Vodafone 1997 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 1997 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

|

|

Vodafone Group Plc Annual Report & Accounts for the year ended 31 March 1997

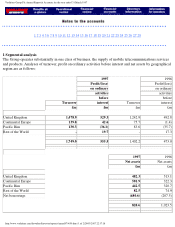

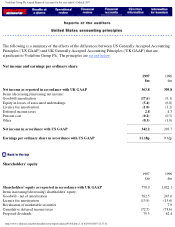

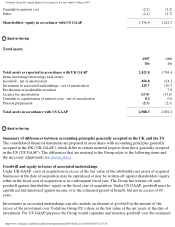

Cumulative pension cost (2.2) (2.2)

Other (2.1) (1.7)

Shareholders' equity in accordance with US GAAP 1,336.9 1,241.3

Total assets

1997 1996

£m £m

Total assets as reported in accordance with UK GAAP 2,421.8 1,763.4

Items increasing/(decreasing) total assets:

Goodwill - net of amortisation 456.8 114.3

Investment in associated undertakings - net of amortisation 125.7 130.7

Revaluation of marketable securities -7.9

Licence fee amortisation (13.9) (13.6)

Cumulative capitalisation of interest costs - net of amortisation 0.2 0.6

Pension prepayment (2.3) (2.1)

Total assets in accordance with US GAAP 2,988.3 2,001.2

Summary of differences between accounting principles generally accepted in the UK and the US

The consolidated financial statements are prepared in accordance with accounting principles generally

accepted in the UK ('UK GAAP'), which differ in certain material respects from those generally accepted

in the US ('US GAAP'). The differences that are material to the Group relate to the following items and

the necessary adjustments are shown above.

Goodwill and equity in losses of associated undertakings

Under UK GAAP, costs of acquisition in excess of the fair value of the attributable net assets of acquired

businesses at the date of acquisition may be capitalised or may be written-off against shareholders' equity,

either in the fiscal year of acquisition or in a subsequent fiscal year. The Group has written-off such

goodwill against shareholders' equity in the fiscal year of acquisition. Under US GAAP, goodwill must be

capitalised and amortised against income over the estimated period of benefit, but not in excess of 40

years.

Investments in associated undertakings can also include an element of goodwill in the amount of the

excess of the investment over Vodafone Group Plc's share in the fair value of the net assets at the date of

investment. For US GAAP purposes the Group would capitalise and amortise goodwill over the estimated

http://www.vodafone.com/download/investor/reports/annual97/4/8.htm (2 of 4)29/03/2007 22:37:32