offerings, and our ability to partner with new and emerging technology providers.

The technology industry is characterized by rapid innovation and the frequent introduction of new and enhanced hardware, software and

services offerings. We have been and will continue to be dependent on innovations in hardware, software and services offerings, as well as the

acceptance of those innovations by customers. A decrease in the rate of innovation, or the lack of acceptance of innovations by customers, could

have an adverse effect on our business, results of operations or cash flows.

In addition, if we are unable to keep up with changes in technology and new hardware, software and services offerings, for example by

providing the appropriate training to our account managers, sales technology specialists and engineers to enable them to effectively sell and

deliver such new offerings to customers, our business, results of operations or cash flows could be adversely affected.

We also are dependent upon our vendor partners for the development and marketing of hardware, software and services to compete

effectively with hardware, software and services of vendors whose products and services we do not currently offer or that we are not authorized

to offer in one or more customer channels. To the extent that a vendor's offering that is highly in demand is not available to us for resale in one

or more customer channels, and there is not a competitive offering from another vendor that we are authorized to sell in such customer channels,

our business, results of operations or cash flows could be adversely impacted.

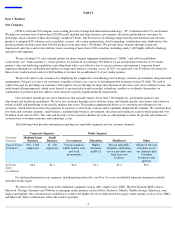

Substantial competition could reduce our market share and significantly harm our financial performance.

Our current competition includes:

We expect the competitive landscape in which we compete to continue to change as new technologies are developed. While innovation

can help our business as it creates new offerings for us to sell, it can also disrupt our business model and create new and stronger competitors.

Some of our hardware and software vendor partners sell, and could intensify their efforts to sell, their products directly to our

customers. In addition, traditional OEMs are increasing their services capabilities through mergers and acquisitions with service providers,

which could potentially increase competition in the market to provide comprehensive technology solutions to customers. Moreover, newer,

potentially disruptive technologies exist and are being developed that deliver technology solutions as a service, for example, cloud based

solutions, including Software as a Service ("SaaS"), Infrastructure as a Service ("IaaS") and Platform as a Service ("PaaS"). These technologies

could increase the amount of sales directly to customers rather than through resellers like us, or could lead to a reduction in our profitability. If

any of these trends becomes more prevalent, it could adversely affect our business, results of operations or cash flows.

We focus on offering a high level of service to gain new customers and retain existing customers. To the extent we face increased

competition to gain and retain customers, we may be required to reduce prices, increase advertising expenditures or take other actions which

could adversely affect our business, results of operations or cash flows. Additionally, some of our competitors may reduce their prices in an

attempt to stimulate sales, which may require us to reduce prices. This would require us to sell a greater number of products to achieve the same

level of net sales and gross profit. If such a reduction in prices occurs and we are unable to attract new customers and sell increased quantities of

products, our sales growth and profitability could be adversely affected.

The success of our business depends on the continuing development, maintenance and operation of our information technology systems.

Our success is dependent on the accuracy, proper utilization and continuing development of our information technology systems,

including our business systems, Web servers and voice and data networks. The quality and our utilization

11

•

National resellers such as Dimension Data, ePlus, Insight Enterprises, PC Connection, PCM, Presidio, Softchoice, World Wide

Technology and many regional and local resellers;

• Manufacturers who sell directly to customers, such as Dell, Hewlett-

Packard and Apple;

• e-

tailers, such as Amazon, Newegg, TigerDirect.com and Buy.com;

• Large service providers and system integrators, such as IBM, Accenture, Hewlett-

Packard and Dell; and

• Retailers (including their e-

commerce activities) such as Staples, Office Depot and Office Max.